Deck 17: Time Series Forecasting and Index Numbers

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Assume that the current date is February 1, 2003. The linear regression model was applied to a monthly time series based on the last 24 months' sales (from January 2000 through December 2002). The following partial computer output summarizes the results.  Determine the predicted sales for this month.

Determine the predicted sales for this month.

A) 45.9

B) 42.7

C) 44.3

D) 109.1

E) 113.4

Determine the predicted sales for this month.A) 45.9

B) 42.7

C) 44.3

D) 109.1

E) 113.4

Question

Question

Question

Question

Assume that the current date is February 1, 2003. The linear regression model was applied to a monthly time series based on the last 24 months' sales (from January 2000 through December 2002). The following partial computer output summarizes the results.  At a significance level of .05, what is the value of the rejection point in testing the slope for significance?

At a significance level of .05, what is the value of the rejection point in testing the slope for significance?

A) 1.717

B) 1.96

C) 2.074

D) 1.645

E) 2.064

At a significance level of .05, what is the value of the rejection point in testing the slope for significance?A) 1.717

B) 1.96

C) 2.074

D) 1.645

E) 2.064

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

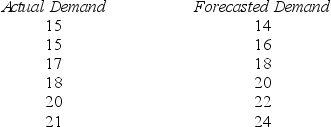

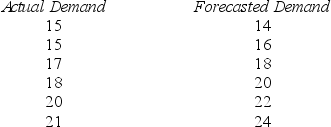

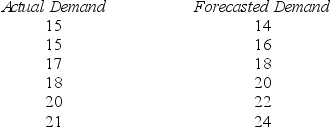

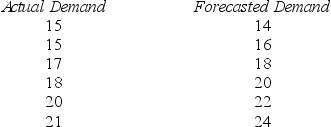

XYZ Company, Annual Data  Based on the information given in the table above, we can conclude that, in general,

Based on the information given in the table above, we can conclude that, in general,

A) the forecasting method is underestimating demand.

B) the forecasting method is overestimating demand.

C) we cannot determine whether the predictions are underestimating or overestimating demand.

Based on the information given in the table above, we can conclude that, in general,A) the forecasting method is underestimating demand.

B) the forecasting method is overestimating demand.

C) we cannot determine whether the predictions are underestimating or overestimating demand.

Question

Question

Question

XYZ Company, Annual Data  Based on the information given in the table above, what is the average forecast error?

Based on the information given in the table above, what is the average forecast error?

A) -1.3333

B) 1.6667

C) -2.5

D) -3.3333

E) 4.5

Based on the information given in the table above, what is the average forecast error?A) -1.3333

B) 1.6667

C) -2.5

D) -3.3333

E) 4.5

Question

Question

Question

Question

Question

Question

Question

XYZ Company, Annual Data  Based on the information given in the table above, what is the MSD?

Based on the information given in the table above, what is the MSD?

A) 1.3333

B) 1.6667

C) 2.5

D) 3.3333

E) 4.5

Based on the information given in the table above, what is the MSD?A) 1.3333

B) 1.6667

C) 2.5

D) 3.3333

E) 4.5

Question

Question

Question

Question

Question

XYZ Company, Annual Data  Based on the information given in the table above, what is the MAD?

Based on the information given in the table above, what is the MAD?

A) 1.3333

B) 1.6667

C) 2.5

D) 3.3333

E) 4.5

Based on the information given in the table above, what is the MAD?A) 1.3333

B) 1.6667

C) 2.5

D) 3.3333

E) 4.5

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/161

Play

Full screen (f)

Deck 17: Time Series Forecasting and Index Numbers

1

Removing the seasonal effect by dividing the actual time series observation by the estimated seasonal factor associated with the time series observation is called deseasonalization.

True

2

Exponential smoothing is a forecasting method that applies equal weights to the time series observations.

False

3

The smoothing constant is a number that determines how much weight is attached to each observation.

