Deck 14: Auditing Inventory Processes: Tracking and Costing Products in the Land Development and Home Building Industry

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

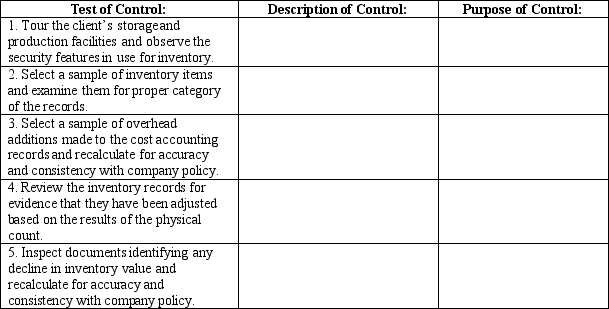

The following tests of controls are being performed on the audit of Hoppes Homes, Inc. For each test of control, fill in the table to indicate the corresponding control and the purpose of the control.

Question

Question

Question

Question

Question

Question

Question

Match between columns

Question

Match between columns

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/64

Play

Full screen (f)

Deck 14: Auditing Inventory Processes: Tracking and Costing Products in the Land Development and Home Building Industry

1

Management may estimate costs of material, labor, and overhead for each unit of inventory based upon experience and/or engineering specifications.

True

2

In a manufacturing environment using a backflush system, a typical trigger for posting inventory transactions is the company's vulnerability to shrinkage losses.

False

3

Which types of inventory transactions are not likely to create variable interest entities that would require consolidation?

A) Land purchase contracts.

B) Joint ventures.

C) Percentage of completion contracts.

D) Options for future land purchases.

A) Land purchase contracts.

B) Joint ventures.

C) Percentage of completion contracts.

D) Options for future land purchases.

C

4

FSAS 151 requires that abnormal overhead costs be allocated to products based on excess capacity of the facilities.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

5

When using the percentage of completion method, the amount of revenue recognized in the current period is calculated using the proportion of total expected product costs relative to costs incurred to date.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

6

Controls in the inventory cycle that support proper records of units and costs cannot be effective unless the documentation and controls for purchasing, payroll, and sales are also effective.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

7

Observation is the form of audit evidence typically used for testing the operating effectiveness of many of the physical controls over inventory.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

8

Manufacturing entities using standard costing systems should avoid the use of accounting estimates in order to reduce the likelihood of audit adjustments.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

9

Direct tracing is a cost accounting technique for tracking individual costs associated with a manufactured product or production process.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

10

Dual purpose tests performed in the planning stages of the audit inform the auditor regarding changes in the inventory that will influence the audit procedures required by this cycle.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

11

Homebuilders need not be concerned with unasserted claims because future risks do not require disclosure in the financial statements.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

12

Auditors are responsible for setting up procedures for a physical inventory count that will be observed by management

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following statements is true regarding the complex nature of inventory accounting in the land development and home building industry?

A) Common costs, such as capitalized interest, often require complex calculations.

B) The size and type of units to which costs must be allocated for a single parcel of land may vary considerably.

C) Costs associated with zoning applications and legal fees may occur in periods prior to the land acquisition.

D) All of the above are true.

A) Common costs, such as capitalized interest, often require complex calculations.

B) The size and type of units to which costs must be allocated for a single parcel of land may vary considerably.

C) Costs associated with zoning applications and legal fees may occur in periods prior to the land acquisition.

D) All of the above are true.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

14

Residential home building companies are primarily involved in which of the following business activities?

A) Community planning and construction.

B) Financing residential mortgages.

C) Selling land plots to developers.

D) Design of residential community centers.

A) Community planning and construction.

B) Financing residential mortgages.

C) Selling land plots to developers.

D) Design of residential community centers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

15

In the land development and home building industry, the cost of a parcel of land must be allocated to the various residential units and other facilities in a community.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following is the method of allocating costs to individual residential units in the land development and home building industry?

A) Variable costing.

B) Job order costing.

C) Historical costing.

D) Acquisition costing.

A) Variable costing.

B) Job order costing.

C) Historical costing.

D) Acquisition costing.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

17

In the land development and home building industry, materials costs are typically added to the inventory cost of a specific unit based on actual purchases prices except when:

A) subcontractors are used, in which case the costs cannot be directly traced to plan specifications.

B) multifamily residences are constructed, in which case it is necessary to allocate common costs.

C) job order costing is used, in which case the specific identification method cannot be applied.

