Deck 29: Further Consolidation Issues I: Accounting for Intragroup Transact

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

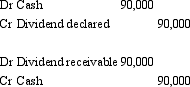

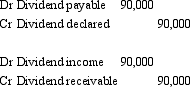

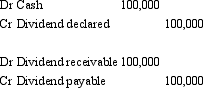

Little Company declared a dividend of $90,000 for the period ended 30 June 2005.Big Company owns 100 per cent of the equity of Little Company.Big Company accrues dividends when they are declared by its subsidiaries.What elimination entry would be required to prepare the consolidated financial statements for the group for the period ended 30 June 2005?

A)

B)

C)

D)

E) None of the given answers.

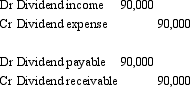

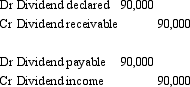

A)

B)

C)

D)

E) None of the given answers.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

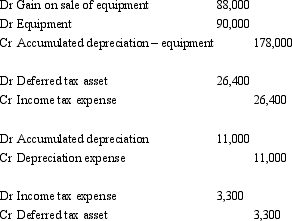

Zeus Ltd owns 100 per cent of the issued capital of Ares Ltd.On 1 July 2005 Zeus Ltd purchased an item of equipment from Ares Ltd for $800,000.Ares had owned the equipment for 2 years.It originally cost $890,000 and the accumulated depreciation was $178,000 at the time of sale.The equipment has been depreciated over this time,but not written down or revalued.The remaining useful life of the equipment at 1 July 2005 is estimated to be 8 years.Zeus Ltd expects the benefits to be obtained from the equipment to be evenly received over its useful life.The tax rate is 30 per cent. What are the consolidation journal entries required for this inter-company transaction for the period ended 30 June 2006?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Question

Question

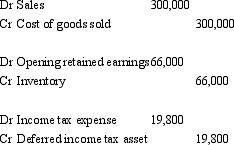

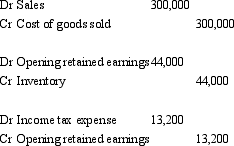

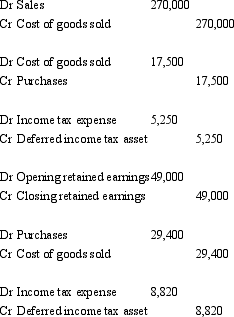

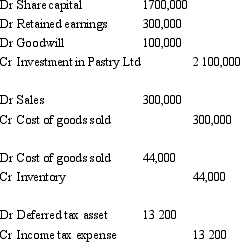

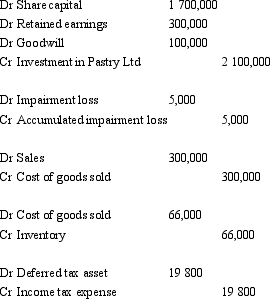

French Ltd owns 100 per cent of the issued capital of Pastry Ltd.During the period ended 30 June 2006 Pastry Ltd sold inventory that cost $190,000 for $300,000 to French Ltd.Sixty per cent of this inventory remains on hand in French Ltd at the end of that year.Both companies use a perpetual inventory system.The taxation rate is 30 per cent. What consolidation journal entries are required in relation to the inter-company transaction for the period ending 30 June 2007?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Question

Question

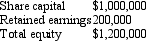

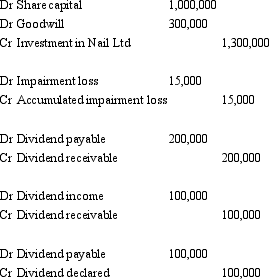

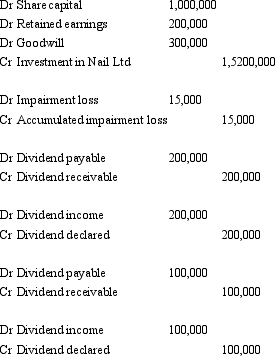

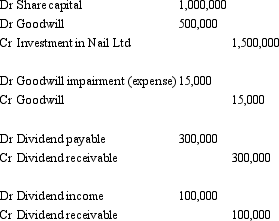

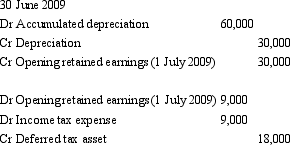

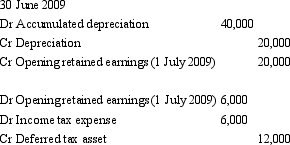

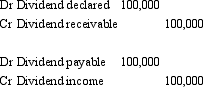

Hammer Ltd acquired all the issued capital of Nail Ltd on 1 July 2005 for cash consideration of $1.5 million.The fair value of the net assets of Nail Ltd at that date was $1.2 million as follows:  During the period ended 30 June 2006,Nail Ltd declared a dividend of $200,000 that is identified as being paid out of pre-acquisition profits and a further $100,000 is declared at the end of the period that is out of post-acquisition profits.Goodwill had been determined to have been impaired by $15,000 during the period.What consolidation journal entries would be required to prepare group accounts for the period ended 30 June 2006?

During the period ended 30 June 2006,Nail Ltd declared a dividend of $200,000 that is identified as being paid out of pre-acquisition profits and a further $100,000 is declared at the end of the period that is out of post-acquisition profits.Goodwill had been determined to have been impaired by $15,000 during the period.What consolidation journal entries would be required to prepare group accounts for the period ended 30 June 2006?

A)

B)

C)

D)

E) None of the given answers.

