Deck 8: Monopoly

Full screen (f)

Question

Question

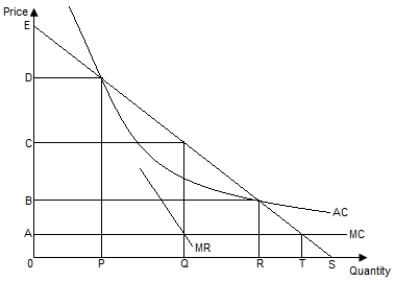

The following figure shows the demand curve ES, the average cost curve AC, the marginal cost curve MC, and the marginal revenue curve MR for a firm.

Figure 8-1

Refer to Figure 8-1. The efficient level of output in the market is:

A) R - P.

B) R.

C) Q.

D) P.

E) T.

Figure 8-1

Refer to Figure 8-1. The efficient level of output in the market is:

A) R - P.

B) R.

C) Q.

D) P.

E) T.

Question

The following figure shows the demand curve ES, the average cost curve AC, the marginal cost curve MC, and the marginal revenue curve MR for a firm.

Figure 8-1

Refer to Figure 8-1. Under average-cost pricing, the equilibrium price and output in the market are _____, respectively.

A) B and R

B) A and T

C) C and Q

D) D and P

E) A and Q

Figure 8-1

Refer to Figure 8-1. Under average-cost pricing, the equilibrium price and output in the market are _____, respectively.

A) B and R

B) A and T

C) C and Q

D) D and P

E) A and Q

Question

Question

Question

The following figure shows the demand curve ES, the average cost curve AC, the marginal cost curve MC, and the marginal revenue curve MR for a firm.

Figure 8-1

Refer to Figure 8-1. If the regulator institutes marginal-cost pricing in the market, then:

A) MC = AC.

B) P = AC.

C) MR = MC.

D) P = MC > AC.

E) P = MC < AC.

Figure 8-1

Refer to Figure 8-1. If the regulator institutes marginal-cost pricing in the market, then:

A) MC = AC.

B) P = AC.

C) MR = MC.

D) P = MC > AC.

E) P = MC < AC.

Question

Question

Question

Question

Question

Question

Question

Question

The following figure shows the demand curve ES, the average cost curve AC, the marginal cost curve MC, and the marginal revenue curve MR for a firm.

Figure 8-1

Refer to Figure 8-1. If the firm operates as a monopoly in an unregulated market, its profit-maximizing price and output would be _____, respectively.

A) C and Q

B) A and Q

C) B and R

D) D and P

E) A and T

Figure 8-1

Refer to Figure 8-1. If the firm operates as a monopoly in an unregulated market, its profit-maximizing price and output would be _____, respectively.

A) C and Q

B) A and Q

C) B and R

D) D and P

E) A and T

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/51

Play

Full screen (f)

Deck 8: Monopoly

1

A monopolist produces and sells 400 units at a price of $40 per unit. The monopolist's marginal cost is equal to $15 and average cost is equal to $23. The monopolist's profit is:

A) $6,800.

B) $8,000.

C) $10,000.

D) $16,000.

E) None of these are correct.

A) $6,800.

B) $8,000.

C) $10,000.

D) $16,000.

E) None of these are correct.

A

2

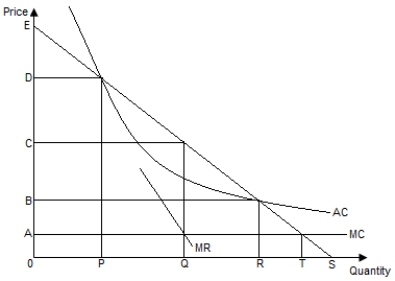

The following figure shows the demand curve ES, the average cost curve AC, the marginal cost curve MC, and the marginal revenue curve MR for a firm.

Figure 8-1

Refer to Figure 8-1. The efficient level of output in the market is:

A) R - P.

B) R.

C) Q.

D) P.

E) T.

