Deck 11: Auto-Correlation

Full screen (f)

Question

Question

The second stage of the Durbin-Watson test for the presence of autocorrelation is to

A)regress the current period residuals on the residuals lagged one period.

B)regress the residuals lagged one period on the current period residuals.

C)calculate the test statistic

D)calculate the test statistic

A)regress the current period residuals on the residuals lagged one period.

B)regress the residuals lagged one period on the current period residuals.

C)calculate the test statistic

D)calculate the test statistic

Question

Question

Question

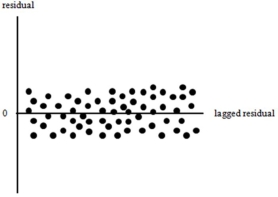

Suppose that you plot the residuals from a regression of Number of Wins on Payroll for the Dallas Cowboys over the last 20 years and you get the following

You would conclude that

A)definitely autocorrelated.

B)likely not autocorrelated.

C)possibly autocorrelated and you would perform a formal test for heteroskedasticity.

D)possibly autocorrelated and you would always perform a correction for autocorrelation.

You would conclude that

A)definitely autocorrelated.

B)likely not autocorrelated.

C)possibly autocorrelated and you would perform a formal test for heteroskedasticity.

D)possibly autocorrelated and you would always perform a correction for autocorrelation.

Question

Question

Question

Question

Question

Question

Question

An AR(2)process is written as

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

An AR(1,6)process is written as

A)

B)

C)

D)

A)

B)

C)

D)

Question

An AR(1)process is written as

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

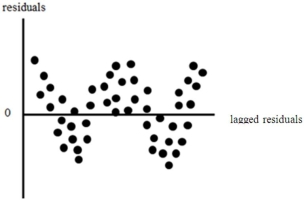

Suppose that you plot the residuals from a regression of GDP on the unemployment rate and you get the following

You would conclude that the error terms are

A)definitely autocorrelated.

B)likely not autocorrelated.

C)possibly autocorrelated and you would perform a formal test for autocorrelation.

D)possibly autocorrelated and you would perform a correction for heteroskedasticity.

You would conclude that the error terms are

A)definitely autocorrelated.

B)likely not autocorrelated.

C)possibly autocorrelated and you would perform a formal test for autocorrelation.

D)possibly autocorrelated and you would perform a correction for heteroskedasticity.

Question

Question

The third step of the Regression test for AR(1)is to estimate the model

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Iterations in the Cochrane-Orcutt method for AR(1)should be continued until

A)

B)

C) changes by .05 between iterations.

changes by .05 between iterations.

D) is stable between iterations.

is stable between iterations.

A)

B)

C)

changes by .05 between iterations.D)

is stable between iterations. Question

Suppose that you are performing the Regression test for AR(1)and you get (standard errors in parentheses)with 50 observations

You would conclude that

A)autocorrelation is not present in the data.

B)autocorrelation is present in the data.

C)heteroskedasticity is not present in the data.

D)heteroskedasticity is present in the data.

You would conclude that

A)autocorrelation is not present in the data.

B)autocorrelation is present in the data.

C)heteroskedasticity is not present in the data.

D)heteroskedasticity is present in the data.

Question

The third step in the first iteration of the Cochrane-Orcutt method for AR(1)is to

A)use the estimate of to adjust the dependent variable.

to adjust the dependent variable.

B)use the estimate of to adjust the independent variables.

to adjust the independent variables.

C)use the estimate of to adjust the dependent variable and the independent variables.

to adjust the dependent variable and the independent variables.

D)use the estimate of and

and  to adjust the dependent variable and the independent variables.

to adjust the dependent variable and the independent variables.

A)use the estimate of

to adjust the dependent variable.B)use the estimate of

to adjust the independent variables.C)use the estimate of

to adjust the dependent variable and the independent variables.D)use the estimate of

and to adjust the dependent variable and the independent variables. Question

Question

Question

Question

Question

A potential shortcoming of the Cochrane-Orcutt method for AR(1)is that it

A)drops the first the first two observations.