True

4

Holt-Winters double exponential smoothing would be an appropriate method to use to forecast a time series that exhibits a linear trend with no seasonal or cyclical patterns.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

5

A Paasche index more accurately provides a year-to-year comparison of the annual cost of selected products in the market basket than a Laspeyres index.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

6

The forecaster who uses MSD (mean squared deviations) to measure the effectiveness of forecasting methods would prefer method 1, which results in several smaller forecast errors, to method 2, which results in one large forecast error equal to the sum of the absolute values of several small forecast errors given by method 1.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

7

A positive autocorrelation implies that negative error terms will be followed by negative error terms.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

8

Cyclical variation exists when the magnitude of the seasonal swing does not depend on the level of a time series.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

9

When using moving averages to estimate the seasonal factors, we need to compute the centered moving average if there is an odd number of seasons.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

10

Dummy variables are used to model increasing seasonal variation.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

11

Simple exponential smoothing is an appropriate method for prediction purposes when there is a significant trend present in a time series.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

12

While a simple index is calculated by using the values of one time series, an aggregate index is computed based on the accumulated values of more than one time series.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

13

When deseasonalizing a time series observation, the actual time series observation is divided by its seasonal factor.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

14

A time series decomposition method would not be used to forecast seasonal data.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

15

A simple exponential forecasting method would not be used to forecast seasonal data.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

16

A univariate time series model is used to predict future values of a time series based only upon past values of a time series.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

17

Dummy variable regression would be an appropriate method to use to forecast a time series that exhibits a linear trend with no seasonal or cyclical patterns.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

18

Trend refers to a long-run upward or downward movement of a time series over a period of time.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

19

The simple moving average method is primarily useful in determining the impact of trend on a time series.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

20

Forecasters using a multiplicative decomposition model or time series regression model, assume that the time series components are changing over time.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

21

Simple exponential smoothing is a forecasting method that applies equal weights to the time series observations.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

22

When a forecaster uses the ________ method, she or he assumes that the time series components are changing slowly over time.

A) time series regression

B) exponential smoothing

C) index number

D) multiplicative decomposition

A) time series regression

B) exponential smoothing

C) index number

D) multiplicative decomposition

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

23

Seasonal variations are periodic patterns in a time series that must last at least one year.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

24

In the Durbin-Watson test, if the calculated d-statistic is greater than the upper value of the d-statistic, then

A) we do not reject H0, which says the error terms are not autocorrelated.

B) we do reject H0, which says the error terms are not autocorrelated.

C) the test is inconclusive.

D) we do reject H0, which says the error terms are positively or negatively autocorrelated.

A) we do not reject H0, which says the error terms are not autocorrelated.

B) we do reject H0, which says the error terms are not autocorrelated.

C) the test is inconclusive.

D) we do reject H0, which says the error terms are positively or negatively autocorrelated.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

25

Exponential smoothing is designed to forecast time series described by regular and seasonal components that are always changing over time.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

26

The no-trend time series model is given by

A) TRt = β0 + β1t.

B) TRt = β0.

C) TRt = β0 + β1t + β2t2.

D) TRt = β0 + βln(t).

A) TRt = β0 + β1t.

B) TRt = β0.

C) TRt = β0 + β1t + β2t2.

D) TRt = β0 + βln(t).

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

27

All of the following are forecasting methods except

A) Holt-Winters double exponential smoothing.

B) simple exponential smoothing.

C) time series regression.

D) MAD autocorrelation.

A) Holt-Winters double exponential smoothing.

B) simple exponential smoothing.

C) time series regression.

D) MAD autocorrelation.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

28

Causal variables can be used in forecasting models.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

29

Box-Jenkins methodology is a more sophisticated approach to forecasting a time series with components that might be changing over time.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

30

If the errors produced by a forecasting method for 3 observations are −1, −2, and −6, then what is the mean squared error or deviation?

A) 9

B) −9

C) 3

D) 13.67

A) 9

B) −9

C) 3

D) 13.67

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

31

If the errors produced by a forecasting method for 3 observations are +3, +3, and −3, then what is the mean squared error?

A) 9

B) 0

C) 3

D) −3

E) 2

A) 9

B) 0

C) 3

D) −3

E) 2

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

32

If the errors produced by a forecasting method for 3 observations are +3, +3, and −3, then what is the mean absolute deviation?

A) 9

B) 0

C) 3

D) −3

A) 9

B) 0

C) 3

D) −3

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

33

Random shock is a value that is assumed to have been randomly selected that is the same for each and every time period.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

34

When a forecaster uses the ________ method, she or he assumes that the time series components are changing quickly over time.

A) time series regression

B) simple exponential smoothing

C) Box-Jenkins

D) multiplicative decomposition

A) time series regression

B) simple exponential smoothing

C) Box-Jenkins

D) multiplicative decomposition

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

35

Three criteria used to compare two forecasting methods are the mean absolute deviation, the mean squared deviation, and the mean absolute percentage error.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

36

The multiplicative Winters method is used to forecast time series when there are no seasonal factors that are part of the model.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

37

The Box-Jenkins methodology can be used to identify what is called an autoregressive-moving average model.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following is not a component of time series?