Figure 8-1

Refer to Figure 8-1. The efficient level of output in the market is:

A) R - P.

B) R.

C) Q.

D) P.

E) T.

E

3

The following figure shows the demand curve ES, the average cost curve AC, the marginal cost curve MC, and the marginal revenue curve MR for a firm.

Figure 8-1

Refer to Figure 8-1. Under average-cost pricing, the equilibrium price and output in the market are _____, respectively.

A) B and R

B) A and T

C) C and Q

D) D and P

E) A and Q

Figure 8-1

Refer to Figure 8-1. Under average-cost pricing, the equilibrium price and output in the market are _____, respectively.

A) B and R

B) A and T

C) C and Q

D) D and P

E) A and Q

A

4

Which of the following is a characteristic of a firm that is a natural monopoly?

A) The firm's average costs decline over all levels of output.

B) The firm's elasticity of supply is very low.

C) The firm does not incur any sunk costs.

D) The firm faces a horizontal demand curve.

E) The firm makes zero economic profit.

A) The firm's average costs decline over all levels of output.

B) The firm's elasticity of supply is very low.

C) The firm does not incur any sunk costs.

D) The firm faces a horizontal demand curve.

E) The firm makes zero economic profit.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following is true of a pure monopoly?

A) A pure monopoly can raise the market price indefinitely.

B) A pure monopoly is typically more efficient than other firms in the market.

C) A pure monopoly faces a horizontal demand curve.

D) A pure monopoly restricts output below the competitive level.

E) A pure monopoly produces at the level where price equals marginal cost.

A) A pure monopoly can raise the market price indefinitely.

B) A pure monopoly is typically more efficient than other firms in the market.

C) A pure monopoly faces a horizontal demand curve.

D) A pure monopoly restricts output below the competitive level.

E) A pure monopoly produces at the level where price equals marginal cost.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

6

The following figure shows the demand curve ES, the average cost curve AC, the marginal cost curve MC, and the marginal revenue curve MR for a firm.

Figure 8-1

Refer to Figure 8-1. If the regulator institutes marginal-cost pricing in the market, then:

A) MC = AC.

B) P = AC.

C) MR = MC.

D) P = MC > AC.

E) P = MC < AC.

Figure 8-1

Refer to Figure 8-1. If the regulator institutes marginal-cost pricing in the market, then:

A) MC = AC.

B) P = AC.

C) MR = MC.

D) P = MC > AC.

E) P = MC < AC.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following is a criticism of average-cost pricing as a regulatory response to a natural monopoly?

A) With average-cost pricing, output produced is smaller than the efficient level of output.

B) Firms that practice average-cost pricing suffer persistent losses.

C) Imperfect information about the firm's costs reduces the effectiveness of average-cost pricing.

D) Under average-cost pricing, the market price is lower than the efficient price.

E) Answers with average-cost pricing, output produced is smaller than the efficient level of output and imperfect information about the firm's costs reduces the effectiveness of average-cost pricing are both correct.

A) With average-cost pricing, output produced is smaller than the efficient level of output.

B) Firms that practice average-cost pricing suffer persistent losses.

C) Imperfect information about the firm's costs reduces the effectiveness of average-cost pricing.

D) Under average-cost pricing, the market price is lower than the efficient price.

E) Answers with average-cost pricing, output produced is smaller than the efficient level of output and imperfect information about the firm's costs reduces the effectiveness of average-cost pricing are both correct.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following is true of a profit-maximizing competitive firm in the short run?

A) The firm produces at the point where price is equal to marginal cost.

B) The firm produces at the point where average cost is at its minimum point.

C) The demand curve faced by each firm in the industry is downward sloping.

D) The firm always makes a zero economic profit.

E) The firm suffers a deadweight loss.

A) The firm produces at the point where price is equal to marginal cost.

B) The firm produces at the point where average cost is at its minimum point.

C) The demand curve faced by each firm in the industry is downward sloping.

D) The firm always makes a zero economic profit.