During the period ended 30 June 2006,Nail Ltd declared a dividend of $200,000 that is identified as being paid out of pre-acquisition profits and a further $100,000 is declared at the end of the period that is out of post-acquisition profits.Goodwill had been determined to have been impaired by $15,000 during the period.What consolidation journal entries would be required to prepare group accounts for the period ended 30 June 2006?A)

B)

C)

D)

E) None of the given answers.

Question

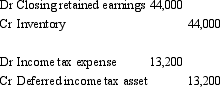

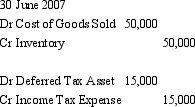

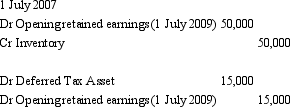

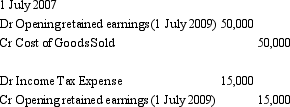

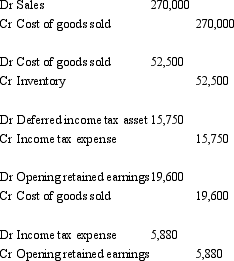

The journal entries to eliminate unrealised profit in closing inventory at 30 June 2007 were as follows.  What are the journal entries to eliminate the unrealised profits in opening inventory the following period?

What are the journal entries to eliminate the unrealised profits in opening inventory the following period?

A)

B)

C)

D)

E) None of the given answers

What are the journal entries to eliminate the unrealised profits in opening inventory the following period?A)

B)

C)

D)

E) None of the given answers

Question

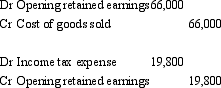

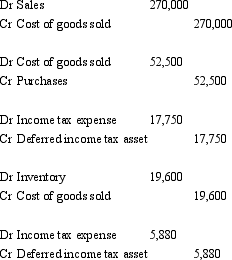

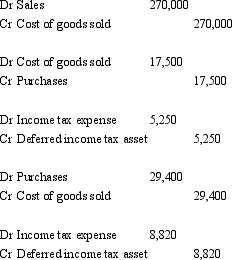

Belgium Ltd owns all the issued capital of Chocolate Ltd.During the period ended 30 June 2005 Belgium Ltd sold Chocolate Ltd inventory that had a cost of $200,000 for $270,000.At the end of the current period Chocolate Ltd had 75 per cent of that inventory still on hand; the rest was sold to entities external to the group.During the previous period Chocolate Ltd had sold inventory to Belgium Ltd at a profit of $49,000.At the end of that period (30 June 2004)Belgium Ltd still had 40 per cent of that inventory on hand.That entire inventory was sold to parties external to the group during the current year.The taxation rate is 30 per cent and both companies use a perpetual inventory system. What consolidation journal entries are required to eliminate the effects of these transactions for the period ended 30 June 2005?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Question

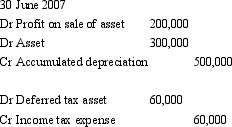

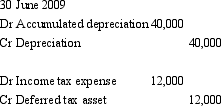

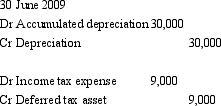

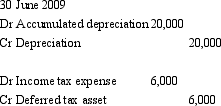

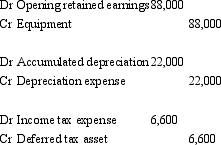

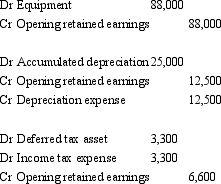

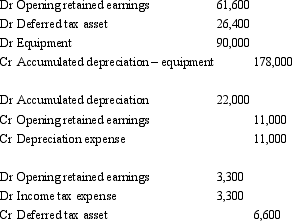

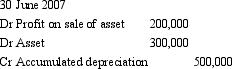

A non-current asset was sold by Subsidiary Limited to Parent Limited on 30 June 2007.The carrying amount of the asset at the time of the sale was $700,000.As part of the consolidation process,the following journal entry was passed.  Assuming there is another ten years of useful life remaining for the asset,what are the journal entries at 30 June 2009 to adjust for depreciation?

Assuming there is another ten years of useful life remaining for the asset,what are the journal entries at 30 June 2009 to adjust for depreciation?

A)

B)

C)

D)

E)

Assuming there is another ten years of useful life remaining for the asset,what are the journal entries at 30 June 2009 to adjust for depreciation?A)

B)

C)

D)

E)

Question

Question

Question

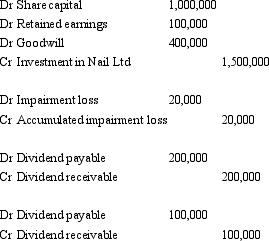

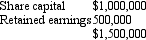

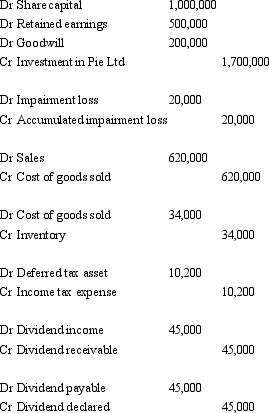

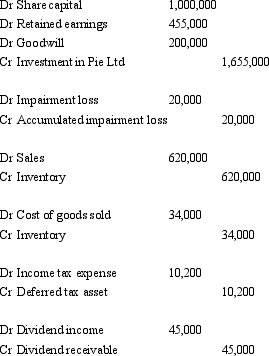

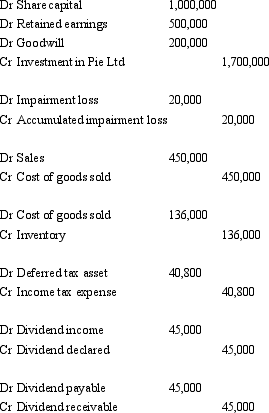

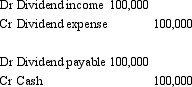

Meat Ltd purchased 100 per cent of the issued capital of Pie Ltd for a cash consideration of $1.7 million on 1 July 2004.At that time the fair value of the net assets of Pie Ltd were represented by:  Goodwill had been determined to have been impaired by $20,000 during the period.During the period ended 30 June 2005 Pie Ltd sold inventory that cost $450,000 for $620,000 to Meat Ltd.Twenty percent of this inventory remains on hand in Meat Ltd at the end of the year.Both companies use a perpetual inventory system.The taxation rate is 30 per cent.At the end of the period Pie Ltd declared a dividend of $45,000 that has not yet been paid.

