Exam 4: Demand and Supply Applications

Exam 1: The Scope and Method of Economics238 Questions

Exam 2: The Economic Problem: Scarcity and Choice220 Questions

Exam 3: Demand, Supply, and Market Equilibrium298 Questions

Exam 4: Demand and Supply Applications173 Questions

Exam 5: Elasticity189 Questions

Exam 6: Household Behavior and Consumer Choice273 Questions

Exam 7: The Production Process: the Behavior of Profit-Maximizing Firms273 Questions

Exam 8: Short-Run Costs and Output Decisions387 Questions

Exam 9: Long-Run Costs and Output Decisions362 Questions

Exam 10: Input Demand: The Labor and Land Markets198 Questions

Exam 11: Input Demand: The Capital Market and the Investment Decision230 Questions

Exam 12: General Equilibrium and the Efficiency of Perfect Competition202 Questions

Exam 13: Monopoly and Antitrust Policy396 Questions

Exam 14: Oligopoly217 Questions

Exam 15: Monopolistic Competition235 Questions

Exam 16: Externalities, Public Goods, and Common Resources275 Questions

Exam 17: Uncertainty and Asymmetric Information132 Questions

Exam 18: Income Distribution and Poverty197 Questions

Exam 19: Public Finance: The Economics of Taxation281 Questions

Exam 20: Introduction to Macroeconomics241 Questions

Exam 21: Measuring National Output and National Income292 Questions

Exam 22: Unemployment, Inflation, and Long-Run Growth297 Questions

Exam 23: Aggregate Expenditure and Equilibrium Output355 Questions

Exam 24: The Government and Fiscal Policy360 Questions

Exam 25: Money, the Federal Reserve, and the Interest Rate357 Questions

Exam 26: The Determination of Aggregate Output, the Price Level, and the Interest Rate243 Questions

Exam 27: Policy Effects and Cost Shocks in the Asad Model200 Questions

Exam 28: The Labor Market in the Macroeconomy287 Questions

Exam 29: Financial Crises, Stabilization, and Deficits260 Questions

Exam 30: Household and Firm Behavior in the Macroeconomy: a Further Look364 Questions

Exam 31: Long-Run Growth196 Questions

Exam 32: Alternative Views in Macroeconomics294 Questions

Exam 33: International Trade, Comparative Advantage, and Protectionism289 Questions

Exam 34: Open-Economy Macroeconomics: the Balance of Payments and Exchange Rates308 Questions

Exam 35: Economic Growth in Developing Economies133 Questions

Exam 36: Critical Thinking About Research105 Questions

Select questions type

A U.S. import fee on steel would increase the domestic quantity of steel demanded.

(True/False)

4.8/5  (44)

(44)

When supply is ________ or the product is ________, then price is demand determined.

(Multiple Choice)

4.7/5 (25)

In the short run, it is necessary to ________ a good whenever excess demand exists.

(Multiple Choice)

4.7/5 (27)

In a "black market," goods are traded at market determined prices.

(True/False)

4.8/5 (36)

Refer to the information provided in Figure 4.1 below to answer the question(s) that follow.  Figure 4.1

-Refer to Figure 4.1. The United States will import 6 million apples per day if a per-apple tax of ________ is levied on imported apples.

Figure 4.1

-Refer to Figure 4.1. The United States will import 6 million apples per day if a per-apple tax of ________ is levied on imported apples.

(Multiple Choice)

4.8/5 (37)

Refer to the information provided in Figure 4.6 below to answer the question(s) that follow.

Equilibrium in this market occurs at the intersection of curves S and D. ![Refer to the information provided in Figure 4.6 below to answer the question(s) that follow. Equilibrium in this market occurs at the intersection of curves S and D. Figure 4.6 -Refer to Figure 4.6. Consumer surplus changes by the area [E - C] if price goes from equilibrium to](https://storage.examlex.com/TB2924/11eab9ca_3e60_924e_b53a_cfc323460690_TB2924_00_TB2924_00_TB2924_00_TB2924_00_TB2924_00_TB2924_00_TB2924_00_TB2924_00_TB2924_00_TB2924_00_TB2924_00_TB2924_00_TB2924_00_TB2924_00.jpg) Figure 4.6

-Refer to Figure 4.6. Consumer surplus changes by the area [E - C] if price goes from equilibrium to

Figure 4.6

-Refer to Figure 4.6. Consumer surplus changes by the area [E - C] if price goes from equilibrium to

(Multiple Choice)

4.9/5 (38)

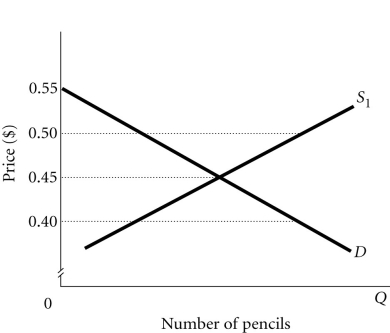

Refer to the information provided in Figure 4.3 below to answer the question(s) that follow.  Figure 4.3

-Refer to Figure 4.3. The government setting the price of pencils at $0.40 would be an example of an effective

Figure 4.3

-Refer to Figure 4.3. The government setting the price of pencils at $0.40 would be an example of an effective

(Multiple Choice)

4.8/5 (33)

Refer to the information provided in Figure 4.6 below to answer the question(s) that follow.

Equilibrium in this market occurs at the intersection of curves S and D. Figure 4.6

-Refer to Figure 4.6. If price goes from equilibrium to P1, consumer surplus changes by the area

(Multiple Choice)

4.9/5 (38)

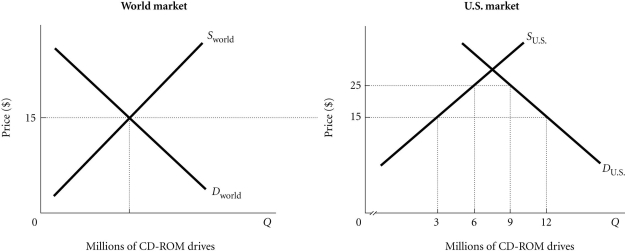

Refer to the information provided in Figure 4.5 below to answer the question(s) that follow.  Figure 4.5

-Refer to Figure 4.5. Assume that initially there is free trade. If the United States then imposes a $10.00 tax per CD-Rom drive on imported CD-Rom drives

Figure 4.5

-Refer to Figure 4.5. Assume that initially there is free trade. If the United States then imposes a $10.00 tax per CD-Rom drive on imported CD-Rom drives

(Multiple Choice)

4.8/5 (33)

Producer surplus describes a situation in which there is excess quantity demanded.

(True/False)

4.7/5 (29)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)