E) The firm suffers a deadweight loss.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

9

Industry demand is given by P = 200 - .4Q. The long-run industry costs are such that: LAC = LMC = $80. Based on this information, which of the following is true?

A) If the market is a pure monopoly, the price of the good will be $140.

B) If the market is perfectly competitive, 300 units of the good will be supplied.

C) If the market is perfectly competitive, the price of the good will be $100.

D) If the market is a pure monopoly, 200 units of the good will be produced.

E) Answers if the market is a pure monopoly, the price of the good will be $140 and if the market is perfectly competitive, 300 units of the good will be supplied are both correct.

A) If the market is a pure monopoly, the price of the good will be $140.

B) If the market is perfectly competitive, 300 units of the good will be supplied.

C) If the market is perfectly competitive, the price of the good will be $100.

D) If the market is a pure monopoly, 200 units of the good will be produced.

E) Answers if the market is a pure monopoly, the price of the good will be $140 and if the market is perfectly competitive, 300 units of the good will be supplied are both correct.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

10

A monopolist maximizes profit by producing:

A) on the inelastic portion of the demand curve

B) at the level where average cost is minimized

C) at the point where the cost of producing the last unit of output equals price.

D) at the output level where marginal revenue equals marginal cost

E) at the level where the deadweight loss is minimized.

A) on the inelastic portion of the demand curve

B) at the level where average cost is minimized

C) at the point where the cost of producing the last unit of output equals price.

D) at the output level where marginal revenue equals marginal cost

E) at the level where the deadweight loss is minimized.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

11

A market is considered a pure monopoly when:

A) all firms in the market sell homogeneous goods.

B) there is a single buyer for the goods produced in the market.

C) the firm produces a good that has imperfect substitutes.

D) a single firm produces a good that has no close substitutes.

E) there are low entry barriers in the market.

A) all firms in the market sell homogeneous goods.

B) there is a single buyer for the goods produced in the market.

C) the firm produces a good that has imperfect substitutes.

D) a single firm produces a good that has no close substitutes.

E) there are low entry barriers in the market.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

12

A monopoly earns positive economic profits in the long run because:

A) there are barriers to entry in the market.

B) demand in a monopoly market is perfectly inelastic.

C) it faces a kinked demand curve.

D) it operates with constant returns to scale.

E) it operates with an optimal plant size.

A) there are barriers to entry in the market.

B) demand in a monopoly market is perfectly inelastic.

C) it faces a kinked demand curve.

D) it operates with constant returns to scale.

E) it operates with an optimal plant size.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

13

Cartels are inherently unstable because individual members:

A) face horizontal demand curves.

B) tend to produce above their quotas.

C) are culturally and politically heterogeneous.

D) produce highly differentiated products.

E) have a low elasticity of supply.

A) face horizontal demand curves.

B) tend to produce above their quotas.

C) are culturally and politically heterogeneous.

D) produce highly differentiated products.

E) have a low elasticity of supply.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

14

The following figure shows the demand curve ES, the average cost curve AC, the marginal cost curve MC, and the marginal revenue curve MR for a firm.

Figure 8-1

Refer to Figure 8-1. If the firm operates as a monopoly in an unregulated market, its profit-maximizing price and output would be _____, respectively.

A) C and Q

B) A and Q

C) B and R

D) D and P

E) A and T

Figure 8-1

Refer to Figure 8-1. If the firm operates as a monopoly in an unregulated market, its profit-maximizing price and output would be _____, respectively.

A) C and Q

B) A and Q

C) B and R

D) D and P

E) A and T

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

15

If the regulator institutes average-cost pricing in a natural monopoly market, then:

A) the firm makes zero economic profit.

B) the firm has an incentive to produce at minimum cost.

C) the marginal benefit to the consumer is less than marginal cost to the firm.

D) firms in the market will produce at the efficient level.

E) consumer surplus in the market is maximized.

A) the firm makes zero economic profit.

B) the firm has an incentive to produce at minimum cost.

