Exam 7: Foreign Currency Derivatives: Futures and Options

Exam 1: Multinational Financial Management: Opportunities and Challenges73 Questions

Exam 2: The International Monetary System61 Questions

Exam 3: The Balance of Payments83 Questions

Exam 4: Financial Goals and Corporate Governance69 Questions

Exam 5: The Foreign Exchange Market69 Questions

Exam 6: International Parity Conditions61 Questions

Exam 7: Foreign Currency Derivatives: Futures and Options88 Questions

Exam 8: Interest Risk and Swaps49 Questions

Exam 9: Foreign Exchange Rate Determination and Intervention63 Questions

Exam 10: Transaction Exposure64 Questions

Exam 11: Translation Exposure54 Questions

Exam 12: Operating Exposure58 Questions

Exam 13: Global Cost and Availability of Capital83 Questions

Exam 14: Funding the Multinational Firm94 Questions

Exam 15: Multinational Tax Management65 Questions

Exam 16: International Trade Finance75 Questions

Exam 17: Foreign Direct Investment and Political Risk55 Questions

Exam 18: Multinational Capital Budgeting and Cross-Border Acquisitions61 Questions

Select questions type

Which of the following is NOT true for the writer of a put option?

(Multiple Choice)

4.8/5  (45)

(45)

Traders who believe volatilities will fall significantly in the near-term will:

(Multiple Choice)

4.8/5 (40)

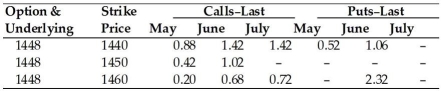

Use the table to answer following question(s).

April 19, 2009, British Pound Option Prices (cents per pound, 62,500 pound contracts).

-Refer to Table 7.1. The May call option on pounds with a strike price of 1440 means:

-Refer to Table 7.1. The May call option on pounds with a strike price of 1440 means:

(Multiple Choice)

4.7/5 (40)

Option values increase with the length of time to maturity. The expected change in the option premium from a small change in the time to expiration is termed delta.

(True/False)

4.9/5 (31)

A speculator in the futures market wishing to lock in a price at which they could ________ a foreign currency will ________ a futures contract.

(Multiple Choice)

4.9/5 (45)

A foreign currency ________ gives the purchaser the right, not the obligation, to buy a given amount of foreign exchange at a fixed price per unit for a specified period.

(Multiple Choice)

4.8/5 (30)

Option premiums deteriorate at a/an ________ as they approach expiration.

(Multiple Choice)

4.8/5 (44)

As a general statement, it is safe to say that businesses generally use the ________ for foreign currency option contracts, and individuals and financial institutions typically use the ________.

(Multiple Choice)

4.8/5 (29)

A put option on yen is written with a strike price of ¥105.00/$. Which spot price maximizes your profit if you choose to exercise the option before maturity?

(Multiple Choice)

4.9/5 (37)

The writer of the option is referred to as the seller, and the buyer of the option is referred to as the holder.

(True/False)

4.8/5 (41)

A foreign currency ________ option gives the holder the right to ________ a foreign currency, whereas a foreign currency ________ option gives the holder the right to ________ an option.

(Multiple Choice)

4.8/5 (51)

Which of the following is NOT true for the writer of a call option?

(Multiple Choice)

4.8/5 (38)

Which of the following is NOT a contract specification for currency futures trading on an organized exchange?

(Multiple Choice)

4.8/5 (34)

The price of an option is always somewhat greater than its intrinsic value, since there is always some chance that the intrinsic value will rise between the present and the expiration date.

(True/False)

4.9/5 (37)

Historical volatility is the correct method for the calculation of the option volatility.

(True/False)

4.8/5 (32)

A foreign currency ________ contract calls for the future delivery of a standard amount of foreign exchange at a fixed time, place, and price.

(Multiple Choice)

4.8/5 (41)

The time value is asymmetric in value as you move away from the strike price (i.e., the time value at two cents above the strike price is not necessarily the same as the time value two cents below the strike price).

(True/False)

4.9/5 (38)

Jasper Pernik is a currency speculator who enjoys "betting" on changes in the foreign currency exchange market. Currently the spot price for the Japanese yen is ¥129.87/$ and the 6-month forward rate is ¥128.53/$. Jasper thinks the yen will move to ¥128.00/$ in the next six months. If Jasper buys $100,000 worth of yen at today's spot price and sells within the next six months at ¥128/$, he will earn a profit of:

(Multiple Choice)

4.7/5 (40)

The expected change in the option premium from a small change in the domestic interest rate (home currency) is term rho.

(True/False)

5.0/5 (28)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)