Multiple Choice

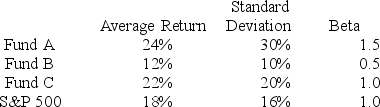

You want to evaluate three mutual funds using the Sharpe measure for performance evaluation. The risk-free return during the sample period is 6%. The average returns, standard deviations, and betas for the three funds are given below, as are the data for the S&P 500 Index.

The fund with the highest Sharpe measure is

A) Fund A.

B) Fund B.

C) Fund C.

D) Funds A and B (tied for highest) .

E) Funds A and C (tied for highest) .

Correct Answer:

Verified

Correct Answer:

Verified

Q1: Suppose a particular investment earns an arithmetic

Q2: You want to evaluate three mutual funds

Q6: The following data are available relating to

Q7: You want to evaluate three mutual funds

Q9: Studies of style analysis have found that

Q23: The Jensen portfolio evaluation measure<br>A) is a

Q32: The geometric average rate of return is

Q62: Suppose you own two stocks, A and

Q68: Suppose two portfolios have the same average

Q74: The dollar-weighted return on a portfolio is