C) the marginal benefit to the consumer is less than marginal cost to the firm.

D) firms in the market will produce at the efficient level.

E) consumer surplus in the market is maximized.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

16

The basic objective of a cartel is to:

A) maximize profit for the largest, most influential members.

B) increase the total consumer surplus in the market.

C) produce the highest output level possible.

D) secure monopoly profits for its members.

E) successfully practice price discrimination in the market.

A) maximize profit for the largest, most influential members.

B) increase the total consumer surplus in the market.

C) produce the highest output level possible.

D) secure monopoly profits for its members.

E) successfully practice price discrimination in the market.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following does not contribute to the existence of monopoly power?

A) A continuously decreasing long-run average cost curve

B) The possession of a patent

C) The control of essential inputs in the production process

D) A pure cost or quality advantage

E) A relatively inelastic market demand curve

A) A continuously decreasing long-run average cost curve

B) The possession of a patent

C) The control of essential inputs in the production process

D) A pure cost or quality advantage

E) A relatively inelastic market demand curve

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following is true of pure monopolies?

A) Monopolies earn positive economic profits in the long run.

B) Monopolies produce output that is greater than the competitive level.

C) Monopolies produce products that have a negligible marginal cost but a high fixed cost.

D) Monopolies reduce welfare by engaging in excessive product differentiation.

E) Answers monopolies earn positive economic profits in the long run and monopolies reduce welfare by engaging in excessive product differentiation are both correct.

A) Monopolies earn positive economic profits in the long run.

B) Monopolies produce output that is greater than the competitive level.

C) Monopolies produce products that have a negligible marginal cost but a high fixed cost.

D) Monopolies reduce welfare by engaging in excessive product differentiation.

E) Answers monopolies earn positive economic profits in the long run and monopolies reduce welfare by engaging in excessive product differentiation are both correct.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is likely to take place if regulators split a natural monopoly into two smaller firms?

A) The number of firms in the market will increase but the market price will be unchanged.

B) The output in the industry will increase.

C) The cost of production in the industry will increase.

D) The market demand curve will become flatter.

E) The total industry profits will increase.

A) The number of firms in the market will increase but the market price will be unchanged.

B) The output in the industry will increase.

C) The cost of production in the industry will increase.

D) The market demand curve will become flatter.

E) The total industry profits will increase.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

20

Compared to a perfectly competitive industry, a monopolist will generally produce:

A) a greater level of output a lower price.

B) a greater level of output at a higher price.

C) a smaller level of output a lower price.

D) a smaller level of output at a higher price.

E) roughly the same level of output but at a higher price.

A) a greater level of output a lower price.

B) a greater level of output at a higher price.

C) a smaller level of output a lower price.

D) a smaller level of output at a higher price.

E) roughly the same level of output but at a higher price.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following is the best example of product differentiation?

A) A cookie manufacturer introduces a new variant of cookies for Halloween.

B) A firm that sells printers starts a new manufacturing unit to manufacture printer cartridges.

C) A firm that produces laptops introduces a new line of tablet personal computers.

D) A leading women's fashion house introduces a line of men's clothing.

E) A supermarket introduces a range of pre-packaged salads.

A) A cookie manufacturer introduces a new variant of cookies for Halloween.

B) A firm that sells printers starts a new manufacturing unit to manufacture printer cartridges.

C) A firm that produces laptops introduces a new line of tablet personal computers.

D) A leading women's fashion house introduces a line of men's clothing.

E) A supermarket introduces a range of pre-packaged salads.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

22

Many natural monopolies are regulated. Explain the rationale for such regulation.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

23

In the long run, the economic profit earned by a firm under monopolistic competition:

A) is positive because firms produce with excess capacity.

B) is zero because of price wars among a small number of firms.

C) is zero because of free entry and exit possibilities in the market.

D) is positive because of advertising and product differentiation by the firms.

E) is positive because of collusive behavior between firms.

A) is positive because firms produce with excess capacity.