A) trend

B) seasonal

C) cyclical

D) irregular

E) smoothing constant

A) trend

B) seasonal

C) cyclical

D) irregular

E) smoothing constant

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

39

The multiplicative Winters method used to forecast time series applies a seasonal factor SNT to the forecasting model.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

40

Multiplicative decompositions assume that time series components remain essentially constant over time.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

41

The ________ component of a time series refers to the erratic time series movements that follow no recognizable or regular pattern.

A) trend

B) seasonal

C) cyclical

D) irregular

A) trend

B) seasonal

C) cyclical

D) irregular

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

42

The ________ component of a time series measures the fluctuations in a time series due to economic conditions of prosperity and recession with a duration of approximately 2 years or longer.

A) trend

B) seasonal

C) cyclical

D) irregular

A) trend

B) seasonal

C) cyclical

D) irregular

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

43

Seasonal variations are periodic patterns in a time series that are repeated over time. For which one of the following time series variables is it not possible to recognize seasonal variations?

A) quarters of the year

B) months of the year

C) days of the week

D) hours of the day

E) years

A) quarters of the year

B) months of the year

C) days of the week

D) hours of the day

E) years

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

44

A major drawback of the aggregate price index is that

A) it does not take into account the fact that some items in the market basket are purchased more frequently than others.

B) it is difficult to compute.

C) it is computed by using the values from a single time series or based on a single product.

D) percentage comparisons cannot be made to the base year.

A) it does not take into account the fact that some items in the market basket are purchased more frequently than others.

B) it is difficult to compute.

C) it is computed by using the values from a single time series or based on a single product.

D) percentage comparisons cannot be made to the base year.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

45

Suppose that the unadjusted seasonal factor for the month of April is 1.10. The sum of the 12 months' unadjusted seasonal factor values is 12.18. The normalized (adjusted) seasonal factor value for April

A) is larger than 1.1.

B) is smaller than 1.1.

C) is equal to 1.1.

D) cannot be determined with the information provided.

A) is larger than 1.1.

B) is smaller than 1.1.

C) is equal to 1.1.

D) cannot be determined with the information provided.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

46

The ________ component of a time series consists of erratic and unsystematic fluctuations in the time series data.

A) trend

B) seasonal

C) cyclical

D) irregular

A) trend

B) seasonal

C) cyclical

D) irregular

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

47

A sustained long-term change in the level of the variable that is being forecasted per unit of time is

A) a trend.

B) a time series.

C) seasonality.

D) a change due to business cycles.

A) a trend.

B) a time series.

C) seasonality.

D) a change due to business cycles.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

48

Assume that the current date is February 1, 2003. The linear regression model was applied to a monthly time series based on the last 24 months' sales (from January 2000 through December 2002). The following partial computer output summarizes the results. Determine the predicted sales for this month.

A) 45.9

B) 42.7

C) 44.3

D) 109.1

E) 113.4

Determine the predicted sales for this month.A) 45.9

B) 42.7

C) 44.3

D) 109.1

E) 113.4

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

49

A sequence of values of some variable or composite of variables taken at successive, uninterrupted time periods is called a

A) least squares (linear) trend line.

B) moving average.

C) cyclical component.

D) time series.

E) seasonal factor.

A) least squares (linear) trend line.

B) moving average.

C) cyclical component.

D) time series.

E) seasonal factor.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

50

When the moving average method is used to estimate the seasonal factors with quarterly sales data, a(n) ________ period moving average is used.

A) 2

B) 3

C) 4

D) 5

E) 8

A) 2

B) 3

C) 4

D) 5

E) 8

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

51

Which of the following time series forecasting methods would not be used to forecast a time series that exhibits a linear trend with no seasonal or cyclical patterns?

A) dummy variable regression

B) linear trend regression

C) Holt-Winters double exponential smoothing

D) multiplicative Winters method

E) both dummy variable regression and multiplicative Winters method

A) dummy variable regression

B) linear trend regression

C) Holt-Winters double exponential smoothing

D) multiplicative Winters method

E) both dummy variable regression and multiplicative Winters method

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

52

Assume that the current date is February 1, 2003. The linear regression model was applied to a monthly time series based on the last 24 months' sales (from January 2000 through December 2002). The following partial computer output summarizes the results. At a significance level of .05, what is the value of the rejection point in testing the slope for significance?

