Multiple Choice

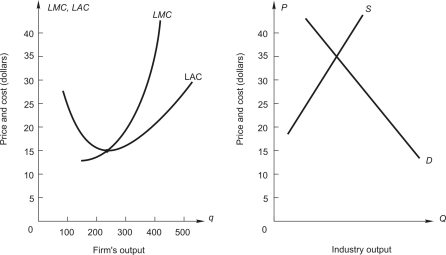

Below,the graph on the left shows long-run average and marginal cost for a typical firm in a perfectly competitive industry.The graph on the right shows demand and long-run supply for an increasing-cost industry.  If this were a constant-cost industry,what would be the price when the industry gets to long-run competitive equilibrium?

If this were a constant-cost industry,what would be the price when the industry gets to long-run competitive equilibrium?

A) between $35 and $20

B) $35

C) $20

D) below $20

E) above $35

Correct Answer:

Verified

Correct Answer:

Verified

Q62: Below,the graph on the left shows long-run

Q64: Consider a competitive industry and a price-taking

Q65: Which of the following is NOT a

Q67: Consider a competitive industry and a price-taking

Q68: Below,the graph on the left shows long-run

Q69: The table below shows a competitive firm's

Q70: A consulting company estimated market demand and

Q71: When a perfect competitive industry is in

Q93: In a competitive industry the market-determined price

Q97: Firm A and firm B both have