Exam 4: Demand and Supply Applications

Exam 1: The Scope and Method of Economics238 Questions

Exam 2: The Economic Problem: Scarcity and Choice220 Questions

Exam 3: Demand, Supply, and Market Equilibrium298 Questions

Exam 4: Demand and Supply Applications173 Questions

Exam 5: Elasticity189 Questions

Exam 6: Household Behavior and Consumer Choice273 Questions

Exam 7: The Production Process: the Behavior of Profit-Maximizing Firms273 Questions

Exam 8: Short-Run Costs and Output Decisions387 Questions

Exam 9: Long-Run Costs and Output Decisions362 Questions

Exam 10: Input Demand: The Labor and Land Markets198 Questions

Exam 11: Input Demand: The Capital Market and the Investment Decision230 Questions

Exam 12: General Equilibrium and the Efficiency of Perfect Competition202 Questions

Exam 13: Monopoly and Antitrust Policy396 Questions

Exam 14: Oligopoly217 Questions

Exam 15: Monopolistic Competition235 Questions

Exam 16: Externalities, Public Goods, and Common Resources275 Questions

Exam 17: Uncertainty and Asymmetric Information132 Questions

Exam 18: Income Distribution and Poverty197 Questions

Exam 19: Public Finance: The Economics of Taxation281 Questions

Exam 20: Introduction to Macroeconomics241 Questions

Exam 21: Measuring National Output and National Income292 Questions

Exam 22: Unemployment, Inflation, and Long-Run Growth297 Questions

Exam 23: Aggregate Expenditure and Equilibrium Output355 Questions

Exam 24: The Government and Fiscal Policy360 Questions

Exam 25: Money, the Federal Reserve, and the Interest Rate357 Questions

Exam 26: The Determination of Aggregate Output, the Price Level, and the Interest Rate243 Questions

Exam 27: Policy Effects and Cost Shocks in the Asad Model200 Questions

Exam 28: The Labor Market in the Macroeconomy287 Questions

Exam 29: Financial Crises, Stabilization, and Deficits260 Questions

Exam 30: Household and Firm Behavior in the Macroeconomy: a Further Look364 Questions

Exam 31: Long-Run Growth196 Questions

Exam 32: Alternative Views in Macroeconomics294 Questions

Exam 33: International Trade, Comparative Advantage, and Protectionism289 Questions

Exam 34: Open-Economy Macroeconomics: the Balance of Payments and Exchange Rates308 Questions

Exam 35: Economic Growth in Developing Economies133 Questions

Exam 36: Critical Thinking About Research105 Questions

Select questions type

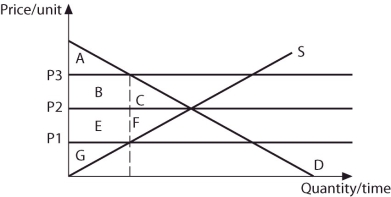

Refer to the information provided in Figure 4.6 below to answer the question(s) that follow.

Equilibrium in this market occurs at the intersection of curves S and D.  Figure 4.6

-Refer to Figure 4.6. If price is P1, consumer surplus is area

Figure 4.6

-Refer to Figure 4.6. If price is P1, consumer surplus is area

(Multiple Choice)

4.8/5  (32)

(32)

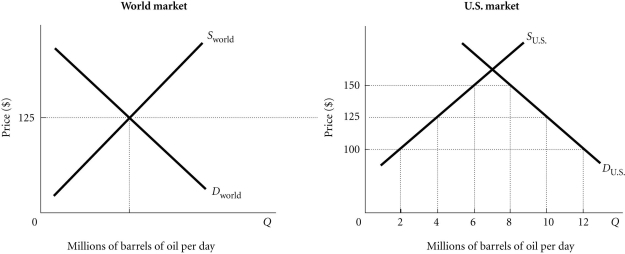

Refer to the information provided in Figure 4.4 below to answer the question(s) that follow.  Figure 4.4

-Refer to Figure 4.4. Assume that initially there is free trade. If the United States then imposes a $25 tax per barrel of imported oil

Figure 4.4

-Refer to Figure 4.4. Assume that initially there is free trade. If the United States then imposes a $25 tax per barrel of imported oil

(Multiple Choice)

4.9/5 (44)

If the most someone is willing to pay for an airline ticket to Las Vegas is $300 and the market price of the ticket is $200, then this buyer will get consumer surplus of

(Multiple Choice)

4.7/5 (29)

If the equilibrium price of gasoline is $3.00 per gallon and the government will not allow oil companies to charge more than $2.00 per gallon of gasoline, which of the following will happen?

(Multiple Choice)

4.9/5 (26)

Related to the Economics in Practice on page 77: If a hurricane results in the supply of hotel rooms decreasing and the equilibrium price for hotel rooms increases, the demand for hotel rooms ________ and total revenue from the sale of hotel rooms ________.

(Multiple Choice)

4.9/5 (32)

People scalping tickets for a jazz festival will be successful at selling the tickets for a profit

(Multiple Choice)

5.0/5 (47)

The government imposes a maximum price on apartments that is above the equilibrium price. You accurately predict that

(Multiple Choice)

4.8/5 (40)

In the short run, nonprice rationing will happen whenever there is excess demand in a market.

(True/False)

4.8/5 (39)

Related to the Economics in Practice on p. 81: The initial price of $0 for the Shakespeare in the Park tickets is akin to the city of New York ________ the tickets.

(Multiple Choice)

4.8/5 (37)

For a particular product, an effective price ceiling results in

(Multiple Choice)

4.8/5 (37)

The difference between current market price and full costs of production for the firm is known as

(Multiple Choice)

4.8/5 (39)

An example of an ineffective price ceiling would be the government setting the maximum price of wheat at ________ per bushel when the market price is at $5.00 per bushel.

(Multiple Choice)

4.8/5 (27)

In the short run, it is necessary to nonprice ration a good whenever ________ exists.

(Multiple Choice)

4.9/5 (38)

Refer to the information provided in Figure 4.6 below to answer the question(s) that follow.

Equilibrium in this market occurs at the intersection of curves S and D. Figure 4.6

-Refer to Figure 4.6. At equilibrium, consumer surplus is area

(Multiple Choice)

4.9/5 (34)

A U.S. import fee on steel would increase the domestic quantity of steel supplied.

(True/False)

4.8/5 (36)

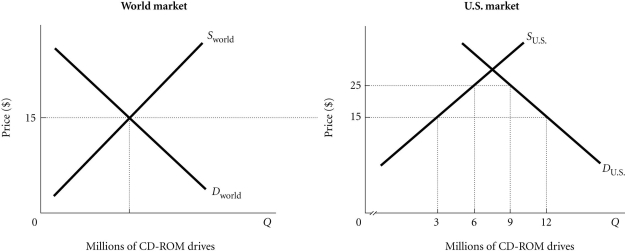

Refer to the information provided in Figure 4.5 below to answer the question(s) that follow.  Figure 4.5

-Refer to Figure 4.5. Assume that initially there is free trade. If the United States then imposes a $10.00 tax per CD-Rom drive on imported CD-Rom drives

Figure 4.5

-Refer to Figure 4.5. Assume that initially there is free trade. If the United States then imposes a $10.00 tax per CD-Rom drive on imported CD-Rom drives

(Multiple Choice)

4.7/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)