Exam 29: Further Consolidation Issues I: Accounting for Intragroup Transact

Exam 1: An Overview of the Australian External Reporting Environment50 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financ62 Questions

Exam 3: Theories of Financial Accounting61 Questions

Exam 4: An Overview of Accounting for Assets62 Questions

Exam 5: Depreciation of Property, plant and Equipment62 Questions

Exam 6: Revaluation and Impairment Testing of Non-Current Assets59 Questions

Exam 7: Inventory61 Questions

Exam 8: Accounting for Intangibles61 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets61 Questions

Exam 10: An Overview of Accounting for Liabilities58 Questions

Exam 11: Accounting for Lease78 Questions

Exam 12: Set-Off and Extinguishment of Debt47 Questions

Exam 13: Accounting for Employee Benefits67 Questions

Exam 14: Share Capital and Reserves66 Questions

Exam 15: Accounting for Financial Instruments72 Questions

Exam 16: Revenue Recognition Issues64 Questions

Exam 17: The Statement of Comprehensive Income and Statement of Changes in E62 Questions

Exam 18: Accounting for Share-Based Payments62 Questions

Exam 19: Accounting for Income Taxes56 Questions

Exam 20: Cash-Flow Statements60 Questions

Exam 21: Accounting for the Extractive Industries60 Questions

Exam 22: Accounting for General Insurance Contracts58 Questions

Exam 23: Accounting for Superannuation Plans62 Questions

Exam 24: Events Occurring After Balance Sheet Date62 Questions

Exam 25: Segment Reporting61 Questions

Exam 26: Related-Party Disclosures59 Questions

Exam 27: Earnings Per Share43 Questions

Exam 28: Accounting for Group Structures69 Questions

Exam 29: Further Consolidation Issues I: Accounting for Intragroup Transact46 Questions

Exam 30: Further Consolidation Issues II: Accounting for Minority Interests34 Questions

Exam 31: Further Consolidation Issues III: Accounting for Indirect Ownershi38 Questions

Exam 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg39 Questions

Exam 33: Accounting for Equity Investments67 Questions

Exam 33: Accounting for Equity Investments59 Questions

Exam 35: Accounting for Foreign Currency Transactions58 Questions

Exam 36: Translation of the Accounts of Foreign Operations41 Questions

Exam 37: Accounting for Corporate Social Responsibility59 Questions

Select questions type

Little Company declared a dividend of $90,000 for the period ended 30 June 2005.Big Company owns 100 per cent of the equity of Little Company.Big Company accrues dividends when they are declared by its subsidiaries.What elimination entry would be required to prepare the consolidated financial statements for the group for the period ended 30 June 2005?

Free

(Multiple Choice)

4.9/5  (28)

(28)

Correct Answer: Verified

Verified

B

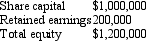

Hammer Ltd acquired all the issued capital of Nail Ltd on 1 July 2005 for cash consideration of $1.5 million.The fair value of the net assets of Nail Ltd at that date was $1.2 million as follows:  During the period ended 30 June 2006,Nail Ltd declared a dividend of $200,000 that is identified as being paid out of pre-acquisition profits and a further $100,000 is declared at the end of the period that is out of post-acquisition profits.Goodwill had been determined to have been impaired by $15,000 during the period.What consolidation journal entries would be required to prepare group accounts for the period ended 30 June 2006?

During the period ended 30 June 2006,Nail Ltd declared a dividend of $200,000 that is identified as being paid out of pre-acquisition profits and a further $100,000 is declared at the end of the period that is out of post-acquisition profits.Goodwill had been determined to have been impaired by $15,000 during the period.What consolidation journal entries would be required to prepare group accounts for the period ended 30 June 2006?

Free

(Multiple Choice)

4.8/5 (45)

Correct Answer:Verified

B

Companies in an economic entity may increase the level of consolidated sales reported by selling inventory between themselves.

Free

(True/False)

4.8/5 (35)

Correct Answer:Verified

False

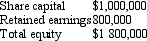

Radio Ltd acquired all the issued capital of Wave Ltd on 1 July 2004 for cash consideration of $2 million.The fair value of the net assets of Wave Ltd at that date was $1.8 million as follows:  During the period ending 30 June 2005 Wave Ltd declare a dividend of $300,000 that is identified as being paid out of pre-acquisition profits.Goodwill had been determined to have impaired by $20,000 during the period.What consolidation journal entries would be required to prepare group accounts for the period ended 30 June 2005?