Goodwill had been determined to have been impaired by $20,000 during the period.During the period ended 30 June 2005 Pie Ltd sold inventory that cost $450,000 for $620,000 to Meat Ltd.Twenty percent of this inventory remains on hand in Meat Ltd at the end of the year.Both companies use a perpetual inventory system.The taxation rate is 30 per cent.At the end of the period Pie Ltd declared a dividend of $45,000 that has not yet been paid.

What consolidation journal entries are required for the period ending 30 June 2005?

A)

B)

C)

D)

E) None of the given answers.

Goodwill had been determined to have been impaired by $20,000 during the period.During the period ended 30 June 2005 Pie Ltd sold inventory that cost $450,000 for $620,000 to Meat Ltd.Twenty percent of this inventory remains on hand in Meat Ltd at the end of the year.Both companies use a perpetual inventory system.The taxation rate is 30 per cent.At the end of the period Pie Ltd declared a dividend of $45,000 that has not yet been paid.What consolidation journal entries are required for the period ending 30 June 2005?

A)

B)

C)

D)

E) None of the given answers.

Question

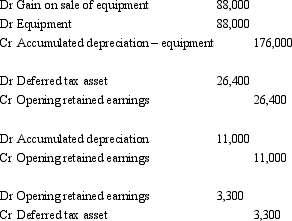

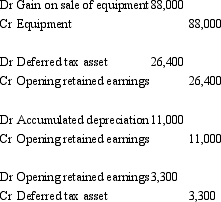

Zeus Ltd owns 100 per cent of the issued capital of Ares Ltd.On 1 July 2005 Zeus Ltd purchased an item of equipment from Ares Ltd for $800,000.Ares had owned the equipment for 2 years.It originally cost $890,000 and the accumulated depreciation was $178,000 at the time of sale.The equipment has been depreciated over this time,but not written down or revalued.The remaining useful life of the equipment at 1 July 2005 is estimated to be 8 years.Zeus Ltd expects the benefits to be obtained from the equipment to be evenly received over its useful life.The tax rate is 30 per cent. What are the consolidation journal entries required for this inter-company transaction for the period ended 30 June 2007?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Question

Question

Monster Co Ltd owns 100 per cent of the issued shares of Mini Co Ltd.Mini Co Ltd declared a dividend of $100,000 for the period ended 30 June 2004.Monster Co Ltd accrues dividends when they are declared by its subsidiaries.What elimination entry would be required to prepare the consolidated financial statements for the group for the period ended 30 June 2005?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Question

Question

Question

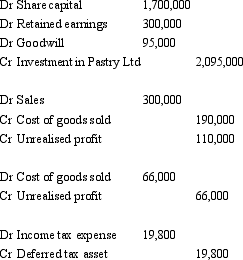

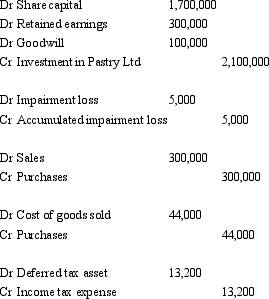

French Ltd purchased 100 per cent of the issued capital of Pastry Ltd for a cash consideration of $2.1 million on 1 July 2005.At that time the fair value of the net assets of Pastry Ltd were represented by:  Goodwill had been determined to have been impaired by $ 5000 during the period.During the period ended 30 June 2006 Pastry Ltd sold inventory that cost $190,000 for $300,000 to French Ltd.Sixty percent of this inventory remains on hand in French Ltd at the end of the year.Both companies use a perpetual inventory system.The taxation rate is 30 per cent.

Goodwill had been determined to have been impaired by $ 5000 during the period.During the period ended 30 June 2006 Pastry Ltd sold inventory that cost $190,000 for $300,000 to French Ltd.Sixty percent of this inventory remains on hand in French Ltd at the end of the year.Both companies use a perpetual inventory system.The taxation rate is 30 per cent.

What consolidation journal entries are required for the period ending 30 June 2006?

A)

B)

C)

D)

E) None of the given answers.

Goodwill had been determined to have been impaired by $ 5000 during the period.During the period ended 30 June 2006 Pastry Ltd sold inventory that cost $190,000 for $300,000 to French Ltd.Sixty percent of this inventory remains on hand in French Ltd at the end of the year.Both companies use a perpetual inventory system.The taxation rate is 30 per cent.What consolidation journal entries are required for the period ending 30 June 2006?

A)

B)

C)

D)

E) None of the given answers.

Question

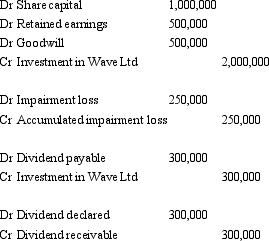

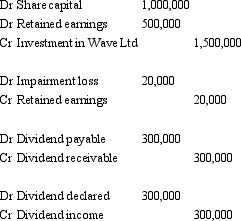

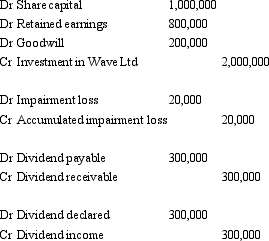

Radio Ltd acquired all the issued capital of Wave Ltd on 1 July 2004 for cash consideration of $2 million.The fair value of the net assets of Wave Ltd at that date was $1.8 million as follows:  During the period ending 30 June 2005 Wave Ltd declare a dividend of $300,000 that is identified as being paid out of pre-acquisition profits.Goodwill had been determined to have impaired by $20,000 during the period.What consolidation journal entries would be required to prepare group accounts for the period ended 30 June 2005?

