Multiple Choice

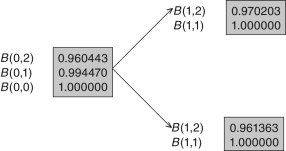

Use the fact that the pseudo-probability of default at time zero is (1/ 2) to answer the questions that follow.

Use the fact that the pseudo-probability of default at time zero is (1/ 2) to answer the questions that follow.

-Consider a floorlet with maturity time 1 and strike price 0.035.What are the payoffs to the option at time 1 in the up and down nodes?

A) 0.0307,0.0402

B) 0.0042,0.0000

C) 0.0354,0.0056

D) 0.0050,0.0050

E) 0.0000,0.0050

Correct Answer:

Verified

Correct Answer:

Verified

Q13: Which of the following statements about an

Q14: <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB4275/.jpg" alt=" Use the fact

Q15: Suppose that a company has issued a

Q16: <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB4275/.jpg" alt=" Use the fact

Q17: The writer of an interest rate floor

Q18: Suppose that a portfolio manager has purchased

Q19: Use the following tree to answer the

Q20: Which of the following statements is INCORRECT?<br>A)

Q22: Use the following tree to answer the

Q23: Which of the following statements is correct?<br>A)