D) large quantities of building materials are purchased that cannot be tracked to individual units.

A) subcontractors are used, in which case the costs cannot be directly traced to plan specifications.

B) multifamily residences are constructed, in which case it is necessary to allocate common costs.

C) job order costing is used, in which case the specific identification method cannot be applied.

D) large quantities of building materials are purchased that cannot be tracked to individual units.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

18

At the end of the accounting period, adjustments for under- or overapplied overhead are simply posted to the inventory accounts.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

19

One method for testing cutoff and in-transit inventory is for the auditor to examine shipping documents for a few days before and after year-end and determine whether the inventory records properly reflect the transaction in the correct period.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

20

A construction problem that is not immediately evident is referred to as a latent defect.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following is true regarding perpetual inventory systems?

A) Detailed accounting records must be maintained so that changes in inventory accounts can be posted when the transactions occur.

B) An end-of period physical inventory count is required to determine the changes in inventory accounts.

C) Detailed accounting records must be maintained so that changes in inventory accounts can be posted in a purchases account.

D) More accounting time is required at the end of the period to update the inventory accounts for the period's changes.

A) Detailed accounting records must be maintained so that changes in inventory accounts can be posted when the transactions occur.

B) An end-of period physical inventory count is required to determine the changes in inventory accounts.

C) Detailed accounting records must be maintained so that changes in inventory accounts can be posted in a purchases account.

D) More accounting time is required at the end of the period to update the inventory accounts for the period's changes.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

22

When a company's cost accounting system uses process costing, work-in-process is accumulated based on:

A) batches.

B) specific inventory projects.

C) raw materials less shrinkage.

D) periodic labor charts.

A) batches.

B) specific inventory projects.

C) raw materials less shrinkage.

D) periodic labor charts.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following business functions or activities is unique to the manufacturing industry with respect to the production of finished goods from raw materials?

A) An effective cost accounting function.

B) An effective inventory stores function.

C) The requirement for a physical inventory count at year-end.

D) The consideration of impairment losses.

A) An effective cost accounting function.

B) An effective inventory stores function.

C) The requirement for a physical inventory count at year-end.

D) The consideration of impairment losses.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

24

The purpose of a materials requisition form is to:

A) track work-in process inventory so the appropriate percentage of completion proportion can be computed.

B) authorize the release of raw materials into work-in-process.

C) trigger the accounting entry to reduce raw materials inventory records and increase finished goods.

D) update the general ledger for the movement of materials into finished goods.

A) track work-in process inventory so the appropriate percentage of completion proportion can be computed.

B) authorize the release of raw materials into work-in-process.

C) trigger the accounting entry to reduce raw materials inventory records and increase finished goods.

D) update the general ledger for the movement of materials into finished goods.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

25

GAAP requires the use of _______ costing for accumulating all direct and allocated costs to inventory units.

A) job order

B) absorption

C) backflush

D) fair value

A) job order

B) absorption

C) backflush

D) fair value

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

26

Physical controls over inventory are typically tested for operating effectiveness by:

A) confirmation.

B) observation.

C) walkthrough.

D) reconciliation.

A) confirmation.

B) observation.

C) walkthrough.

D) reconciliation.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

27

When applying the percentage of completion method, companies in the land development and home building industry must first:

A) estimate the actual costs to be incurred in the current period.

B) calculate a percentage to designate for inventory costing.

C) trace costs incurred to date for each residential unit to the inventory accounting records.

D) estimate the proportion of actual costs incurred relative to total expected costs.

A) estimate the actual costs to be incurred in the current period.

B) calculate a percentage to designate for inventory costing.

C) trace costs incurred to date for each residential unit to the inventory accounting records.

D) estimate the proportion of actual costs incurred relative to total expected costs.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

28

Overhead costs are also known as:

A) direct costs.

B) work-in-process costs.

C) tracked costs.

D) indirect costs.

A) direct costs.

B) work-in-process costs.

C) tracked costs.

D) indirect costs.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following tests should be performed by an auditor to ensure that all completed inventory is physically moved to finished goods and that the inventory records are updated concurrent with the physical movement?

A) Evaluate whether management's inventory count controls and procedures are appropriate and observe inventory counting to assess whether the procedures are being followed.

B) Inspect the inventory records for evidence that they have been properly adjusted based on the results of the physical counts.

C) For a sample of finished goods inventory items, agree the increase in the finished goods inventory records to a corresponding decrease in work-in-process for the same date.