During the period ending 30 June 2005 Wave Ltd declare a dividend of $300,000 that is identified as being paid out of pre-acquisition profits.Goodwill had been determined to have impaired by $20,000 during the period.What consolidation journal entries would be required to prepare group accounts for the period ended 30 June 2005?

A)

B)

C)

D)

E) None of the given answers.

During the period ending 30 June 2005 Wave Ltd declare a dividend of $300,000 that is identified as being paid out of pre-acquisition profits.Goodwill had been determined to have impaired by $20,000 during the period.What consolidation journal entries would be required to prepare group accounts for the period ended 30 June 2005?A)

B)

C)

D)

E) None of the given answers.

Question

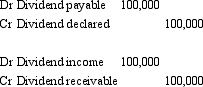

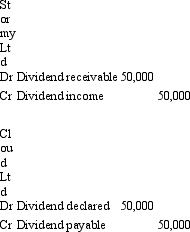

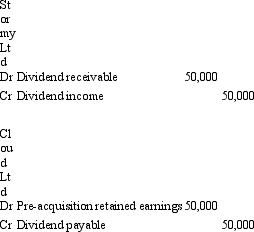

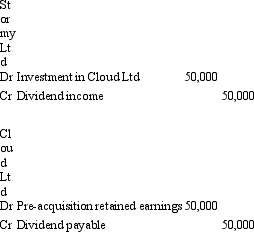

Stormy Ltd has purchased all the issued capital of Cloud Ltd at the beginning of the current period.At the end of the period Cloud Ltd declares a dividend of $50,000 that is identified as being paid out of pre-acquisition profits.What entries would Stormy Ltd and Cloud Ltd make in their own books? (Assume Stormy Ltd accrues the dividends of subsidiaries when they are declared.)

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Question

A non-current asset was sold by Subsidiary Limited to Parent Limited during the 2006-07 financial year.The carrying amount of the asset at the time of the sale was $700,000.As part of the consolidation process,the following journal entry was passed.  What (a)amount did Parent Limited pay Subsidiary Limited for the asset; (b)was the cost of the asset as shown in the books of Subsidiary Limited?

What (a)amount did Parent Limited pay Subsidiary Limited for the asset; (b)was the cost of the asset as shown in the books of Subsidiary Limited?

A) (a) $900,000; (b) $1,400,000

B) (a) $900,000; (b) $1,200,000.

C) (a) $700,000; (b) $1,200,000

D) (a) $900,000; (b) $800,000

E) Cannot determine from the information provided.

What (a)amount did Parent Limited pay Subsidiary Limited for the asset; (b)was the cost of the asset as shown in the books of Subsidiary Limited?A) (a) $900,000; (b) $1,400,000

B) (a) $900,000; (b) $1,200,000.

C) (a) $700,000; (b) $1,200,000

D) (a) $900,000; (b) $800,000

E) Cannot determine from the information provided.

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/46

Play

Full screen (f)

Deck 29: Further Consolidation Issues I: Accounting for Intragroup Transact

1

If a subsidiary makes a dividend payment out of pre-acquisition earnings,the parent entity should consider whether its investment in the subsidiary is impaired.

True

2

If we simply aggregate the sales of the parent and subsidiary companies,without adjustment,when there have been intragroup sales,total income would be overstateD.

True

3

Intragroup sales of non-current assets results in the need to eliminate the effect of any profit or loss on sale in the period of the sale and,in the rest of the periods of the asset's life,any tax effects of the profit or loss,the depreciation and accumulated depreciation will have to be adjusted for the life of the asset,along with the tax effects of the adjustment to depreciation:

True

4

The value of inventory on hand for the economic group at the end of the period will always equal the sum of the inventory on hand at the end of the period for each of the entities in the group:

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

5

In the absence of an election to be a 'tax consolidated group',the Australian Tax Office assesses income earned by the individual legal entities in an economic group and does not take into consideration consolidation adjustments required for group accounts:

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

6

Dividends paid between entities in the group should be:

A) Not permitted by the ultimate controlling entity because it does not make sense to exchange money between entities in the one economic group.

B) Reflected in the group accounts because it reflects the economic return the group earned by investing in the companies that form its operations.

C) Eliminated from the group accounts, but reflected in the individual legal entity accounts, since the group accounts reflect the many entities as one single economic entity.

D) Retained in the consolidated statements but disclosed separately as related-party transactions.

E) None of the given answers.

A) Not permitted by the ultimate controlling entity because it does not make sense to exchange money between entities in the one economic group.

B) Reflected in the group accounts because it reflects the economic return the group earned by investing in the companies that form its operations.

C) Eliminated from the group accounts, but reflected in the individual legal entity accounts, since the group accounts reflect the many entities as one single economic entity.

D) Retained in the consolidated statements but disclosed separately as related-party transactions.

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

7

AASB 127 "Consolidated and Separate Financial Statements" prescribes that intragroup balances,transactions,income and expenses be eliminated in full on consolidation.This requirement is consistent with the parent entity concept of consolidation.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

8

Examples of intragroup transactions include:

A) Dividends payable to group members.

B) The payment of taxation.

C) The recognition of minority interests.