A) 1.717

B) 1.96

C) 2.074

D) 1.645

E) 2.064

At a significance level of .05, what is the value of the rejection point in testing the slope for significance?A) 1.717

B) 1.96

C) 2.074

D) 1.645

E) 2.064

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

53

In general, the number of dummy variables used to model constant seasonal variation is equal to the number of

A) seasons.

B) seasons minus 1.

C) seasons plus 1.

D) seasons minus 2.

E) seasons divided by two.

A) seasons.

B) seasons minus 1.

C) seasons plus 1.

D) seasons minus 2.

E) seasons divided by two.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

54

The ________ component of a time series reflects the long-run decline or growth in a time series.

A) trend

B) seasonal

C) cyclical

D) irregular

A) trend

B) seasonal

C) cyclical

D) irregular

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

55

When the magnitude of the seasonal swing does not depend on the level of a time series, we call this ________ variation.

A) increasing seasonal

B) cyclical seasonal

C) constant seasonal

D) decreasing seasonal

E) no seasonal

A) increasing seasonal

B) cyclical seasonal

C) constant seasonal

D) decreasing seasonal

E) no seasonal

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

56

Since a(n) ________ index employs the base-period quantities in all succeeding periods, it allows for ready comparisons for identical quantities of goods purchased between the base period and all succeeding periods.

A) simple

B) aggregate

C) Laspeyres

D) Paasche

E) quantity

A) simple

B) aggregate

C) Laspeyres

D) Paasche

E) quantity

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

57

Which of the following time series forecasting methods would not be used to forecast seasonal data?

A) dummy variable regression

B) simple exponential smoothing

C) time series decomposition

D) multiplicative Winters method

A) dummy variable regression

B) simple exponential smoothing

C) time series decomposition

D) multiplicative Winters method

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

58

Those fluctuations that are associated with climate, holidays, and related activities are referred to as ________ variations.

A) trend

B) seasonal

C) cyclical

D) irregular

A) trend

B) seasonal

C) cyclical

D) irregular

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

59

A restaurant has been experiencing higher sales during the weekends, compared to the weekdays. Daily restaurant sales patterns for this restaurant over a week are an example of a(n) ________ component of a time series.

A) trend

B) seasonal

C) cyclical

D) irregular

A) trend

B) seasonal

C) cyclical

D) irregular

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

60

In the multiplicative decomposition method, the centered moving averages provide an estimate of

A) trend × seasonal.

B) trend × cycle.

C) seasonal × cycle.

D) trend × irregular.

E) seasonal × irregular.

A) trend × seasonal.

B) trend × cycle.

C) seasonal × cycle.

D) trend × irregular.

E) seasonal × irregular.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

61

When there is ________ seasonal variation, the magnitude of the seasonal swing does not depend on the level of the time series.

A) cyclical

B) constant

C) irregular

D) increasing

A) cyclical

B) constant

C) irregular

D) increasing

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

62

A forecasting method that weights recent observations more heavily is called ________.

A) time series analysis

B) first-order autocorrelation

C) multiplicative decomposition

D) exponential smoothing

A) time series analysis

B) first-order autocorrelation

C) multiplicative decomposition

D) exponential smoothing

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

63

The demand for a product for the last six years has been 15, 15, 17, 18, 20, and 19. The manager wants to predict the demand for this time series using the following simple linear trend equation: trt = 12 + 2t. Use this equation to forecast the demand for this product, and then calculate the MAD.

A) MAD = 1.333

B) MAD = 1.6

C) MAD = 2.0

D) MAD = 2.333

E) MAD = 2.5

A) MAD = 1.333

B) MAD = 1.6

C) MAD = 2.0

D) MAD = 2.333

E) MAD = 2.5

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

64

XYZ Company, Annual Data Based on the information given in the table above, we can conclude that, in general,

A) the forecasting method is underestimating demand.

B) the forecasting method is overestimating demand.

C) we cannot determine whether the predictions are underestimating or overestimating demand.

Based on the information given in the table above, we can conclude that, in general,A) the forecasting method is underestimating demand.

B) the forecasting method is overestimating demand.

C) we cannot determine whether the predictions are underestimating or overestimating demand.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

65

In a given week, the NYSE (New York Stock Exchange) is generally open from Monday through Friday. If we wanted to use the multiple regression method with dummy variables to study the impact of the day of the week on stock market performance, we would need ________ dummy variables.

A) 5

B) 52

C) 4

D) 3

E) 365

A) 5

B) 52

C) 4

D) 3

E) 365

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

66

Weighting in exponential smoothing is accomplished by using ________.