B)drops the first observation.

C)does not typcially estimate correctly.

correctly.

D) no longer changes between iterations.

no longer changes between iterations.

A)drops the first the first two observations.

B)drops the first observation.

C)does not typcially estimate

correctly.D)

no longer changes between iterations. Question

The second step in the first iteration of the Cochrane-Orcutt method for AR(1)is to estimate the model

A) to generate an estimate of

to generate an estimate of  .

.

B) to generate an estimate of

to generate an estimate of  .

.

C) to generate an estimate of

to generate an estimate of  and

and  .

.

D) to generate an estimate of

to generate an estimate of  .

.

A)

to generate an estimate of .B)

to generate an estimate of .C)

to generate an estimate of and .D)

to generate an estimate of . Question

The second iteration of the Cochrane-Orcutt method for AR(1)involves

A)repeating the process in the first iteration for the data adjusted by and

and  .

.

B)repeating the process in the first iteration for the data adjusted by .

.

C)re-estimating following the process in the first iteration.

following the process in the first iteration.

D)re-estimating using the data lagged one period.

using the data lagged one period.

A)repeating the process in the first iteration for the data adjusted by

and .B)repeating the process in the first iteration for the data adjusted by

.C)re-estimating

following the process in the first iteration.D)re-estimating

using the data lagged one period. Question

Question

The Prais-Winsten procedure for AR(1)improves on the Cochrane-Orcutt method for AR(1)by

A)incorporating estimates of the first observation only in the first iteration.

B)incorporating estimates of the first observation in all iterations.

C)generating an estimate of that actually equals ρ.

that actually equals ρ.

D)reducing the required number of iterations.

A)incorporating estimates of the first observation only in the first iteration.

B)incorporating estimates of the first observation in all iterations.

C)generating an estimate of

that actually equals ρ.D)reducing the required number of iterations.

Question

Question

Question

Suppose you are interested in explaining variation in quarterly Net Exports (billions)and that you estimate the regression function (standard errors in parentheses)

a)How many years' worth of data do you have? How can you tell? Explain.

b)Do you suspect that autocorrelation might be present in this model? If so,what type? Why? Explain.

c)How would you use the Regression test for AR(1)to determine whether autocorrelation is present? Explain.

d)Suppose you know that the autocorrelation follows an AR(1)process.How would you use the Prais-Winsten method to correct for the autocorrelation? Explain.

e)When using the Prais-Winsten method,how many observations will you have in your final analysis? Why? Explain.

a)How many years' worth of data do you have? How can you tell? Explain.

b)Do you suspect that autocorrelation might be present in this model? If so,what type? Why? Explain.

c)How would you use the Regression test for AR(1)to determine whether autocorrelation is present? Explain.

d)Suppose you know that the autocorrelation follows an AR(1)process.How would you use the Prais-Winsten method to correct for the autocorrelation? Explain.

e)When using the Prais-Winsten method,how many observations will you have in your final analysis? Why? Explain.

Question

Question

Question

Suppose you are interested in explaining variation in monthly Ice Cream consumption (thousands of gallons)and that you estimate the regression function (standard errors in parentheses)

a)How many years' worth of data do you have? How can you tell? Explain.

b)Do you suspect that autocorrelation might be present in this model? If so,what type? Why? Explain.

c)How would you use the Durbin-Watson test to determine whether autocorrelation is present? Explain.What type of autoregressive process does the Durbin-Watson test work for?

d)Suppose you know that the autocorrelation follows an AR(1)process.How would you use the Cochrane-Orcutt method to correct for the autocorrelation? Explain.

e)When using the Cochrane-Orcutt method,how many observations will you have in your final analysis? Why? Explain.

a)How many years' worth of data do you have? How can you tell? Explain.

b)Do you suspect that autocorrelation might be present in this model? If so,what type? Why? Explain.

c)How would you use the Durbin-Watson test to determine whether autocorrelation is present? Explain.What type of autoregressive process does the Durbin-Watson test work for?

d)Suppose you know that the autocorrelation follows an AR(1)process.How would you use the Cochrane-Orcutt method to correct for the autocorrelation? Explain.

e)When using the Cochrane-Orcutt method,how many observations will you have in your final analysis? Why? Explain.