D) The sale of inventories to external parties.

E) None of the given answers.

A) Dividends payable to group members.

B) The payment of taxation.

C) The recognition of minority interests.

D) The sale of inventories to external parties.

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

9

Little Company declared a dividend of $90,000 for the period ended 30 June 2005.Big Company owns 100 per cent of the equity of Little Company.Big Company accrues dividends when they are declared by its subsidiaries.What elimination entry would be required to prepare the consolidated financial statements for the group for the period ended 30 June 2005?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

10

Intragroup transactions that are to be eliminated in the consolidated accounts include:

A) Inter-entity loans.

B) Inter-entity sales of non-current assets.

C) The payment of management fees to a member of the group.

D) The transfer of tax losses between entities in the group without consideration being paid.

E) All of the given answers.

A) Inter-entity loans.

B) Inter-entity sales of non-current assets.

C) The payment of management fees to a member of the group.

D) The transfer of tax losses between entities in the group without consideration being paid.

E) All of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

11

AASB 127 "Consolidated and Separate Financial Statements" prescribes that intragroup balances,transactions,income and expenses be eliminated in full on consolidation.This requirement is consistent with the economic entity concept of consolidation.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

12

Intragroup profits are eliminated in consolidation to exclude intragroup transactions in the parent entity's financial statements.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

13

Parent Ltd sells inventories to Child Ltd amounting to $200 000 during the financial year.The inventories are no longer in the hands of Child Ltd at year-end.Parent Ltd is no longer required to eliminate these intragroup transactions because these transactions have been realised by sale to external parties.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

14

Company A owns 51 per cent of the issued capital of Company B and Company A owns 60 per cent of the issued capital of Company

C. Company A controls both B and

C. If Company A sells inventory for $500,000 to Company C and Company C sells it to Company B for $600,000 and Company B sells it to an entity external to the group for $700,000, the amount of sales revenue to be recorded for that inventory for the group of companies is $1,560,000:

C. Company A controls both B and

C. If Company A sells inventory for $500,000 to Company C and Company C sells it to Company B for $600,000 and Company B sells it to an entity external to the group for $700,000, the amount of sales revenue to be recorded for that inventory for the group of companies is $1,560,000:

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

15

Question 1: Transactions between entities that form an economic group should be eliminated in proportion to the level of control between the parent entity and the subsidiary entity:

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

16

Companies in an economic entity may increase the level of consolidated sales reported by selling inventory between themselves.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

17

The level of equity ownership is not a factor in deciding what proportion of a transaction between entities in a group should be eliminated.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

18

Dividends may be identified as being paid out of pre-acquisition or post-acquisition profits by a subsidiary company.Where dividends are paid out of post-acquisition profits the investment in the subsidiary should be decreased by the amount of the dividend.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

19

The fact that consolidation worksheets start "afresh" each year means that the tax entry for eliminating unrealised profit in opening inventory requires a "Dr" to Deferred Tax Assets,rather than Income Tax Expense:

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

20

Intragroup profits are eliminated in consolidation to reduce consolidated profits.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

21

Zeus Ltd owns 100 per cent of the issued capital of Ares Ltd.On 1 July 2005 Zeus Ltd purchased an item of equipment from Ares Ltd for $800,000.Ares had owned the equipment for 2 years.It originally cost $890,000 and the accumulated depreciation was $178,000 at the time of sale.The equipment has been depreciated over this time,but not written down or revalued.The remaining useful life of the equipment at 1 July 2005 is estimated to be 8 years.Zeus Ltd expects the benefits to be obtained from the equipment to be evenly received over its useful life.The tax rate is 30 per cent. What are the consolidation journal entries required for this inter-company transaction for the period ended 30 June 2006?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

22

Companies A,B and C are all part of the one economic entity,but are all separate legal entities required to prepare their own financial statements.Company A sold Company B's inventory that cost $56,000 for $78,000.At the end of the same period Company B has three-quarters of that inventory still on hand and the rest has been sold to an entity outside the economic group.At what amount should the inventory remaining in Company B be recorded in Company B's own financial statements?

A) $42,000

B) $58 500

C) $56,000

D) $14 625

E) None of the given answers.

A) $42,000

B) $58 500

C) $56,000

D) $14 625

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

23

French Ltd owns 100 per cent of the issued capital of Pastry Ltd.During the period ended 30 June 2006 Pastry Ltd sold inventory that cost $190,000 for $300,000 to French Ltd.Sixty per cent of this inventory remains on hand in French Ltd at the end of that year.Both companies use a perpetual inventory system.The taxation rate is 30 per cent. What consolidation journal entries are required in relation to the inter-company transaction for the period ending 30 June 2007?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

24

What is the amount of unrealised profit that needs to be eliminated at the end of the period,in the following situation,where Morecombe Limited is the parent of Wise Limited? (Ignore the tax effect) Morecombe purchases 500 units of inventory for $20 each.Morecombe sells this entire inventory to Wise at a mark up of 25 per cent.Wise then sells half of the inventory to an external party.Half of the remaining amount (after the external sale)is sold back to Morecombe for $2,500.

A) Cannot determine from the information given.

B) $300.

C) $625.

D) $1 250.

E) $2 500.

A) Cannot determine from the information given.

B) $300.

C) $625.

D) $1 250.

E) $2 500.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

25

Hammer Ltd acquired all the issued capital of Nail Ltd on 1 July 2005 for cash consideration of $1.5 million.The fair value of the net assets of Nail Ltd at that date was $1.2 million as follows: During the period ended 30 June 2006,Nail Ltd declared a dividend of $200,000 that is identified as being paid out of pre-acquisition profits and a further $100,000 is declared at the end of the period that is out of post-acquisition profits.Goodwill had been determined to have been impaired by $15,000 during the period.What consolidation journal entries would be required to prepare group accounts for the period ended 30 June 2006?