D) For a sample of finished goods inventory items, agree the increase in the finished goods inventory records to a corresponding decrease in raw materials, purchasing, and payroll.

A) Evaluate whether management's inventory count controls and procedures are appropriate and observe inventory counting to assess whether the procedures are being followed.

B) Inspect the inventory records for evidence that they have been properly adjusted based on the results of the physical counts.

C) For a sample of finished goods inventory items, agree the increase in the finished goods inventory records to a corresponding decrease in work-in-process for the same date.

D) For a sample of finished goods inventory items, agree the increase in the finished goods inventory records to a corresponding decrease in raw materials, purchasing, and payroll.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

30

An inventory posting method which uses "triggers" to indicate when inventory has passed through a manufacturing stage is:

A) perpetual.

B) periodic.

C) weighted average.

D) backflush.

A) perpetual.

B) periodic.

C) weighted average.

D) backflush.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

31

In order to obtain audit evidence about account balances, many tests of controls may be enhanced by the added activity of tracing the sampled items from the inventory compilation report and verifying that the compilation amounts agree with the general ledger. This enhanced test would be considered a:

A) substantive procedure.

B) dual-purpose test.

C) walkthrough.

D) physical inventory count.

A) substantive procedure.

B) dual-purpose test.

C) walkthrough.

D) physical inventory count.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

32

Over- and underapplied overhead variances are typically allocated among:

A) direct materials, direct labor, and manufacturing overhead.

B) raw materials, work-in-process, and finished goods inventory.

C) the inventory accounts and cost of goods sold.

D) the inventory and human resources-related accounts.

A) direct materials, direct labor, and manufacturing overhead.

B) raw materials, work-in-process, and finished goods inventory.

C) the inventory accounts and cost of goods sold.

D) the inventory and human resources-related accounts.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

33

Physical controls over inventories are important in a manufacturing environment because they enhance management's ability to:

A) produce credible financial reports.

B) prevent "in-house" losses such as theft and damage of inventory.

C) detect inefficient or ineffective manufacturing operations.

D) correct errors resulting from the physical inventory count.

A) produce credible financial reports.

B) prevent "in-house" losses such as theft and damage of inventory.

C) detect inefficient or ineffective manufacturing operations.

D) correct errors resulting from the physical inventory count.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

34

For planned communities, common costs can be allocated to individual residential units using the:

A) relative interest allocation method.

B) relative capitalization of costs method.

C) relative area or relative sales value allocation method.

D) relative impact estimation process.

A) relative interest allocation method.

B) relative capitalization of costs method.

C) relative area or relative sales value allocation method.

D) relative impact estimation process.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

35

To ensure that a client's raw materials, work-in-process, and finished goods inventories are physically protected from theft or damage, an auditor could perform a test of controls such as:

A) selecting a sample of inventory items from the inventory records and inspecting them for consistency with the category of records.

B) reviewing the company's inventory policies for adherence to GAAP.

C) observing the client's physical inventory count to assess whether the company's procedures are being followed.

D) touring the storage and production facilities and observe the security procedures in place.

A) selecting a sample of inventory items from the inventory records and inspecting them for consistency with the category of records.

B) reviewing the company's inventory policies for adherence to GAAP.

C) observing the client's physical inventory count to assess whether the company's procedures are being followed.

D) touring the storage and production facilities and observe the security procedures in place.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

36

For which of the following circumstances would it be appropriate for an auditor to examine the inventory records for evidence of adjustment based on results of the physical count?

A) To ensure that the process for the physical count of inventory includes proper procedures.

B) To ensure that the correct result of the physical count, in conjunction with cost information, is used to update the accounting records.

C) To ensure that the policies for assessing inventory valuation are appropriate.

D) To ensure that the inventory records are updated for physical movement of items within the production process.

A) To ensure that the process for the physical count of inventory includes proper procedures.

B) To ensure that the correct result of the physical count, in conjunction with cost information, is used to update the accounting records.

C) To ensure that the policies for assessing inventory valuation are appropriate.

D) To ensure that the inventory records are updated for physical movement of items within the production process.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

37

An auditor may select a sample of items from the inventory records and inspect them for consistency with the category of the records. The purpose of this test of controls is to ensure that:

A) recorded inventory exists.

B) inventories are physically protected from theft or damage.

C) policies for assessing inventory valuation are appropriate.

D) proper procedures are followed for the process of the physical count.

A) recorded inventory exists.

B) inventories are physically protected from theft or damage.

C) policies for assessing inventory valuation are appropriate.