Question

Question

Question

Question

Suppose you are interested in explaining variation in annual Defense Spending (billions)and that you estimate the regression function (standard errors in parentheses)

a)How many years' worth of data do you have? How can you tell? Explain.

b)Do you suspect that autocorrelation might be present in this model? If so,what type? Why? Explain.

c)How would you use the Regression test for AR(2)to determine whether autocorrelation is present? Explain.

d)What is the preferred method of correct for potential autocorrelation? Why is it preferred? Explain.

Suppose you are interested in explaining variation in annual Defense Spending (billions)and that you estimate the sample regression function (standard errors in parentheses)

a)How many years' worth of data do you have? How can you tell? Explain.

b)Do you suspect that autocorrelation might be present in this model? If so,what type? Why? Explain.

c)How would you use the Regression test for AR(2)to determine whether autocorrelation is present? Explain.

d)What is the preferred method of correct for potential autocorrelation? Why is it preferred? Explain.

Suppose you are interested in explaining variation in annual Defense Spending (billions)and that you estimate the sample regression function (standard errors in parentheses)

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/50

Play

Full screen (f)

Deck 11: Auto-Correlation

1

The autoregressive structure of the error term is the current-period error term and

A)the dependent variable.

B)the independent variables.

C)prior-period error terms.

D)future-period error terms.

A)the dependent variable.

B)the independent variables.

C)prior-period error terms.

D)future-period error terms.

C

2

The second stage of the Durbin-Watson test for the presence of autocorrelation is to

A)regress the current period residuals on the residuals lagged one period.

B)regress the residuals lagged one period on the current period residuals.

C)calculate the test statistic

D)calculate the test statistic

A)regress the current period residuals on the residuals lagged one period.

B)regress the residuals lagged one period on the current period residuals.

C)calculate the test statistic

D)calculate the test statistic

D

3

Because it violates time-series assumption ____,autocorrelation results in estimates that are ____.

A)T6;biased

B)T6;inefficient

C)T6;unbiased

D)T4;inefficient

A)T6;biased

B)T6;inefficient

C)T6;unbiased

D)T4;inefficient

B

4

Autoregressive error terms are potentially problematic because they result in

A)biased parameter estimates.

B)estimated standard errors that are incorrect.

C)estimated standard errors that are always too small.

D)incorrect estimated slope coefficients.

A)biased parameter estimates.

B)estimated standard errors that are incorrect.

C)estimated standard errors that are always too small.

D)incorrect estimated slope coefficients.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

5

Suppose that you plot the residuals from a regression of Number of Wins on Payroll for the Dallas Cowboys over the last 20 years and you get the following

You would conclude that

A)definitely autocorrelated.

B)likely not autocorrelated.

C)possibly autocorrelated and you would perform a formal test for heteroskedasticity.

D)possibly autocorrelated and you would always perform a correction for autocorrelation.

You would conclude that

A)definitely autocorrelated.

B)likely not autocorrelated.

C)possibly autocorrelated and you would perform a formal test for heteroskedasticity.

D)possibly autocorrelated and you would always perform a correction for autocorrelation.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

6

A simple method for determining whether autocorrelation is present in a given data set is to

A)construct a histogram.

B)calculate the variance of the sample.

C)examine the residual plot.

D)plot the data points from smallest to largest.

A)construct a histogram.

B)calculate the variance of the sample.

C)examine the residual plot.

