Multiple Choice

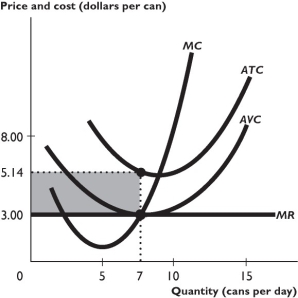

The above figure shows some a firm's cost curves and its marginal revenue curve.

-Consider a short-run equilibrium in a perfectly competitive market.Suppose that the firms' average total cost and marginal cost schedules differ.In the short run,

A) all firms in the market must be able to make an economic profit.

B) all firms produce equal amounts of output.

C) some firms might incur an economic loss, but still produce output.

D) some firms might make an economic profit and, as a result, shut down.

E) all firms in the market must be able to make either positive or zero economic profit.

Correct Answer:

Verified

Correct Answer:

Verified

Q44: Is the number of sellers in the

Q163: If the price received by a perfectly

Q220: In the short run,a perfectly competitive firm

Q221: <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB1458/.jpg" alt=" -The above figure

Q222: For a perfectly competitive rancher in Wyoming,if

Q223: Perfect competition _ a fair outcome _.<br>A)

Q226: <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB1458/.jpg" alt=" -The above figure

Q227: Suppose a perfectly competitive market is in

Q228: A perfectly competitive firm is a price

Q230: The demand curve faced by a perfectly