D) proper procedures are followed for the process of the physical count.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

38

If a client company performs its physical inventory counts on a date other than year-end, auditors must verify that:

A) no shrinkage results.

B) there are no discrepancies between accounting records and goods on hand as of the date of the physical count.

C) the count data is rolled forward or rolled back to the financial statements based on transaction data between the dates of the physical count and year-end.

D) authorization controls applied during the period were sufficient to prevent losses between the dates of the physical count and year-end.

A) no shrinkage results.

B) there are no discrepancies between accounting records and goods on hand as of the date of the physical count.

C) the count data is rolled forward or rolled back to the financial statements based on transaction data between the dates of the physical count and year-end.

D) authorization controls applied during the period were sufficient to prevent losses between the dates of the physical count and year-end.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

39

A manufacturer's definition of raw materials would be:

A) natural goods that have never been processed.

B) inputs to production.

C) outputs from production.

D) processed goods that await inventory recordkeeping.

A) natural goods that have never been processed.

B) inputs to production.

C) outputs from production.

D) processed goods that await inventory recordkeeping.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

40

Which of the following is not a control concern for inventory?

A) Inventory records are adjusted to reflect the inventory that has been verified through a physical count.

B) Any decrement in inventory value is properly reflected in the amounts.

C) Inventory is safeguarded through all stages of movement and the production process.

D) Reported inventory amounts are properly estimated through management authorization of completeness.

A) Inventory records are adjusted to reflect the inventory that has been verified through a physical count.

B) Any decrement in inventory value is properly reflected in the amounts.

C) Inventory is safeguarded through all stages of movement and the production process.

D) Reported inventory amounts are properly estimated through management authorization of completeness.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

41

Which of the following is an appropriate substantive test of details of account balances for the inventory cycle for the verification of an accurate cutoff?

A) Test movements between raw materials, work-in-process, and finished goods by selecting transactions from the inventory records and examining supporting documents.

B) Reperform calculations testing mathematical accuracy including total extensions of price and quantity and unit or batch aggregations.

C) Examine shipping documents for a few days before and after year end and trace to inventory records, agreeing for proper inclusion and exclusion.

D) Review and recalculate client's analysis supporting adjustments resulting from the physical inventory count.

A) Test movements between raw materials, work-in-process, and finished goods by selecting transactions from the inventory records and examining supporting documents.

B) Reperform calculations testing mathematical accuracy including total extensions of price and quantity and unit or batch aggregations.

C) Examine shipping documents for a few days before and after year end and trace to inventory records, agreeing for proper inclusion and exclusion.

D) Review and recalculate client's analysis supporting adjustments resulting from the physical inventory count.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

42

In order for an auditor to test ownership of a client's inventories, each of the following substantive tests of details of account balances are appropriate except:

A) review loan agreements for inventory that has been pledged or assigned.

B) review sales agreements for bill-and-hold arrangements.

C) review contracts for inventory held on consignment.

D) review policy for asset impairment write-downs.

A) review loan agreements for inventory that has been pledged or assigned.

B) review sales agreements for bill-and-hold arrangements.

C) review contracts for inventory held on consignment.

D) review policy for asset impairment write-downs.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

43

Which of the following is not an acceptable manner of testing an audit client's estimates?

A) Compare subsequent actual amounts to the accounting estimates.

B) Recalculate accounting estimates using management's process.

C) Prepare an independent estimate and compare with management's result.

D) Observe management's process of calculating estimates.

A) Compare subsequent actual amounts to the accounting estimates.

B) Recalculate accounting estimates using management's process.

C) Prepare an independent estimate and compare with management's result.

D) Observe management's process of calculating estimates.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

44

Which of the following audit steps for observing a client's inventory count are to be performed after the physical count is complete?

A) Obtain the number of the receiving report and shipping document for the last item of the period and check to see that the inventory is properly included or excluded.

B) Inquire of client's management about whether any inventory owned by others is held on consignment.

C) Trace items selected and included in audit test recounts into the client's inventory records.

D) Check for the sequential numbering of tags used in the physical counts, including identification of all used and unused numbers.

A) Obtain the number of the receiving report and shipping document for the last item of the period and check to see that the inventory is properly included or excluded.

B) Inquire of client's management about whether any inventory owned by others is held on consignment.

C) Trace items selected and included in audit test recounts into the client's inventory records.