D)plot the data points from smallest to largest.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

7

Autocorrelation occurs when

A)an omitted independent variable is correlated with the error term.

B)the error term is correlated across different time-periods.

C)the error term has a non-constant variance.

D)the error term is,on average,equal to zero.

A)an omitted independent variable is correlated with the error term.

B)the error term is correlated across different time-periods.

C)the error term has a non-constant variance.

D)the error term is,on average,equal to zero.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

8

The most likely violation of the assumptions required for OLS to be BLUE when dealing with time-series data is referred to as

A)heteroskedasticity.

B)homeskedasticity.

C)autocorrelation.

D)autoskedasticity.

A)heteroskedasticity.

B)homeskedasticity.

C)autocorrelation.

D)autoskedasticity.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

9

Autocorrelation is a problem because it causes the

A)estimated slope coefficients to be biased.

B)estimated standard errors to be incorrect.

C)data to be spuriously correlated.

D)estimated standard errors to always be too small.

A)estimated slope coefficients to be biased.

B)estimated standard errors to be incorrect.

C)data to be spuriously correlated.

D)estimated standard errors to always be too small.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

10

Autocorrelation violates the time-series assumption

A)T3.

B)T4.

C)T5.

D)T6.

A)T3.

B)T4.

C)T5.

D)T6.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

11

The null hypothesis for testing for the presence of autocorrelation is

A)the error terms are correlated over time.

B)the error terms are not correlated over time.

C)the error terms follow an AR(1)process.

D)the error terms have constant variance over time.

A)the error terms are correlated over time.

B)the error terms are not correlated over time.

C)the error terms follow an AR(1)process.

D)the error terms have constant variance over time.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

12

An AR(2)process is written as

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

13

The first step of the Durbin-Watson test for the presence of autocorrelation is to estimate the model and determine

A)the current period residuals.

B)the residuals lagged one period.

C)the current period residuals and the residuals lagged one period.

D)the current period residuals,the residuals lagged one period,and the residuals lagged two periods.

A)the current period residuals.

B)the residuals lagged one period.

C)the current period residuals and the residuals lagged one period.

D)the current period residuals,the residuals lagged one period,and the residuals lagged two periods.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

14

An AR(1,6)process is written as

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

15

An AR(1)process is written as

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

16

If autocorrelation is not present,then the Durbin-Watson test statistic will be

A)near 0.

B)near 2.

C)near 4.

D)between 0 and 1.

A)near 0.

B)near 2.

C)near 4.

D)between 0 and 1.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

17

Suppose that you plot the residuals from a regression of GDP on the unemployment rate and you get the following

You would conclude that the error terms are

A)definitely autocorrelated.

B)likely not autocorrelated.

C)possibly autocorrelated and you would perform a formal test for autocorrelation.

D)possibly autocorrelated and you would perform a correction for heteroskedasticity.

You would conclude that the error terms are

A)definitely autocorrelated.

B)likely not autocorrelated.

C)possibly autocorrelated and you would perform a formal test for autocorrelation.

D)possibly autocorrelated and you would perform a correction for heteroskedasticity.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

18

If positive autocorrelation is not present,then the Durbin-Watson test statistic will be

A)closer to 0.

B)closer to 2.

C)closer to 4.

D)greater than 3.

A)closer to 0.

B)closer to 2.

C)closer to 4.

D)greater than 3.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

19

The third step of the Regression test for AR(1)is to estimate the model

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

20

The first step of the Regression test for the presence of AR(1)is to estimate the model and determine

A)the current period squared residuals.

B)the residuals lagged one period.

C)the current period residuals and the residuals lagged one period.

D)the current period residuals,the residuals lagged one period,and the residuals lagged two periods.

A)the current period squared residuals.

B)the residuals lagged one period.

C)the current period residuals and the residuals lagged one period.