B) is zero because of price wars among a small number of firms.

C) is zero because of free entry and exit possibilities in the market.

D) is positive because of advertising and product differentiation by the firms.

E) is positive because of collusive behavior between firms.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

24

How can the quality of a product serve as an entry barrier in a market?

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

25

In the long run, monopolistically competitive firms:

A) earn zero economic profit.

B) face perfectly elastic demand curves.

C) tend to standardize their products.

D) produce output at minimum marginal cost.

E) merge and form a few dominant firms to maximize profit.

A) earn zero economic profit.

B) face perfectly elastic demand curves.

C) tend to standardize their products.

D) produce output at minimum marginal cost.

E) merge and form a few dominant firms to maximize profit.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

26

Explain why monopolies are economically inefficient.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

27

In comparing monopolistic competition to perfect competition, the major difference lies in:

A) the number of firms in each industry.

B) the typical firm size in each industry.

C) the degree of entry barriers in each industry.

D) the demand curves faced by individual firms in each industry.

E) the long-run profits of firms in each industry.

A) the number of firms in each industry.

B) the typical firm size in each industry.

C) the degree of entry barriers in each industry.

D) the demand curves faced by individual firms in each industry.

E) the long-run profits of firms in each industry.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

28

Why do monopolistically competitive firms have a tendency to advertise much more than perfectly competitive firms?

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following, if true, would be an example of a monopolistically competitive industry?

A) In the utilities industry, average cost declines over all levels of output.

B) In the automobile industry, fixed costs as well as variable costs are high.

C) In the retail trade industry, a large number of firms provide similar products.

D) The market for basic office supplies (pencils, paper, and clips) is served by scores of online suppliers.

E) In the pharmaceuticals industry, the entire market is served by a small number of large firms.

A) In the utilities industry, average cost declines over all levels of output.

B) In the automobile industry, fixed costs as well as variable costs are high.

C) In the retail trade industry, a large number of firms provide similar products.

D) The market for basic office supplies (pencils, paper, and clips) is served by scores of online suppliers.

E) In the pharmaceuticals industry, the entire market is served by a small number of large firms.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

30

The demand curve faced by individual firms under monopolistic competition is:

A) perfectly elastic.

B) perfectly inelastic.

C) downward-sloping.

D) upward-sloping.

E) the same as the market demand curve.

A) perfectly elastic.

B) perfectly inelastic.

C) downward-sloping.

D) upward-sloping.

E) the same as the market demand curve.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

31

Why are substantial economies of scale considered a barrier to entry?

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

32

How useful is the Lerner index as a measure of monopoly power?

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

33

Carefully define and describe a natural monopoly.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

34

Unlike perfectly competitive markets, monopolistically competitive markets:

A) have significant barriers to entry.

B) face declining average costs at all levels of output.

C) have fewer firms.

D) produce differentiated products.

E) Answers face declining average costs at all levels of output and produce differentiated products are both correct.

A) have significant barriers to entry.

B) face declining average costs at all levels of output.

C) have fewer firms.

D) produce differentiated products.

E) Answers face declining average costs at all levels of output and produce differentiated products are both correct.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

35

A monopolist faces the demand curve P = 100 - 2Q, where P = price and Q is quantity demanded. If the monopolist has a total cost of C = 50 + 20Q, determine its profit-maximizing price and output.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

36

The profit margins for fast food firms like Wendy's have fallen because of an increase in competition from similar fast food chains and microwaveable food available in supermarkets. Based on this information, which of the following is true?

A) The elasticity of demand for Wendy's fast food is relatively inelastic.

B) Wendy's operates as a monopoly firm in the fast food market.

C) The fast food market is monopolistically competitive.

D) Wendy's fast food is an inferior good for most consumers.

E) There are strategic entry barriers in the fast-food market.

A) The elasticity of demand for Wendy's fast food is relatively inelastic.

B) Wendy's operates as a monopoly firm in the fast food market.