D) Check for the sequential numbering of tags used in the physical counts, including identification of all used and unused numbers.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

45

A test of controls can be modified to be performed as a dual purpose test if the modification provides evidence about the related account balances. Describe a substantive procedure that can be added to a test of controls in order make it a dual purpose test. The substantive procedure you identify must be one that could be added to most any test of controls involving a sample selection or mathematical verification.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

46

When ICFR and the quality of perpetual inventory records justify relying on an inventory count by the company at other than fiscal year end, the auditor's testing should include each of the following except:

A) verification of inventory purchases occurring during the period between the time of the physical count and year end.

B) tests of controls performed during the period between the time of the physical count and year end.

C) reconciliation of the count result to the final inventory balances in the financial statements.

D) verification of sales transactions during the period between the time of the physical count and year end.

A) verification of inventory purchases occurring during the period between the time of the physical count and year end.

B) tests of controls performed during the period between the time of the physical count and year end.

C) reconciliation of the count result to the final inventory balances in the financial statements.

D) verification of sales transactions during the period between the time of the physical count and year end.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

47

Land development and home building companies provide warranties for:

A) impaired assets.

B) manufacturer's defects and latent defects.

C) amenities.

D) obsolete or slow-moving items.

MATCHING

A) impaired assets.

B) manufacturer's defects and latent defects.

C) amenities.

D) obsolete or slow-moving items.

MATCHING

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

48

Which of the following is true regarding an auditor's assessment of management estimates for calculations related to inventory valuation in the land development and home building industry?

A) Greater uncertainty exists regarding estimates of future cash flows when development and construction are still in the early stages.

B) Since prospective buyers can cancel the contracts, management estimates expected cancellations using current engineering specifications.

C) If an auditor assessed the company's process and underlying assumptions in a prior period, the assessment does not need to be updated for subsequent audits unless there is a change in the underlying assumptions.

D) Auditors typically engage a specialist to perform detailed calculations of discounted cash flows expected from inventory.

A) Greater uncertainty exists regarding estimates of future cash flows when development and construction are still in the early stages.

B) Since prospective buyers can cancel the contracts, management estimates expected cancellations using current engineering specifications.

C) If an auditor assessed the company's process and underlying assumptions in a prior period, the assessment does not need to be updated for subsequent audits unless there is a change in the underlying assumptions.

D) Auditors typically engage a specialist to perform detailed calculations of discounted cash flows expected from inventory.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

49

When well-maintained perpetual inventory records are verified periodically by the client by comparisons with physical counts, what is the appropriate timing of the auditor's observation procedures?

A) Either during the period under audit or at the balance sheet date.

B) Either during or after the end of the period under audit.

C) Only at the balance sheet date.

D) Only during the end of the period under audit.

A) Either during the period under audit or at the balance sheet date.

B) Either during or after the end of the period under audit.

C) Only at the balance sheet date.

D) Only during the end of the period under audit.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

50

In order for an auditor to test valuation of a client's inventories, each of the following substantive tests of details of account balances are appropriate except:

A) using computer-assisted auditing techniques, reperform calculations testing the mathematical accuracy of report extensions and batch aggregations.

B) reperform calculations supporting decisions about inventory write-downs or write-offs.

C) obtain documentation supporting amounts of obsolete or slow-moving inventory items.

D) evaluate any changes made to the client's impairment policies in light of engineering and production information or other underlying assumptions.

A) using computer-assisted auditing techniques, reperform calculations testing the mathematical accuracy of report extensions and batch aggregations.

B) reperform calculations supporting decisions about inventory write-downs or write-offs.

C) obtain documentation supporting amounts of obsolete or slow-moving inventory items.

D) evaluate any changes made to the client's impairment policies in light of engineering and production information or other underlying assumptions.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

51

In accounting for inventory, the quality of estimates made by a client's management is directly related to:

A) the likelihood of error in the allocation of common costs.

B) the strength of internal controls of the inventory process.

C) the degree of sophistication of the client's automated inventory processes.

D) the number of tags or count sheets used in the client's physical inventory count.

A) the likelihood of error in the allocation of common costs.

B) the strength of internal controls of the inventory process.

C) the degree of sophistication of the client's automated inventory processes.

D) the number of tags or count sheets used in the client's physical inventory count.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

52

Which of the following measures is not a good example of a substantive analytical procedure for inventory activities and related accounts?

A) The inventory turnover ratio.

B) Gross profit margin ratio.

C) Current ratio.

D) Number of days sales in inventory.

A) The inventory turnover ratio.

B) Gross profit margin ratio.

C) Current ratio.

