Essay

You have collected quarterly data on Canadian unemployment (UrateC)and inflation (InfC)from 1962 to 1999 with the aim to forecast Canadian inflation.

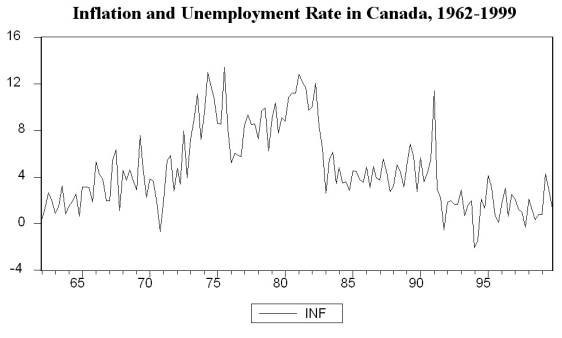

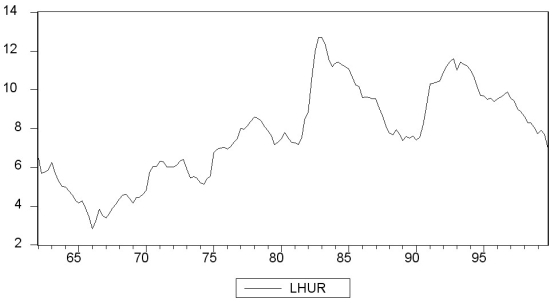

(a)To get a better feel for the data,you first inspect the plots for the series.

Inspecting the Canadian inflation rate plot and having calculated the first autocorrelation to be 0.79 for the sample period,do you suspect that the Canadian inflation rate has a stochastic trend? What more formal methods do you have available to test for a unit root?

Inspecting the Canadian inflation rate plot and having calculated the first autocorrelation to be 0.79 for the sample period,do you suspect that the Canadian inflation rate has a stochastic trend? What more formal methods do you have available to test for a unit root?

(b)You run the following regression,where the numbers in parenthesis are homoskedasticity-only standard errors:  = 0.49- 0.10 Inft-1 - 0.39 △InfCt-1 - 0.33 △InfCt-2 - 0.21 △InfCt-3 + 0.05 △InfCt-4

= 0.49- 0.10 Inft-1 - 0.39 △InfCt-1 - 0.33 △InfCt-2 - 0.21 △InfCt-3 + 0.05 △InfCt-4

(0.28)(0.05)(0.09)(0.09)(0.09)(0.08)

Test for the presence of a stochastic trend.Should you have used heteroskedasticity-robust standard errors? Does the fact that you use quarterly data suggest including four lags in the above regression,or how should you determine the number of lags?

(c)To forecast the Canadian inflation rate for 2000:I,you estimate an AR(1),AR(4),and an ADL(4,1)model for the sample period 1962:I to 1999:IV.The results are as follows:  = 0.002 - 0.31 △InfCt-1

= 0.002 - 0.31 △InfCt-1

(0.014)(0.10)  = 0.021 - 0.46 ΔInfCt-1 - 0.39 ΔInfCt-2 - 0.25 ΔInfCt-3 + 0.03 ΔInfCt-4

= 0.021 - 0.46 ΔInfCt-1 - 0.39 ΔInfCt-2 - 0.25 ΔInfCt-3 + 0.03 ΔInfCt-4

(0.158)(0.10)(0.11)(0.08)(0.07)  = 1.279 - 0.51 ΔInfCt-1 - 0.44 ΔInfCt-2 - 0.30 ΔInfCt-3 - 0.02 ΔInfCt-4

= 1.279 - 0.51 ΔInfCt-1 - 0.44 ΔInfCt-2 - 0.30 ΔInfCt-3 - 0.02 ΔInfCt-4

(0.57)(0.10)(0.11)(0.09)(0.08)

- 0.16 UrateCt-1

(0.07)

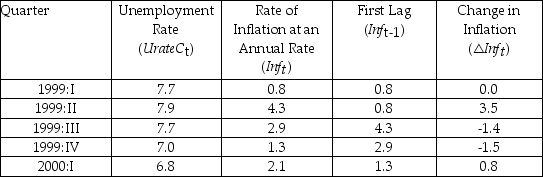

In addition,you have the following information on inflation in Canada during the four quarters of 1999 and the first quarter of 2000:

Inflation and Unemployment in Canada,First Quarter 1999 to First Quarter 2000

For each of the three models,calculate the predicted inflation rate for the period 2000:I and the forecast error.

For each of the three models,calculate the predicted inflation rate for the period 2000:I and the forecast error.

(d)Perform a test on whether or not Canadian unemployment rates Granger-cause the Canadian inflation rate.

Correct Answer:

Verified

(a)A small autocorrelation coefficient t...View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q3: The Bayes-Schwarz Information Criterion (BIC)is given by

Q4: Pseudo out of sample forecasting can be

Q5: The AR(p)model<br>A)is defined as Yt = β0

Q11: You have decided to use the Dickey

Q12: Negative autocorrelation in the change of a

Q12: The Akaike Information Criterion (AIC)is given by

Q13: (Requires Appendix material)Define the difference operator Δ

Q37: The formulae for the AIC and the

Q38: Statistical inference was a concept that was

Q46: You want to determine whether or not