Essay

(Requires Matrix Algebra)Consider the time and entity fixed effect model with a single explanatory variable

Yit = β0 + β1Xit +  D2i + ...+

D2i + ...+  Dni + δ2B2t + ...+ δTBTt + uit,

Dni + δ2B2t + ...+ δTBTt + uit,

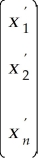

For the case of n = 4 and T = 3,write this model in the form Y = Xβ + U,where,in general,

Y =  ,U =

,U =  ,X =

,X =  =

=  ,and β =

,and β =  How would the X matrix change if you added two binary variables,D1 and B1? Demonstrate that in this case the columns of the X matrix are not independent.Finally show that elimination of one of the two variables is not sufficient to get rid of the multicollinearity problem.In terms of the OLS estimator,

How would the X matrix change if you added two binary variables,D1 and B1? Demonstrate that in this case the columns of the X matrix are not independent.Finally show that elimination of one of the two variables is not sufficient to get rid of the multicollinearity problem.In terms of the OLS estimator,  = (

= (  X)-1

X)-1  Y,why does perfect multicollinearity create a problem?

Y,why does perfect multicollinearity create a problem?

Correct Answer:

Verified

For the case of n = 4 and T = 3,the gene...View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q8: Assume that for the T = 2

Q19: Consider the regression example from your textbook,

Q27: Consider the time and entity fixed effect

Q28: A study,published in 1993,used U.S.state panel data

Q28: The difference between an unbalanced and a

Q31: In Sports Economics,production functions are often estimated

Q32: You want to study the relationship between

Q33: Consider a panel regression of unemployment rates

Q34: Consider the case of time fixed effects

Q35: If Xit is correlated with Xis for