A)

B)

C)

D)

E) None of the given answers.

During the period ended 30 June 2006,Nail Ltd declared a dividend of $200,000 that is identified as being paid out of pre-acquisition profits and a further $100,000 is declared at the end of the period that is out of post-acquisition profits.Goodwill had been determined to have been impaired by $15,000 during the period.What consolidation journal entries would be required to prepare group accounts for the period ended 30 June 2006?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

26

The journal entries to eliminate unrealised profit in closing inventory at 30 June 2007 were as follows. What are the journal entries to eliminate the unrealised profits in opening inventory the following period?

A)

B)

C)

D)

E) None of the given answers

What are the journal entries to eliminate the unrealised profits in opening inventory the following period?A)

B)

C)

D)

E) None of the given answers

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

27

Belgium Ltd owns all the issued capital of Chocolate Ltd.During the period ended 30 June 2005 Belgium Ltd sold Chocolate Ltd inventory that had a cost of $200,000 for $270,000.At the end of the current period Chocolate Ltd had 75 per cent of that inventory still on hand; the rest was sold to entities external to the group.During the previous period Chocolate Ltd had sold inventory to Belgium Ltd at a profit of $49,000.At the end of that period (30 June 2004)Belgium Ltd still had 40 per cent of that inventory on hand.That entire inventory was sold to parties external to the group during the current year.The taxation rate is 30 per cent and both companies use a perpetual inventory system. What consolidation journal entries are required to eliminate the effects of these transactions for the period ended 30 June 2005?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

28

A non-current asset was sold by Subsidiary Limited to Parent Limited on 30 June 2007.The carrying amount of the asset at the time of the sale was $700,000.As part of the consolidation process,the following journal entry was passed. Assuming there is another ten years of useful life remaining for the asset,what are the journal entries at 30 June 2009 to adjust for depreciation?

A)

B)

C)

D)

E)

Assuming there is another ten years of useful life remaining for the asset,what are the journal entries at 30 June 2009 to adjust for depreciation?A)

B)

C)

D)

E)

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

29

The treatment of dividends,paid by a subsidiary,that are identified as paid out of pre-acquisition profits in the period they are paid is to:

A) Capitalise the dividend in the books of the parent entity as a further investment in the subsidiary. This amount will be eliminated on consolidation.

B) Record dividend revenue and the receipt of cash in the books of the parent entity and then eliminate the transaction on consolidation.

C) Record a return of the investment in the subsidiary by decreasing the investment in the subsidiary in the books of the parent entity. The amount of the investment will be eliminated on consolidation.

D) Record a decrease in pre-acquisition reserves or retained profits in the books of the subsidiary so that on consolidation the elimination entry will automatically eliminate the effect of the dividend.

E) None of the given answers.

A) Capitalise the dividend in the books of the parent entity as a further investment in the subsidiary. This amount will be eliminated on consolidation.

B) Record dividend revenue and the receipt of cash in the books of the parent entity and then eliminate the transaction on consolidation.

C) Record a return of the investment in the subsidiary by decreasing the investment in the subsidiary in the books of the parent entity. The amount of the investment will be eliminated on consolidation.

D) Record a decrease in pre-acquisition reserves or retained profits in the books of the subsidiary so that on consolidation the elimination entry will automatically eliminate the effect of the dividend.

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

30

Companies A,B and C are all part of the one economic entity,but are all separate legal entities required to prepare their own financial statements.Company A sold Company B inventory that cost $56,000 for $78,000.At the end of the same period Company B has three-quarters of that inventory still on hand and the rest has been sold to an entity outside the economic group.At what amount should the inventory remaining in Company B be recorded in the consolidated statements?

A) $14 625

B) $56,000

C) $58 500

D) $42,000

E) None of the given answers.

A) $14 625

B) $56,000

C) $58 500

D) $42,000

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

31

Meat Ltd purchased 100 per cent of the issued capital of Pie Ltd for a cash consideration of $1.7 million on 1 July 2004.At that time the fair value of the net assets of Pie Ltd were represented by: Goodwill had been determined to have been impaired by $20,000 during the period.During the period ended 30 June 2005 Pie Ltd sold inventory that cost $450,000 for $620,000 to Meat Ltd.Twenty percent of this inventory remains on hand in Meat Ltd at the end of the year.Both companies use a perpetual inventory system.The taxation rate is 30 per cent.At the end of the period Pie Ltd declared a dividend of $45,000 that has not yet been paid.

What consolidation journal entries are required for the period ending 30 June 2005?

A)

B)

C)

D)

E) None of the given answers.

Goodwill had been determined to have been impaired by $20,000 during the period.During the period ended 30 June 2005 Pie Ltd sold inventory that cost $450,000 for $620,000 to Meat Ltd.Twenty percent of this inventory remains on hand in Meat Ltd at the end of the year.Both companies use a perpetual inventory system.The taxation rate is 30 per cent.At the end of the period Pie Ltd declared a dividend of $45,000 that has not yet been paid.What consolidation journal entries are required for the period ending 30 June 2005?