C) The fast food market is monopolistically competitive.

D) Wendy's fast food is an inferior good for most consumers.

E) There are strategic entry barriers in the fast-food market.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following is true in the long run under monopolistic competition?

A) P = MC.

B) P = AC.

C) P > AC > MC.

D) Price > AC = MC.

E) MR > MC.

A) P = MC.

B) P = AC.

C) P > AC > MC.

D) Price > AC = MC.

E) MR > MC.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

38

The demand curve for a monopolistically competitive firm slopes downward because:

A) the demand for the product drops to zero after a slight price increase.

B) competing firms produce differentiated products.

C) there is a very little brand loyalty towards a single firm's product.

D) customers are not influenced by advertising.

E) buyers are not sensitive to changes in the price of the product.

A) the demand for the product drops to zero after a slight price increase.

B) competing firms produce differentiated products.

C) there is a very little brand loyalty towards a single firm's product.

D) customers are not influenced by advertising.

E) buyers are not sensitive to changes in the price of the product.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

39

Unlike a pure monopoly firm, a monopolistically competitive firm:

A) makes a positive economic profit in the long-run.

B) faces downward sloping demand curve.

C) have no entry barriers to protect it from new entrants.

D) produces a standardized good or service.

E) produces at the level where marginal revenue equals marginal cost.

A) makes a positive economic profit in the long-run.

B) faces downward sloping demand curve.

C) have no entry barriers to protect it from new entrants.

D) produces a standardized good or service.

E) produces at the level where marginal revenue equals marginal cost.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

40

When competing firms or nations collude to form a cartel, the intention is to set one common price. This tendency to avoid competition should bring about stability. Paradoxically, however, cartels are usually unstable. Why?

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

41

Kiwi Inc. dominates the wholesale chicken market in New Zealand. Its production cost is: long-run average cost [LAC] = long-run marginal cost [LMC] = $2 per pound and demand is given by P = 6 - 2Q, where P denotes price per pound and Q denotes output (in millions of pounds).

(a) Determine Kiwi's output and price (presuming it faces no other competitors).

(a) Determine Kiwi's output and price (presuming it faces no other competitors).

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

42

The demand for a good produced by a firm has been reliably measured by P = 100 - 5Q, output Q is measured in thousands of units. If the total cost function is given by: C = 10Q, what is the optimal level of output produced by the monopolist?

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

43

In a perfectly competitive market, industry demand is: P = 850 - 2Q, and industry supply is: P = 250 + 4Q (Supply is the sum of the marginal cost curves of the firms in the industry).

(a) Determine price and output under perfect competition.

(a) Determine price and output under perfect competition.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

44

Carefully explain how short-run equilibrium and long-run equilibrium in monopolistic competition differ. Use graphs to illustrate your answer.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

45

Based on your understanding of monopolistic competition, list five examples of real firms that operate in monopolistically competitive markets.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

46

Compare and contrast a monopolistically competitive firm and a perfectly competitive firm.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

47

A monopolist faces the price equation: P = 1,000 - .5Q, and total cost: C = 50,000 + 100Q + .4Q2.

(a) Determine the price and output that maximize total revenue, and the level of profit.

(a) Determine the price and output that maximize total revenue, and the level of profit.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

48

Regulatory authorities tend to be concerned about barriers to entry. Why are barriers so important?

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

49

Under patent protection, a firm has a monopoly in the production of a high-tech component. Market demand is estimated to be P = 100 - .2Q. The firm's economic costs are given by AC = MC = $60 per component.

(a) Determine the firm's output and price.

(a) Determine the firm's output and price.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

50

Describe the different types of entry barriers and their importance to the study of monopoly.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

51

Most people believe that monopolies always have excessive profits, yet some unregulated monopolies might have very low earnings.

(a) Why might a monopoly have little or no economic value? Explain.

(a) Why might a monopoly have little or no economic value? Explain.

Unlock Deck

Unlock for access to all 51 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 51 flashcards in this deck.