D)the current period residuals,the residuals lagged one period,and the residuals lagged two periods.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

21

The final step of the Regression test for AR(1)is to perform

A)an F-test for the joint significance of ρ1 and ρ2.

B)an F-test for the overall significance of the xt and et - 1.

C)a t-test for the individual significance of ρ.

D)separate t-tests for the individual significance of ρ1 and ρ2.

A)an F-test for the joint significance of ρ1 and ρ2.

B)an F-test for the overall significance of the xt and et - 1.

C)a t-test for the individual significance of ρ.

D)separate t-tests for the individual significance of ρ1 and ρ2.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

22

In order to perform cointegration,you need to identify

A)a second independent variable that is correlated with the dependent variable but uncorrelated with the first independent variable.

B)an independent variable that moves with the dependent variable and produces residuals that are I(0)when the dependent variable is regressed on it.

C)an independent variable that moves with the dependent variable and produces residuals that are I(1)when the dependent variable is regressed on it.

D)an independent variable that moves with the dependent variable and produces non-stationary residuals.

A)a second independent variable that is correlated with the dependent variable but uncorrelated with the first independent variable.

B)an independent variable that moves with the dependent variable and produces residuals that are I(0)when the dependent variable is regressed on it.

C)an independent variable that moves with the dependent variable and produces residuals that are I(1)when the dependent variable is regressed on it.

D)an independent variable that moves with the dependent variable and produces non-stationary residuals.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

23

What are the null and alternative hypotheses for testing for the presence of AR(1)autocorrelation? Why? Explain.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

24

Write out the model for an AR(1)process.Explain what it means.Repeat for an AR(2)process.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

25

You can determine whether a unit root exists by performing

A)a Newey-West test.

B)a Cochrane-Orcutt test.

C)a Prais-Winsten test.

D)a Dickey-Fuller test.

A)a Newey-West test.

B)a Cochrane-Orcutt test.

C)a Prais-Winsten test.

D)a Dickey-Fuller test.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

26

The Cochrane-Orcutt method is

A)an iterative process for determining whether autocorrelation exists.

B)an iterative process for correcting for the presence of autocorrelation.

C)a one-step process for determining whether autocorrelation exists.

D)a one-step process for correcting for the presence of heteroskedasticity.

A)an iterative process for determining whether autocorrelation exists.

B)an iterative process for correcting for the presence of autocorrelation.

C)a one-step process for determining whether autocorrelation exists.

D)a one-step process for correcting for the presence of heteroskedasticity.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

27

How do you perform the Durbin-Watson test for autocorrelation? Explain.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

28

If a unit root exists,then

A)there is no issue with estimating time-series models.

B)steps must be taken to make the time-series a stable AR(1).

C)it is impossible to model the AR(1)process.

D)the time-series is not an AR(1)process.

A)there is no issue with estimating time-series models.

B)steps must be taken to make the time-series a stable AR(1).

C)it is impossible to model the AR(1)process.

D)the time-series is not an AR(1)process.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

29

Iterations in the Cochrane-Orcutt method for AR(1)should be continued until

A)

B)

C) changes by .05 between iterations.

D) is stable between iterations.

A)

B)

C)

changes by .05 between iterations.D)

is stable between iterations. Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

30

Suppose that you are performing the Regression test for AR(1)and you get (standard errors in parentheses)with 50 observations

You would conclude that

A)autocorrelation is not present in the data.

B)autocorrelation is present in the data.

C)heteroskedasticity is not present in the data.

D)heteroskedasticity is present in the data.

You would conclude that

A)autocorrelation is not present in the data.

B)autocorrelation is present in the data.

C)heteroskedasticity is not present in the data.

D)heteroskedasticity is present in the data.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

31

The third step in the first iteration of the Cochrane-Orcutt method for AR(1)is to

A)use the estimate of to adjust the dependent variable.

B)use the estimate of to adjust the independent variables.

C)use the estimate of to adjust the dependent variable and the independent variables.