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

32

Zeus Ltd owns 100 per cent of the issued capital of Ares Ltd.On 1 July 2005 Zeus Ltd purchased an item of equipment from Ares Ltd for $800,000.Ares had owned the equipment for 2 years.It originally cost $890,000 and the accumulated depreciation was $178,000 at the time of sale.The equipment has been depreciated over this time,but not written down or revalued.The remaining useful life of the equipment at 1 July 2005 is estimated to be 8 years.Zeus Ltd expects the benefits to be obtained from the equipment to be evenly received over its useful life.The tax rate is 30 per cent. What are the consolidation journal entries required for this inter-company transaction for the period ended 30 June 2007?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

33

Large Company owns 80 per cent of the issued capital of Smaller Company and Large Company owns 60 per cent of the issued capital of Medium Company.The three companies form an economic entity for the purposes of consolidated accounts.During the period Smaller Company sold inventory to Medium for $400,000.Medium sold the same inventory to Large for $560,000 and Large sold it to an entity external to the group for $760,000.What are the sales revenue reported in the consolidated statements for this item?

A) $1,416,000

B) $1,720,000

C) $760,000

D) $400,000

E) None of the given answers.

A) $1,416,000

B) $1,720,000

C) $760,000

D) $400,000

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

34

Monster Co Ltd owns 100 per cent of the issued shares of Mini Co Ltd.Mini Co Ltd declared a dividend of $100,000 for the period ended 30 June 2004.Monster Co Ltd accrues dividends when they are declared by its subsidiaries.What elimination entry would be required to prepare the consolidated financial statements for the group for the period ended 30 June 2005?

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following statements describes the reasons why tax adjustments may be required when eliminating the unrealised profit from intragroup sales of inventory?

A) Tax is paid on a group perspective and therefore one taxable income figure must be derived for the group.

B) Tax will be adjusted at the request of the Australian Taxation Office.

C) If tax has been paid by one of the separate legal entities, from the group's perspective this represents a deferral of the payment of tax.

D) If tax has been paid by one of the separate legal entities, from the group's perspective this represents a pre-payment of tax.

E) None of the given answers.

A) Tax is paid on a group perspective and therefore one taxable income figure must be derived for the group.

B) Tax will be adjusted at the request of the Australian Taxation Office.

C) If tax has been paid by one of the separate legal entities, from the group's perspective this represents a deferral of the payment of tax.

D) If tax has been paid by one of the separate legal entities, from the group's perspective this represents a pre-payment of tax.

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

36

What is the amount of unrealised profit that needs to be eliminated at the end of the period,in the following situation,where Barker Limited is the parent of Corbett Limited? (Ignore the tax effect) Barker purchases 500 units of inventory for $20 each.Barker sells this entire inventory to Corbett at a mark up of 50 per cent.At the end of the period,100 units are on hand.

A) $1,000.

B) $2,000.

C) $3,000.

D) $5,000.

E) $10,000.

A) $1,000.

B) $2,000.

C) $3,000.

D) $5,000.

E) $10,000.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

37

French Ltd purchased 100 per cent of the issued capital of Pastry Ltd for a cash consideration of $2.1 million on 1 July 2005.At that time the fair value of the net assets of Pastry Ltd were represented by: Goodwill had been determined to have been impaired by $ 5000 during the period.During the period ended 30 June 2006 Pastry Ltd sold inventory that cost $190,000 for $300,000 to French Ltd.Sixty percent of this inventory remains on hand in French Ltd at the end of the year.Both companies use a perpetual inventory system.The taxation rate is 30 per cent.

What consolidation journal entries are required for the period ending 30 June 2006?

A)

B)

C)

D)

E) None of the given answers.

Goodwill had been determined to have been impaired by $ 5000 during the period.During the period ended 30 June 2006 Pastry Ltd sold inventory that cost $190,000 for $300,000 to French Ltd.Sixty percent of this inventory remains on hand in French Ltd at the end of the year.Both companies use a perpetual inventory system.The taxation rate is 30 per cent.What consolidation journal entries are required for the period ending 30 June 2006?

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

38

Radio Ltd acquired all the issued capital of Wave Ltd on 1 July 2004 for cash consideration of $2 million.The fair value of the net assets of Wave Ltd at that date was $1.8 million as follows: During the period ending 30 June 2005 Wave Ltd declare a dividend of $300,000 that is identified as being paid out of pre-acquisition profits.Goodwill had been determined to have impaired by $20,000 during the period.What consolidation journal entries would be required to prepare group accounts for the period ended 30 June 2005?

A)

B)

C)

D)

E) None of the given answers.

During the period ending 30 June 2005 Wave Ltd declare a dividend of $300,000 that is identified as being paid out of pre-acquisition profits.Goodwill had been determined to have impaired by $20,000 during the period.What consolidation journal entries would be required to prepare group accounts for the period ended 30 June 2005?A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

39

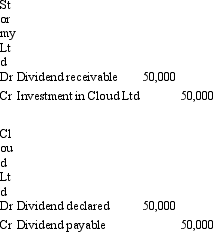

Stormy Ltd has purchased all the issued capital of Cloud Ltd at the beginning of the current period.At the end of the period Cloud Ltd declares a dividend of $50,000 that is identified as being paid out of pre-acquisition profits.What entries would Stormy Ltd and Cloud Ltd make in their own books? (Assume Stormy Ltd accrues the dividends of subsidiaries when they are declared.)

A)

B)

C)

D)

E) None of the given answers.

A)

B)

C)

D)

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

40

A non-current asset was sold by Subsidiary Limited to Parent Limited during the 2006-07 financial year.The carrying amount of the asset at the time of the sale was $700,000.As part of the consolidation process,the following journal entry was passed. What (a)amount did Parent Limited pay Subsidiary Limited for the asset; (b)was the cost of the asset as shown in the books of Subsidiary Limited?

A) (a) $900,000; (b) $1,400,000

B) (a) $900,000; (b) $1,200,000.

C) (a) $700,000; (b) $1,200,000

D) (a) $900,000; (b) $800,000

E) Cannot determine from the information provided.

