Essay

(Requires Appendix material)Your textbook states that in "the distributed lag regression model,the error term ut can be correlated with its lagged values.This autocorrelation arises,because,in time series data,the omitted factors that comprise ut can themselves be serially correlated."

(a)Give an example what the authors have in mind.

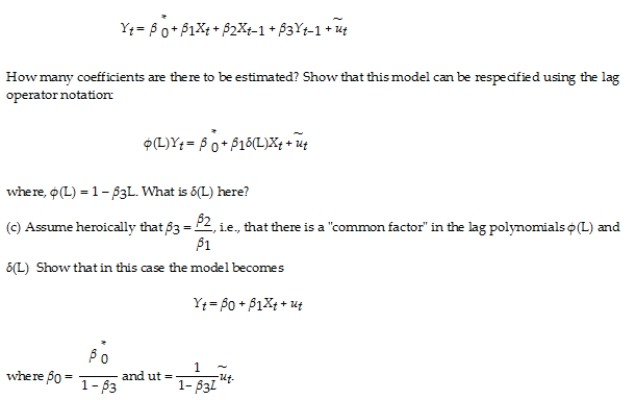

(b)Consider the ADL model,where the X's are strictly exogenous,and there is no autocorrelation (and/or heteroskedasticity)in the error term.  (d)Explain why autocorrelation in this model can be seen as a "simplification," not a "nuisance." Can you use the F-test to test the above hypothesis? Why or why not?

(d)Explain why autocorrelation in this model can be seen as a "simplification," not a "nuisance." Can you use the F-test to test the above hypothesis? Why or why not?

Correct Answer:

Verified

(a)Taking the textbook example of the pe...View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q8: The impact effect is the<br>A)zero period dynamic

Q17: Autocorrelation of the error terms<br>A)makes it impossible

Q23: Heteroskedasticity- and autocorrelation-consistent standard errors<br>A)result in the

Q27: In the distributed lag model, the dynamic

Q31: Your textbook presents as an example of

Q32: It has been argued that Canada's aggregate

Q37: Infeasible GLS<br>A)requires too much memory even for

Q40: In the distributed lag model, the coefficient

Q45: HAC standard errors should be used because<br>A)they

Q46: GLS involves<br>A)writing the model in differences and