Multiple Choice

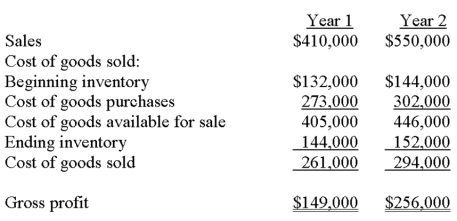

Louise Company reported the following income statement information for Year 1 and Year 2:  The beginning inventory balance for Year 1 is correct. The ending inventory balance for Year 2 is also correct. However, the ending inventory figure for Year 1 was overstated by $20,000. Given this information, the correct gross profit figures for Year 1 and Year 2 would be:

The beginning inventory balance for Year 1 is correct. The ending inventory balance for Year 2 is also correct. However, the ending inventory figure for Year 1 was overstated by $20,000. Given this information, the correct gross profit figures for Year 1 and Year 2 would be:

A) $129,000 for Year 1 and $256,000 for Year 2.

B) $281,000 for Year 1 and $274,000 for Year 2.

C) $129,000 for Year 1 and $276,000 for Year 2.

D) $169,000 for Year 1 and $236,000 for Year 2.

E) $169,000 for Year 1 and $276,000 for Year 2.

Correct Answer:

Verified

Correct Answer:

Verified

Q24: In applying the lower of cost or

Q31: An error in the period-end inventory causes

Q32: Sarbanes Oxley (SOX) demands that companies safeguard

Q38: Tops had cost of goods sold of

Q41: The _ method of assigning costs to

Q73: Some companies use the _ principle or

Q140: Regardless of what inventory method or system

Q156: Using the information given below for a

Q169: A company reported the following information regarding

Q184: The inventory valuation method that has the