What (a)amount did Parent Limited pay Subsidiary Limited for the asset; (b)was the cost of the asset as shown in the books of Subsidiary Limited?A) (a) $900,000; (b) $1,400,000

B) (a) $900,000; (b) $1,200,000.

C) (a) $700,000; (b) $1,200,000

D) (a) $900,000; (b) $800,000

E) Cannot determine from the information provided.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

41

Alice Ltd sold inventory items to its subsidiary Mad Hatter Ltd and had the following intercompany transactions: Cost of $100 000 for $125 000 for the year ended 30 June 2012.Half of the inventory items were sold by Mad Hatter Ltd to external parties before the financial year end 30 June 2012.

Cost of $75 000 for $100 000 for the year ended 30 June 2013.Half of the inventory items were sold by Mad Hatter Ltd to external parties before the financial year end 30 June 2013.

Ignoring taxes,which of the following statements is correct with respect to this transaction only for the year ended 30 June 2013?

A) Consolidated sales will decrease by $125 000.

B) Consolidated sales will increase by $25 000.

C) Consolidated profit will decrease by $12 500.

D) Consolidated profit will increase by $12 000

E) No change in the consolidated profit.

Cost of $75 000 for $100 000 for the year ended 30 June 2013.Half of the inventory items were sold by Mad Hatter Ltd to external parties before the financial year end 30 June 2013.

Ignoring taxes,which of the following statements is correct with respect to this transaction only for the year ended 30 June 2013?

A) Consolidated sales will decrease by $125 000.

B) Consolidated sales will increase by $25 000.

C) Consolidated profit will decrease by $12 500.

D) Consolidated profit will increase by $12 000

E) No change in the consolidated profit.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

42

Woody Ltd sold inventory items to its subsidiary Buzz Lightyear Ltd and had the following intercompany transactions: Cost of $300 000 for $375 000 for the year ended 30 June 2012.One third of the inventory items were sold by Buzz Lightyear Ltd to external parties before the financial year end 30 June 2012.

Cost of $100 000 for $75 000 for the year ended 30 June 2013.Half of the inventory items were sold by Mad Hatter Ltd to external parties before the financial year end 30 June 2013.

Ignoring taxes,which of the following statements is correct with respect to this transaction only for the year ended 30 June 2013

A) Consolidated sales will decrease by $100 000.

B) Consolidated sales will increase by $275 000.

C) Consolidated profit will increase by $62 500.

D) Consolidated profit will increase by $12 000

E) No change in the consolidated profit.

Cost of $100 000 for $75 000 for the year ended 30 June 2013.Half of the inventory items were sold by Mad Hatter Ltd to external parties before the financial year end 30 June 2013.

Ignoring taxes,which of the following statements is correct with respect to this transaction only for the year ended 30 June 2013

A) Consolidated sales will decrease by $100 000.

B) Consolidated sales will increase by $275 000.

C) Consolidated profit will increase by $62 500.

D) Consolidated profit will increase by $12 000

E) No change in the consolidated profit.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

43

Lilo Ltd sells inventory items to its subsidiary Stitch Ltd.If during the financial year 2013,the unrealised profits in ending inventory in Stitch Ltd exceeds that of its unrealized profits in beginning inventory,which of the following statements is correct with respect Lilo Ltd's consolidated financial statements after considering these transactions only?

A) Consolidated profit will decrease;

B) Consolidated deferred tax liability will increase;

C) Consolidated ending inventory will decrease;

D) Consolidated sales will be unaffected;

E) None of the given answers.

A) Consolidated profit will decrease;

B) Consolidated deferred tax liability will increase;

C) Consolidated ending inventory will decrease;

D) Consolidated sales will be unaffected;

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

44

Penny Ltd sells inventory items to its subsidiary Bolt Ltd.If during the financial year 2013,the unrealised profits in ending inventory in Stitch Ltd is less than its unrealised profits in beginning inventory,which of the following statements is correct with respect Penny Ltd's consolidated financial statements after considering these transactions only?

A) Consolidated profit will increase;

B) Consolidated deferred tax liability will increase;

C) Consolidated ending inventory will decrease;

D) Consolidated sales will be unaffected;

E) None of the given answers.

A) Consolidated profit will increase;

B) Consolidated deferred tax liability will increase;

C) Consolidated ending inventory will decrease;

D) Consolidated sales will be unaffected;

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

45

Aladdin Ltd sold inventory items (with a cost of $100 000)to its subsidiary Genie Ltd for $120,000.Half of the inventory items were sold by Genie Ltd to external parties before the financial year end.Ignoring taxes,which of the following statements is correct with respect to this transaction only?

A) Consolidated sales will decrease by $60 000.

B) Consolidated sales will decrease by $100 000.

C) Consolidated profit will decrease by $10 000.

D) Consolidated profit will decrease by $20 000

E) Consolidated cost of goods sold will decrease by $50 000.

A) Consolidated sales will decrease by $60 000.

B) Consolidated sales will decrease by $100 000.

C) Consolidated profit will decrease by $10 000.

D) Consolidated profit will decrease by $20 000

E) Consolidated cost of goods sold will decrease by $50 000.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

46

Aladdin Ltd sells inventory for a profit to its subsidiary,Jasmine Ltd,to be used as machinery in Jasmine Ltd's production process.The consolidation worksheet of Aladdin Ltd with respect to this transaction only should ?not include .....:

A) a debit to sales.

B) a credit to cost of sales.

C) a credit to inventories.

D) a credit to machinery.

E) None of the given answers.

A) a debit to sales.

B) a credit to cost of sales.

C) a credit to inventories.

D) a credit to machinery.

E) None of the given answers.

Unlock Deck

Unlock for access to all 46 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 46 flashcards in this deck.