Exam 11: Perfect Competition

Exam 1: What Is Economics205 Questions

Exam 2: The Economic Problem145 Questions

Exam 3: Demand and Supply188 Questions

Exam 4: Elasticity166 Questions

Exam 5: Efficiency and Equity123 Questions

Exam 6: Government Actions in Markets125 Questions

Exam 7: Global Markets in Action135 Questions

Exam 8: Utility and Demand116 Questions

Exam 9: Possibilities, preferences, and Choices120 Questions

Exam 10: Output and Costs145 Questions

Exam 11: Perfect Competition114 Questions

Exam 12: Monopoly114 Questions

Exam 13: Monopolistic Competition136 Questions

Exam 14: Oligopoly100 Questions

Exam 15: Externalities114 Questions

Exam 16: Public Goods and Common Resources96 Questions

Exam 17: Markets for Factors of Production122 Questions

Exam 18: Economic Inequality115 Questions

Select questions type

In which one of the following situations will a perfectly competitive firm make an economic profit?

Free

(Multiple Choice)

4.8/5  (42)

(42)

Correct Answer: Verified

Verified

B

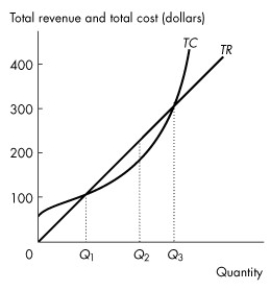

Use the figure below to answer the following question.  Figure 11.2.1

-Refer to Figure 11.2.1,which shows a perfectly competitive firm's total revenue and total cost curves.Which one of the following statements is false?

Figure 11.2.1

-Refer to Figure 11.2.1,which shows a perfectly competitive firm's total revenue and total cost curves.Which one of the following statements is false?

Free

(Multiple Choice)

4.8/5 (35)

Correct Answer:Verified

D

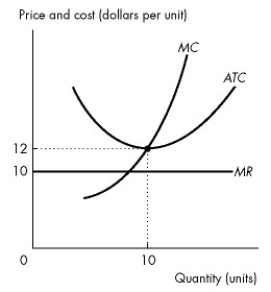

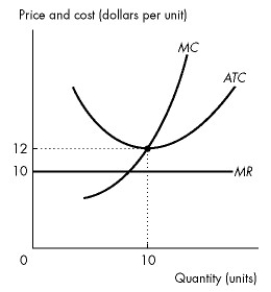

Use the figure below to answer the following questions.  Figure 11.3.1

-Refer to Figure 11.3.1,which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive industry.In the short run,if the market price of the good is $10,the firm produces ________ units of output and ________.

Figure 11.3.1

-Refer to Figure 11.3.1,which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive industry.In the short run,if the market price of the good is $10,the firm produces ________ units of output and ________.

Free

(Multiple Choice)

4.9/5 (41)

Correct Answer:Verified

E

Use the figure below to answer the following questions.  Figure 11.2.2

-Refer to Figure 11.2.2,which shows a perfectly competitive firm's economic profit and loss.The firm is breaking even at points

Figure 11.2.2

-Refer to Figure 11.2.2,which shows a perfectly competitive firm's economic profit and loss.The firm is breaking even at points

(Multiple Choice)

4.8/5 (35)

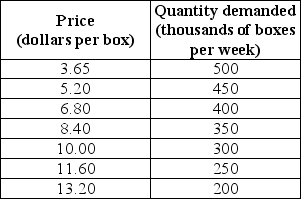

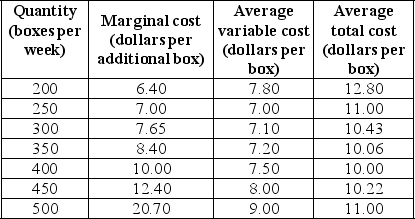

Use the table below to answer the following question.

Table 11.2.4

-Refer to Table 11.2.4.The market is perfectly competitive and there are 1,000 firms that produce paper. The top table sets out the market demand schedule for paper.

Each producer of paper has the costs shown in the bottom table when it uses its least-cost plant size.

The market price is ________ a box and the market output is ________ boxes.The output produced by each firm is ________ boxes.Each firm ________.

-Refer to Table 11.2.4.The market is perfectly competitive and there are 1,000 firms that produce paper. The top table sets out the market demand schedule for paper.

Each producer of paper has the costs shown in the bottom table when it uses its least-cost plant size.

The market price is ________ a box and the market output is ________ boxes.The output produced by each firm is ________ boxes.Each firm ________.