D)use the estimate of and to adjust the dependent variable and the independent variables.

A)use the estimate of

to adjust the dependent variable.B)use the estimate of

to adjust the independent variables.C)use the estimate of

to adjust the dependent variable and the independent variables.D)use the estimate of

and to adjust the dependent variable and the independent variables. Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

32

Newey-West robust standard errors

A)the preferred method for correcting for potential autocorrelation.

B)calculated through an iterative process.

C)automatically calculated in Excel.

D)the result of performing the Prais-Winsten method.

A)the preferred method for correcting for potential autocorrelation.

B)calculated through an iterative process.

C)automatically calculated in Excel.

D)the result of performing the Prais-Winsten method.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

33

The first step in the first iteration of the Cochrane-Orcutt method for AR(1)is to estimate the model and determine

A)the current period residuals.

B)the residuals lagged one period.

C)the current period residuals and the residuals lagged one period.

D)the current period residuals,the residuals lagged one period,and the residuals lagged two periods.

A)the current period residuals.

B)the residuals lagged one period.

C)the current period residuals and the residuals lagged one period.

D)the current period residuals,the residuals lagged one period,and the residuals lagged two periods.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

34

What is autocorrelation? Why is it problematic? Explain.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

35

Conintegration is

A)an iterative process for removing a unit root.

B)an iterative process for correcting the data for the presence of autocorrelation.

C)an empirical method for removing a unit root.

D)an empirical method for making a time-series I(1).

A)an iterative process for removing a unit root.

B)an iterative process for correcting the data for the presence of autocorrelation.

C)an empirical method for removing a unit root.

D)an empirical method for making a time-series I(1).

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

36

A potential shortcoming of the Cochrane-Orcutt method for AR(1)is that it

A)drops the first the first two observations.

B)drops the first observation.

C)does not typcially estimate correctly.

D) no longer changes between iterations.

A)drops the first the first two observations.

B)drops the first observation.

C)does not typcially estimate

correctly.D)

no longer changes between iterations. Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

37

The second step in the first iteration of the Cochrane-Orcutt method for AR(1)is to estimate the model

A) to generate an estimate of .

B) to generate an estimate of .

C) to generate an estimate of and .

D) to generate an estimate of .

A)

to generate an estimate of .B)

to generate an estimate of .C)

to generate an estimate of and .D)

to generate an estimate of . Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

38

The second iteration of the Cochrane-Orcutt method for AR(1)involves

A)repeating the process in the first iteration for the data adjusted by and .

B)repeating the process in the first iteration for the data adjusted by .

C)re-estimating following the process in the first iteration.

D)re-estimating using the data lagged one period.

A)repeating the process in the first iteration for the data adjusted by

and .B)repeating the process in the first iteration for the data adjusted by

.C)re-estimating

following the process in the first iteration.D)re-estimating

using the data lagged one period. Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

39

A unit root exists when

A)the parameter on the AR(1)process is equal to 0.

B)an explosive time-series exists.

C)a time-series is a stable AR(1).

D)the parameter on the AR(1)process is equal to 1.

A)the parameter on the AR(1)process is equal to 0.

B)an explosive time-series exists.

C)a time-series is a stable AR(1).

D)the parameter on the AR(1)process is equal to 1.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

40

The Prais-Winsten procedure for AR(1)improves on the Cochrane-Orcutt method for AR(1)by

A)incorporating estimates of the first observation only in the first iteration.

B)incorporating estimates of the first observation in all iterations.

C)generating an estimate of that actually equals ρ.

D)reducing the required number of iterations.

A)incorporating estimates of the first observation only in the first iteration.

B)incorporating estimates of the first observation in all iterations.

