Exam 11: Auto-Correlation

Exam 1: An Introduction to Econometrics and Statistical Inference16 Questions

Exam 2: Collection and Management of Data16 Questions

Exam 3: Summary Statistics29 Questions

Exam 4: Simple Linear Regression44 Questions

Exam 5: Hypothesis Testing in Linear Regression Analysis34 Questions

Exam 6: Multiple Linear Regression Analysis44 Questions

Exam 7: Qualitative Variables and Non-Linearities in Multiple Linear Regression Analysis40 Questions

Exam 8: Model Selection in Multiple Linear Regression Analysis31 Questions

Exam 9: Heteroskedasticity39 Questions

Exam 10: Time Series Analysis38 Questions

Exam 11: Auto-Correlation50 Questions

Exam 12: Limited Dependent Variables40 Questions

Exam 13: Panel Data31 Questions

Exam 14: Instrumental Variables for Simultaneous Equations, Endogenous Independent Variables, and Measurement Error26 Questions

Exam 15: Quantile Regression, Count Data, Sample Selection Bias, and Quasi-Experimental Methods29 Questions

Select questions type

The second iteration of the Cochrane-Orcutt method for AR(1)involves

Free

(Multiple Choice)

4.8/5  (40)

(40)

Correct Answer: Verified

Verified

B

The autoregressive structure of the error term is the current-period error term and

Free

(Multiple Choice)

4.9/5 (32)

Correct Answer:Verified

C

The null hypothesis for testing for the presence of autocorrelation is

(Multiple Choice)

4.9/5 (34)

How do you perform the Cochrane-Orcutt method for AR(1)processes? Explain.

(Essay)

4.9/5 (30)

What are the null and alternative hypotheses for testing for the presence of AR(1)autocorrelation? Why? Explain.

(Essay)

4.9/5 (30)

What is the potential shortcoming of the Cochrane-Orcutt method for AR(1)processes? Why is it a concern? How do you correct for it? Explain.

(Essay)

4.9/5 (38)

Suppose you are interested in explaining variation in quarterly Net Exports (billions)and that you estimate the regression function (standard errors in parentheses) Net ort= -207.66+ 0.48 Exchange + 1.39 (42.31) (0.15) (0.43) n=116 =.9528

a)How many years' worth of data do you have? How can you tell? Explain.

b)Do you suspect that autocorrelation might be present in this model? If so,what type? Why? Explain.

c)How would you use the Regression test for AR(1)to determine whether autocorrelation is present? Explain.

d)Suppose you know that the autocorrelation follows an AR(1)process.How would you use the Prais-Winsten method to correct for the autocorrelation? Explain.

e)When using the Prais-Winsten method,how many observations will you have in your final analysis? Why? Explain.

(Essay)

4.7/5 (42)

Why are Newey-West robust standard errors the preferred method for dealing with potential autocorrelation? Explain.

(Essay)

4.8/5 (42)

Write out the model for an AR(1)process.Explain what it means.Repeat for an AR(2)process.

(Essay)

4.9/5 (29)

Autoregressive error terms are potentially problematic because they result in

(Multiple Choice)

4.8/5 (46)

If positive autocorrelation is not present,then the Durbin-Watson test statistic will be

(Multiple Choice)

4.9/5 (29)

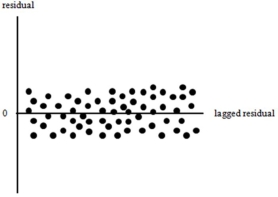

Suppose that you plot the residuals from a regression of Number of Wins on Payroll for the Dallas Cowboys over the last 20 years and you get the following  You would conclude that

You would conclude that

(Multiple Choice)

4.8/5 (31)

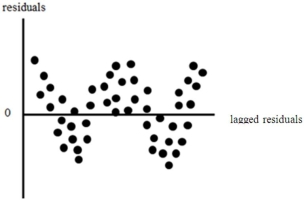

Suppose that you plot the residuals from a regression of GDP on the unemployment rate and you get the following  You would conclude that the error terms are

You would conclude that the error terms are

(Multiple Choice)

4.9/5 (34)

A simple method for determining whether autocorrelation is present in a given data set is to

(Multiple Choice)

4.8/5 (28)

Suppose you are interested in explaining variation in monthly Ice Cream consumption (thousands of gallons)and that you estimate the regression function (standard errors in parentheses) Ice = 247.93+ 12.22+ 217.39 (98.62) (4.35) (81.63) n=192 =.9287

a)How many years' worth of data do you have? How can you tell? Explain.

b)Do you suspect that autocorrelation might be present in this model? If so,what type? Why? Explain.

c)How would you use the Durbin-Watson test to determine whether autocorrelation is present? Explain.What type of autoregressive process does the Durbin-Watson test work for?

d)Suppose you know that the autocorrelation follows an AR(1)process.How would you use the Cochrane-Orcutt method to correct for the autocorrelation? Explain.

e)When using the Cochrane-Orcutt method,how many observations will you have in your final analysis? Why? Explain.

(Essay)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)