(Multiple Choice)

4.7/5 (39)

Assume that the leather market is a perfectly competitive market.The market demand curve for leather is ________ and each individual leather producer's demand curve is ________.

(Multiple Choice)

4.7/5 (35)

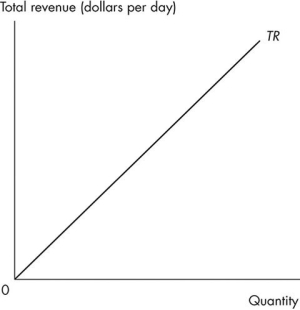

Use the figure below to answer the following questions.  Figure 11.1.1

-Refer to Figure 11.1.1.The firm competes in a perfectly competitive market.The total revenue curve is a straight line because the firm

Figure 11.1.1

-Refer to Figure 11.1.1.The firm competes in a perfectly competitive market.The total revenue curve is a straight line because the firm

(Multiple Choice)

4.9/5 (32)

A firm that temporarily shuts down and produces no output incurs a loss equal to its

(Multiple Choice)

4.8/5 (39)

Initially,a perfectly competitive market that has 1,000 firms is in long-run equilibrium.Then 100 firms in the industry adopt a new technology that reduces the average cost of producing the good.In the short run,the price ________,firms with the new technology make ________ economic profit,and firms with the old technology ________.

(Multiple Choice)

5.0/5 (36)

Which one of the following does not occur in perfect competition?

(Multiple Choice)

4.7/5 (30)

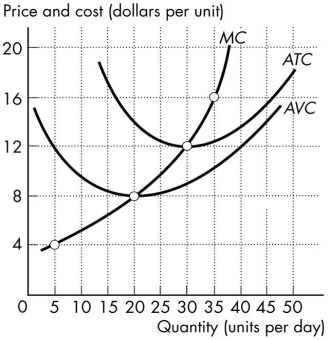

Use the figure below to answer the following question.  Figure 11.4.4

-Refer to Figure 11.4.4,which shows the cost curves for a perfectly competitive firm.If all firms in the market have the same cost curves and the price is $16 per unit,

Figure 11.4.4

-Refer to Figure 11.4.4,which shows the cost curves for a perfectly competitive firm.If all firms in the market have the same cost curves and the price is $16 per unit,

(Multiple Choice)

4.9/5 (33)

In a perfectly competitive market,a firm maximizes its profit by producing the quantity of output at which

(Multiple Choice)

4.7/5 (29)

If a profit-maximizing firm in a perfectly competitive market is making an economic profit,then it must be producing a level of output where

(Multiple Choice)

4.7/5 (38)

If price falls below minimum average variable cost,the best a firm can do is

(Multiple Choice)

4.9/5 (31)

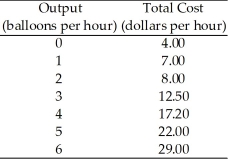

Use the table below to answer the following questions.

Table 11.2.3  -Refer to Table 11.2.3,which gives the total cost schedule for Brenda's Balloon Shop,a perfectly competitive firm.The marginal cost of increasing production from 4 balloons an hour to 5 balloons an hour is

-Refer to Table 11.2.3,which gives the total cost schedule for Brenda's Balloon Shop,a perfectly competitive firm.The marginal cost of increasing production from 4 balloons an hour to 5 balloons an hour is

(Multiple Choice)

4.8/5 (34)

Use the figure below to answer the following questions.  Figure 11.4.1

-Refer to Figure 11.4.1,which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive market.In the long run,

Figure 11.4.1

-Refer to Figure 11.4.1,which shows the cost curves and marginal revenue curve of a firm in a perfectly competitive market.In the long run,

(Multiple Choice)

4.7/5 (25)

Use the information below to answer the following questions.

Fact 11.4.1

Franklin is a fiddlehead farmer.He sold 10 bags of fiddleheads last month,with total fixed cost of $100 and total variable cost of $50.

-Refer to Fact 11.4.1.If the price of fiddleheads last month was $15 per bag,Franklin

(Multiple Choice)

4.8/5 (34)

In a perfectly competitive market,which of the following increases the price that the firms charge in the short run?

(Multiple Choice)

4.9/5 (37)

Use the table below to answer the following questions.

Table 11.2.3

-Refer to Table 11.2.3,which gives the total cost schedule for Brenda's Balloon Shop,a perfectly competitive firm.The average fixed cost of producing the 4th balloon is

(Multiple Choice)

4.9/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)