During the period ending 30 June 2005 Wave Ltd declare a dividend of $300,000 that is identified as being paid out of pre-acquisition profits.Goodwill had been determined to have impaired by $20,000 during the period.What consolidation journal entries would be required to prepare group accounts for the period ended 30 June 2005?

(Multiple Choice)

4.7/5 (28)

If a subsidiary makes a dividend payment out of pre-acquisition earnings,the parent entity should consider whether its investment in the subsidiary is impaired.

(True/False)

4.9/5 (39)

Penny Ltd sells inventory items to its subsidiary Bolt Ltd.If during the financial year 2013,the unrealised profits in ending inventory in Stitch Ltd is less than its unrealised profits in beginning inventory,which of the following statements is correct with respect Penny Ltd's consolidated financial statements after considering these transactions only?

(Multiple Choice)

4.8/5 (38)

Intragroup transactions that are to be eliminated in the consolidated accounts include:

(Multiple Choice)

4.7/5 (34)

Large Company owns 80 per cent of the issued capital of Smaller Company and Large Company owns 60 per cent of the issued capital of Medium Company.The three companies form an economic entity for the purposes of consolidated accounts.During the period Smaller Company sold inventory to Medium for $400,000.Medium sold the same inventory to Large for $560,000 and Large sold it to an entity external to the group for $760,000.What are the sales revenue reported in the consolidated statements for this item?

(Multiple Choice)

4.7/5 (32)

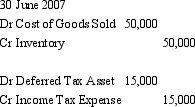

The journal entries to eliminate unrealised profit in closing inventory at 30 June 2007 were as follows.  What are the journal entries to eliminate the unrealised profits in opening inventory the following period?

What are the journal entries to eliminate the unrealised profits in opening inventory the following period?

(Multiple Choice)

4.7/5 (28)

The value of inventory on hand for the economic group at the end of the period will always equal the sum of the inventory on hand at the end of the period for each of the entities in the group:

(True/False)

4.9/5 (37)

Stormy Ltd has purchased all the issued capital of Cloud Ltd at the beginning of the current period.At the end of the period Cloud Ltd declares a dividend of $50,000 that is identified as being paid out of pre-acquisition profits.What entries would Stormy Ltd and Cloud Ltd make in their own books? (Assume Stormy Ltd accrues the dividends of subsidiaries when they are declared.)

(Multiple Choice)

4.8/5 (41)

The treatment of dividends,paid by a subsidiary,that are identified as paid out of pre-acquisition profits in the period they are paid is to:

(Multiple Choice)

4.9/5 (32)

In the absence of an election to be a 'tax consolidated group',the Australian Tax Office assesses income earned by the individual legal entities in an economic group and does not take into consideration consolidation adjustments required for group accounts:

(True/False)

4.8/5 (28)

Belgium Ltd owns all the issued capital of Chocolate Ltd.During the period ended 30 June 2005 Belgium Ltd sold Chocolate Ltd inventory that had a cost of $200,000 for $270,000.At the end of the current period Chocolate Ltd had 75 per cent of that inventory still on hand; the rest was sold to entities external to the group.During the previous period Chocolate Ltd had sold inventory to Belgium Ltd at a profit of $49,000.At the end of that period (30 June 2004)Belgium Ltd still had 40 per cent of that inventory on hand.That entire inventory was sold to parties external to the group during the current year.The taxation rate is 30 per cent and both companies use a perpetual inventory system. What consolidation journal entries are required to eliminate the effects of these transactions for the period ended 30 June 2005?

(Multiple Choice)

4.9/5 (36)

Lilo Ltd sells inventory items to its subsidiary Stitch Ltd.If during the financial year 2013,the unrealised profits in ending inventory in Stitch Ltd exceeds that of its unrealized profits in beginning inventory,which of the following statements is correct with respect Lilo Ltd's consolidated financial statements after considering these transactions only?

(Multiple Choice)

4.8/5 (39)

Question 1: Transactions between entities that form an economic group should be eliminated in proportion to the level of control between the parent entity and the subsidiary entity:

(True/False)

4.8/5 (32)

If we simply aggregate the sales of the parent and subsidiary companies,without adjustment,when there have been intragroup sales,total income would be overstateD.

(True/False)

4.8/5 (40)

Parent Ltd sells inventories to Child Ltd amounting to $200 000 during the financial year.The inventories are no longer in the hands of Child Ltd at year-end.Parent Ltd is no longer required to eliminate these intragroup transactions because these transactions have been realised by sale to external parties.

(True/False)

4.9/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)