C)generating an estimate of

that actually equals ρ.D)reducing the required number of iterations.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

41

What is the potential shortcoming of the Cochrane-Orcutt method for AR(1)processes? Why is it a concern? How do you correct for it? Explain.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

42

How do you perform the Cochrane-Orcutt method for AR(1)processes? Explain.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

43

Suppose you are interested in explaining variation in quarterly Net Exports (billions)and that you estimate the regression function (standard errors in parentheses)

a)How many years' worth of data do you have? How can you tell? Explain.

b)Do you suspect that autocorrelation might be present in this model? If so,what type? Why? Explain.

c)How would you use the Regression test for AR(1)to determine whether autocorrelation is present? Explain.

d)Suppose you know that the autocorrelation follows an AR(1)process.How would you use the Prais-Winsten method to correct for the autocorrelation? Explain.

e)When using the Prais-Winsten method,how many observations will you have in your final analysis? Why? Explain.

a)How many years' worth of data do you have? How can you tell? Explain.

b)Do you suspect that autocorrelation might be present in this model? If so,what type? Why? Explain.

c)How would you use the Regression test for AR(1)to determine whether autocorrelation is present? Explain.

d)Suppose you know that the autocorrelation follows an AR(1)process.How would you use the Prais-Winsten method to correct for the autocorrelation? Explain.

e)When using the Prais-Winsten method,how many observations will you have in your final analysis? Why? Explain.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

44

How do you perform Prais-Winsten method for AR(1)processes? Explain.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

45

What is a unit root? Why is it problematic? Explain.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

46

Suppose you are interested in explaining variation in monthly Ice Cream consumption (thousands of gallons)and that you estimate the regression function (standard errors in parentheses)

a)How many years' worth of data do you have? How can you tell? Explain.

b)Do you suspect that autocorrelation might be present in this model? If so,what type? Why? Explain.

c)How would you use the Durbin-Watson test to determine whether autocorrelation is present? Explain.What type of autoregressive process does the Durbin-Watson test work for?

d)Suppose you know that the autocorrelation follows an AR(1)process.How would you use the Cochrane-Orcutt method to correct for the autocorrelation? Explain.

e)When using the Cochrane-Orcutt method,how many observations will you have in your final analysis? Why? Explain.

a)How many years' worth of data do you have? How can you tell? Explain.

b)Do you suspect that autocorrelation might be present in this model? If so,what type? Why? Explain.

c)How would you use the Durbin-Watson test to determine whether autocorrelation is present? Explain.What type of autoregressive process does the Durbin-Watson test work for?

d)Suppose you know that the autocorrelation follows an AR(1)process.How would you use the Cochrane-Orcutt method to correct for the autocorrelation? Explain.

e)When using the Cochrane-Orcutt method,how many observations will you have in your final analysis? Why? Explain.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

47

Why are Newey-West robust standard errors the preferred method for dealing with potential autocorrelation? Explain.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

48

What is the intuition behind the Regression test for AR(1)? Explain.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

49

How do you perform the Regression test for AR(1)? Explain.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

50

Suppose you are interested in explaining variation in annual Defense Spending (billions)and that you estimate the regression function (standard errors in parentheses)

a)How many years' worth of data do you have? How can you tell? Explain.

b)Do you suspect that autocorrelation might be present in this model? If so,what type? Why? Explain.

c)How would you use the Regression test for AR(2)to determine whether autocorrelation is present? Explain.

d)What is the preferred method of correct for potential autocorrelation? Why is it preferred? Explain.

Suppose you are interested in explaining variation in annual Defense Spending (billions)and that you estimate the sample regression function (standard errors in parentheses)

a)How many years' worth of data do you have? How can you tell? Explain.

b)Do you suspect that autocorrelation might be present in this model? If so,what type? Why? Explain.

c)How would you use the Regression test for AR(2)to determine whether autocorrelation is present? Explain.

d)What is the preferred method of correct for potential autocorrelation? Why is it preferred? Explain.

Suppose you are interested in explaining variation in annual Defense Spending (billions)and that you estimate the sample regression function (standard errors in parentheses)

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 50 flashcards in this deck.