A) first-order autocorrelation

B) smoothing constants

C) the Durbin-Watson method

D) multiplicative decomposing

A) first-order autocorrelation

B) smoothing constants

C) the Durbin-Watson method

D) multiplicative decomposing

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

67

XYZ Company, Annual Data Based on the information given in the table above, what is the average forecast error?

A) -1.3333

B) 1.6667

C) -2.5

D) -3.3333

E) 4.5

Based on the information given in the table above, what is the average forecast error?A) -1.3333

B) 1.6667

C) -2.5

D) -3.3333

E) 4.5

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

68

The demand for a product for the last six years has been 15, 15, 17, 18, 20, and 19. The manager wants to predict the demand for this time series using the following simple linear trend equation: trt = 12 + 2t. What are the forecast errors for the 5th and 6th years?

A) 0, −3

B) 0, +3

C) +2, +5

D) −2, −5

E) −1, −4

A) 0, −3

B) 0, +3

C) +2, +5

D) −2, −5

E) −1, −4

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

69

The purpose behind moving averages and centered moving averages is to eliminate ________.

A) constant variation

B) cyclical variation

C) seasonal variation

D) regular variation

A) constant variation

B) cyclical variation

C) seasonal variation

D) regular variation

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

70

The upward or downward movement that characterizes a time series over a period of time is referred to as ________.

A) seasonal variation

B) cyclical variation

C) a trend

D) irregular variation

A) seasonal variation

B) cyclical variation

C) a trend

D) irregular variation

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

71

When using simple exponential smoothing, the value of the smoothing constant α cannot be

A) negative.

B) greater than zero.

C) greater than 1.

D) .99.

E) negative or greater than 1.

A) negative.

B) greater than zero.

C) greater than 1.

D) .99.

E) negative or greater than 1.

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

72

The ________ test is a test for first-order positive autocorrelation.

A) Durbin-Watson

B) MSD

C) MAD

D) multiplicative Winters

A) Durbin-Watson

B) MSD

C) MAD

D) multiplicative Winters

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

73

When there is first-order autocorrelation, the error term in period t is related to the error term in period ________.

A) t

B) t + 1

C) t − 1

D) t − 2

A) t

B) t + 1

C) t − 1

D) t − 2

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

74

XYZ Company, Annual Data Based on the information given in the table above, what is the MSD?

A) 1.3333

B) 1.6667

C) 2.5

D) 3.3333

E) 4.5

Based on the information given in the table above, what is the MSD?A) 1.3333

B) 1.6667

C) 2.5

D) 3.3333

E) 4.5

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

75

Periodic patterns in time series that repeat themselves within a calendar year or less are referred to as ________.

A) constant variations

B) cyclical variations

C) seasonal variations

D) regular variations

A) constant variations

B) cyclical variations

C) seasonal variations

D) regular variations

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

76

The Holt-Winters double exponential smoothing method is used to forecast time series data with ________.

A) autocorrelation

B) a linear trend

C) cyclical patterns

D) moving averages

A) autocorrelation

B) a linear trend

C) cyclical patterns

D) moving averages

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

77

The demand for a product for the last six years has been 15, 15, 17, 18, 20, and 19. The manager wants to predict the demand for this time series using the following simple linear trend equation: trt = 12 + 2t. Use this equation to forecast the demand for this product, and then calculate the MSD.

A) MSD = 6

B) MSD = 3.3333

C) MSD = 7.0

D) MSD = 2

E) MSD = 2.4

A) MSD = 6

B) MSD = 3.3333

C) MSD = 7.0

D) MSD = 2

E) MSD = 2.4

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

78

The recurring up-and-down movement of a time series around trend levels that last more than one calendar year is called ________.

A) constant variation

B) cyclical variation

C) seasonal variation

D) irregular variation

A) constant variation

B) cyclical variation

C) seasonal variation

D) irregular variation

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

79

XYZ Company, Annual Data Based on the information given in the table above, what is the MAD?

A) 1.3333

B) 1.6667

C) 2.5

D) 3.3333

E) 4.5

Based on the information given in the table above, what is the MAD?A) 1.3333

B) 1.6667

C) 2.5

D) 3.3333

E) 4.5

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

80

The Durbin-Watson statistic is used to detect ________.

A) first-order autocorrelation

B) exponential smoothing

C) multiplicative decomposing

D) irregular variation

A) first-order autocorrelation

B) exponential smoothing

C) multiplicative decomposing

D) irregular variation

Unlock Deck

Unlock for access to all 161 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 161 flashcards in this deck.