Exam 7: Reporting and Interpreting Cost of Goods Sold and Inventory

Exam 1: Financial Statements and Business Decisions122 Questions

Exam 2: Investing and Financing Decisions and the Accounting System132 Questions

Exam 3: Operating Decisions and the Accounting System114 Questions

Exam 4: Adjustments, Financial Statements, and the Quality of Earnings136 Questions

Exam 5: Communicating and Interpreting Accounting Information111 Questions

Exam 6: Reporting and Interpreting Sales Revenue, Receivables, and Cash128 Questions

Exam 7: Reporting and Interpreting Cost of Goods Sold and Inventory124 Questions

Exam 8: Reporting and Interpreting Property, Plant, and Equipment; Intangibles; and Natural Resources126 Questions

Exam 9: Reporting and Interpreting Liabilities113 Questions

Exam 10: Reporting and Interpreting Bonds120 Questions

Exam 11: Reporting and Interpreting Owners Equity118 Questions

Exam 12: Statement of Cash Flows116 Questions

Exam 13: Analyzing Financial Statements110 Questions

Exam 14: Reporting and Interpreting Investments in Other Corporations112 Questions

Select questions type

Compute the missing amounts that are numbered in parentheses for the income statement of each independent case. (Hint: Each case need not be calculated in the numerical order of the missing numbers.)

(Essay)

4.9/5  (38)

(38)

Atomic Company did not record a December 2013 purchase of inventory on credit until January 2014. Assuming that the December 31, 2013 ending inventory was correctly determined, what is the effect of this error on the financial statements for the year ended December 31, 2013?

(Multiple Choice)

4.7/5 (34)

Moore Company purchased an item for inventory that cost $20 per unit and was priced to sell at $30. It was determined that the replacement cost is $18 per unit. Using the lower of cost or market rule, what amount should be reported on the balance sheet for inventory?

(Multiple Choice)

4.9/5 (38)

During periods of increasing unit costs, the LIFO inventory method results in lower income taxes.

(True/False)

4.9/5 (37)

Rio Company uses the FIFO inventory costing method and has a perpetual inventory system. All purchases and sales were cash transactions. The records reflected the following for January, 2014: Units Unit Cost Beginning inventory 100 \ 1.00 Purchase, January 6 200 1.20 Sale, January 10 (at \ 2.40 per unit) 110 Purchase, January 14 100 1.30 Sale, January 29 (at \ 2.60 per unit) 170 Required:

Determine the following:

A. 2014 cost of goods available for sale

B. 2014 cost of goods sold

C. 2014 ending inventory

D. The journal entries for January 6 and 10

(Essay)

4.7/5 (40)

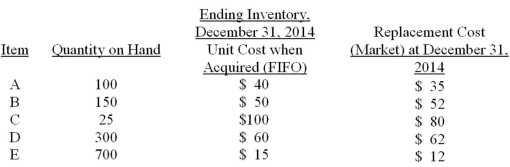

Boulder, Inc. is computing its inventory at December 31, 2014. The following information relates to the five major inventory items regularly stocked for resale.  Required:

Using the lower of cost or market rule, compute the total valuation for each inventory item at December 31, 2014, and the total inventory valuation.

Required:

Using the lower of cost or market rule, compute the total valuation for each inventory item at December 31, 2014, and the total inventory valuation.

(Essay)

4.9/5 (29)

The LIFO inventory method allocates the oldest inventory purchase costs to cost of goods sold.

(True/False)

4.7/5 (41)

The records of Jimmy Company show 2014 purchases of $90,000. An actual count revealed a 2014 ending inventory of $8,000. The 2014 beginning inventory was $5,000. What was cost of goods sold for 2014?

(Essay)

4.9/5 (44)

An overstatement of the 2013 ending inventory results in an understatement of net income during 2014.

(True/False)

4.8/5 (45)

Which of the following is correct when, in the same year, beginning inventory is understated by $1,300 and ending inventory is understated by $700?

(Multiple Choice)

4.9/5 (33)

During periods of decreasing unit costs, use of the FIFO inventory method results in lower gross profit than would use of the LIFO method.

(True/False)

4.9/5 (42)

Inventory turnover is calculated as cost of goods sold divided by average inventory.

(True/False)

4.8/5 (37)

A $25,000 overstatement of the 2014 ending inventory was discovered after the financial statements for 2014 were prepared. Which of the following describes the effect of the inventory error on the 2014 financial statements?

(Multiple Choice)

4.8/5 (36)

A company can use the LIFO inventory method for income tax purposes and the FIFO inventory method for financial reporting purposes during a given year.

(True/False)

4.8/5 (35)

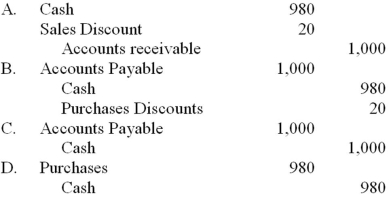

Carrie Company sold merchandise with an invoice price of $1,000 to Underwood, Inc., with terms of 2/10, n/30. Which of the following is the correct entry to record the payment by Underwood Inc., within the 10 days if the company uses the periodic inventory system and the gross method to record purchases?

(Multiple Choice)

4.9/5 (41)

A company reported the following information for its most recent year of operation: purchases, $100,000; beginning inventory, $20,000; and cost of goods sold, $110,000. How much was the company's ending inventory?

(Multiple Choice)

4.8/5 (44)

William Company uses the periodic inventory system and has provided the following data: Units Amount Beginning inventory 6,000 \ 30,000 Purchases 32,000 192,000 Sales 28,000 280,000 Required:

(Essay)

4.8/5 (38)

McMillan Company uses the periodic inventory system. It has compiled the following information in order to prepare the financial statements at December 31, 2014: Gross sales during 2014 \ 2,000,000 Sales returns and allowances during 2014 50,000 Beginning inventory, January 1,2014 100,000 Ending inventory, December 31, 2014 120,000 Purchases during 2014 750,000 Required:

Calculate each of the following:

A. Cost of goods available for sale

B. Cost of goods sold

C. Gross profit

(Essay)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)