D) Number of days sales in inventory.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

53

An auditor generally concludes that a client's estimate is appropriate if:

A) it is consistent with a prior year amount.

B) the underlying amount is not known with certainty.

C) it is within a range of acceptable amounts.

D) the underlying assumptions are subjective.

A) it is consistent with a prior year amount.

B) the underlying amount is not known with certainty.

C) it is within a range of acceptable amounts.

D) the underlying assumptions are subjective.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

54

Analytical procedures can help an auditor assess the reasonableness of the inventory balances by highlighting changes that:

A) suggest slow-moving inventory for possible obsolescence.

B) address whether inventory includes operating costs that should be expensed rather than capitalized.

C) compare the reasonableness of inventory balances with purchases and cost of goods sold.

D) All of the above.

A) suggest slow-moving inventory for possible obsolescence.

B) address whether inventory includes operating costs that should be expensed rather than capitalized.

C) compare the reasonableness of inventory balances with purchases and cost of goods sold.

D) All of the above.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

55

While auditing a client's inventory processes, an auditor computes the gross profit margin ratio and compares it to prior years and budgeted amounts. If the result indicates that the gross profit margin has increased since the prior year and exceeds the budget, it is likely that:

A) ending inventory is overstated and cost of goods sold is understated.

B) both inventory and cost of goods sold is overstated.

C) both inventory and cost of goods sold is understated.

D) ending inventory is understated and cost of goods sold is overstated.

A) ending inventory is overstated and cost of goods sold is understated.

B) both inventory and cost of goods sold is overstated.

C) both inventory and cost of goods sold is understated.

D) ending inventory is understated and cost of goods sold is overstated.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

56

The following tests of controls are being performed on the audit of Hoppes Homes, Inc. For each test of control, fill in the table to indicate the corresponding control and the purpose of the control.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

57

Which of the following is the most appropriate test for auditing inventory in the land development and home building industry?

A) Examine subsequent invoices received in support of estimates of the cost of sales for individual units sold just before year end.

B) Calculate estimated ending inventory using standards and variance information.

C) Review sales contracts for bill-and-hold transactions.

D) All of the above tests are common in the land development and home building industry.

A) Examine subsequent invoices received in support of estimates of the cost of sales for individual units sold just before year end.

B) Calculate estimated ending inventory using standards and variance information.

C) Review sales contracts for bill-and-hold transactions.

D) All of the above tests are common in the land development and home building industry.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

58

Which of the following documents is most likely to provide evidence to support the validity of estimates used in a client's standard costing system?

A) Variance reports.

B) Consignment confirmations.

C) Materials requisitions.

D) Purchase orders.

A) Variance reports.

B) Consignment confirmations.

C) Materials requisitions.

D) Purchase orders.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

59

What estimates are included in the cost of inventory in the land development and home building industry? Specifically, what past costs are allocated? What future amounts must be predicted? What future amounts must be predicted and allocated? Distinguish

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

60

Ballpark Distributors, Inc. is a large public company with a calendar year end that distributes sports memorabilia to various retailers. Ballpark conducted an inventory count on November 30 of the year being audited. Instead of conducting another inventory count at year end, the company decided to estimate the year-end inventory using a sample of the year-end inventory on hand. The company uses a perpetual inventory system and feels that sampling to estimate the year-end inventory will produce a reliable financial statement amount.

Required:

Assume that the auditor observed and tested Ballpark's physical inventory count on

November 30, and was satisfied that the count and resulting adjustments produced

an appropriate inventory account balance on November 30.

(a)What roll-forward procedures between the inventory count date and year end

might the auditor perform?

(b)What additional tests of details of balances can the auditor perform?

Required:

Assume that the auditor observed and tested Ballpark's physical inventory count on

November 30, and was satisfied that the count and resulting adjustments produced

an appropriate inventory account balance on November 30.

(a)What roll-forward procedures between the inventory count date and year end

might the auditor perform?

(b)What additional tests of details of balances can the auditor perform?

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

61

Explain how auditing inventory of a company with a standard cost system requires an audit of estimates.What are the estimates? What procedures would the auditor perform related to variances produced by the system at year end? Why?

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

62

You are assigned to the audit of Hopewell Homebuilders, Inc., a new audit client. Hopewell uses a standard costing system for inventory accounting. What audit procedures are appropriate for evaluating the reasonableness of management's estimates and underlying assumptions used in a standard costing system?

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

63

Match between columns

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

64

Match between columns

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 64 flashcards in this deck.