Exam 23: Accounting for Changes and Errors

Exam 1: The Environment of Financial Reporting41 Questions

Exam 2: Financial Reporting: Its Conceptual Framework87 Questions

Exam 3: Review of a Companys Accounting System87 Questions

Exam 4: The Balance Sheet and the Statement of Changes in Stockholders Equity78 Questions

Exam 5: The Income Statement and the Statement of Cash Flows104 Questions

Exam 6: Additional Aspects of Financial Reporting and Financial Analysis95 Questions

Exam 7: Cash and Receivables99 Questions

Exam 8: Inventories: Cost Measurement and Flow Assumptions89 Questions

Exam 9: Inventories: Special Valuation Issues109 Questions

Exam 10: Property, Plant, and Equipment: Acquisition and Disposal88 Questions

Exam 11: Depreciation and Depletion103 Questions

Exam 12: Intangibles84 Questions

Exam 13: Current Liabilities and Contingencies99 Questions

Exam 14: Long-Term Liabilities and Receivables140 Questions

Exam 15: Investments101 Questions

Exam 16: Contributed Capital121 Questions

Exam 17: Earnings Per Share and Retained Earnings86 Questions

Exam 18: Income Recognition and Measurement of Net Assets71 Questions

Exam 19: Accounting for Income Taxes74 Questions

Exam 20: Accounting for Postemployment Benefits68 Questions

Exam 21: Accounting for Leases114 Questions

Exam 22: The Statement of Cash Flows62 Questions

Exam 23: Accounting for Changes and Errors86 Questions

Exam 24: Time Value of Money Module72 Questions

Select questions type

The Tricia Co.presented financial statements for 2010 and 2011 that contained the following errors: 2011 2010 Ending merchandise inventory \ 700 understated \ 400 overstated Supplies expense 500 understated 100 overstated Assuming that no correcting entries were made, by how much would retained earnings be understated at January 1, 2012?

Free

(Multiple Choice)

4.8/5  (37)

(37)

Correct Answer: Verified

Verified

B

A change in accounting principle from one that is not generally accepted to one that is generally accepted should be treated as

Free

(Multiple Choice)

4.9/5 (45)

Correct Answer:Verified

A

Shelley Construction began operations in 2010 and appropriately used the completed-contract method in accounting for its long-term construction contracts.Effective January 1, 2012, Shelley changed to the percentage-of-completion method for both financial and tax reporting and can justify the change.Although cumulative pretax income up to January 1, 2012, was $800, 000 using the completed-contract method, cumulative pretax income would have totaled $1, 100, 000 had the percentage-of-completion method been used.Assuming an income tax rate of 30%, Shelley's 2012 financial statements should report a marginal change in its January 1, 2012 balance in Retained Earnings to restate it for the effect of the accounting change in the amount of

Free

(Multiple Choice)

4.9/5 (37)

Correct Answer:Verified

C

Which of the following statements does not properly state a basic principle for reporting an accounting change?

(Multiple Choice)

4.9/5 (43)

During 2012, Kramer Company determined, based on new information, that equipment previously depreciated using a ten-year life and a salvage value of $100, 000 had a total estimated life of only six years and a salvage value of $50, 000.The equipment was acquired on January 1, 2010, and was depreciated using the straight-line method.Kramer made an accounting change in 2012 to reflect this additional information, and the change was approved by the IRS.Kramer has an income tax rate of 30%.Assuming Kramer's income before depreciation, before income taxes, and before any retroactive effect of the accounting change (if any)for the year ended December 31, 2012, was $180, 000, Kramer's net income for 2012 should be

(Multiple Choice)

4.9/5 (35)

An overstatement of reported net income for the current year may result from

(Multiple Choice)

4.7/5 (46)

Linda Company has been depreciating equipment for 10 years with an estimated total useful life of 25 years.Linda has revised the estimated life to be only 17 years, with 7 years remaining in the asset's useful life.Linda should

(Multiple Choice)

4.9/5 (28)

IFRS differ from U.S.GAAP regarding the indirect effects of a change in accounting principle in that IFRS

(Multiple Choice)

4.8/5 (37)

Several items related to accounting changes appear below.

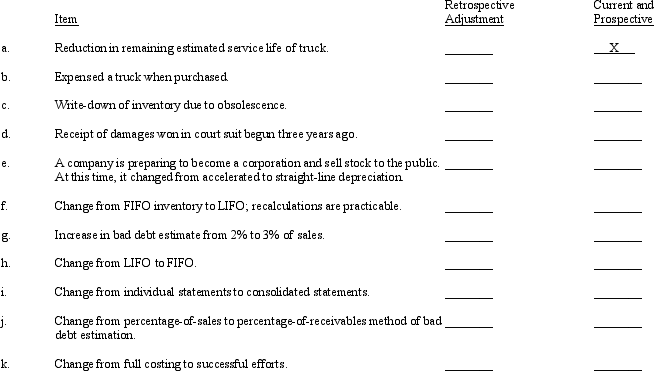

Required:

Indicate the appropriate method of accounting for each case by placing an "X" in the appropriate column.Part (a)has been completed as an example.

Required:

Indicate the appropriate method of accounting for each case by placing an "X" in the appropriate column.Part (a)has been completed as an example.

(Essay)

4.8/5 (33)

Match the diagrams with the concepts by writing the identifying letter of the diagram on the blank line to the left of the concept. "VAL" represents the value to be calculated.

Correct Answer:Verified

Premises:

Responses:

(Matching)

4.9/5 (40)

Lavonne Company purchased a machine on July 1, 2010, for $80, 000.The machine has an estimated useful life of 5 years with a salvage value of $10, 000.It is being depreciated using the straight-line method.On January 1, 2012, Lavonne reevaluated the machine's useful life and now believes it will continue for another 6 years (for a total of 7 1/2 years)and have no salvage value at the end of its useful life.Depreciation expense for the year ended December 31, 2012, related to this machine would be

(Multiple Choice)

4.8/5 (34)

On January 1, 2006, the Rita Company purchased for $80, 000 a building that was expected to have a 20-year useful life with no residual value at the end of its useful life.The straight-line method of depreciation was used.On January 1, 2012, Rita Company determined that the remaining life of the building was four years, and there was no change in residual value.What is the balance in Accumulated Depreciation: Building at December 31, 2012, assuming that Rita properly accounted for the change?

(Multiple Choice)

5.0/5 (42)

On January 1, 2010, Chester Company acquired machinery at a cost of $60, 000.This machinery was being depreciated by the double-declining-balance method over an estimated life of five years with no salvage value.At the beginning of 2012, Chester changed to and could justify straight-line depreciation.Chester's tax rate is 30 percent.The depreciation expense to be included in 2012 net income was

(Multiple Choice)

4.8/5 (37)

Which of the following changes would normally require some footnote disclosure?

(Multiple Choice)

4.9/5 (31)

Leigh Co.reported $7, 000 of net income for 2010.The following errors were then discovered: -Ending 2008 accrued expense was understated by

-Ending 2009 unearned revenue was overstated by .

-Ending 2008 unearned revenue was overstated by

Ignoring income taxes, compute correct 2010 net income.

(Multiple Choice)

4.7/5 (32)

Which of the following statements is not an example of a correction of an error in previously issued financial statements?

(Multiple Choice)

4.8/5 (35)

All of the following would be reported retrospectively by restating prior period's financial results except for a

(Multiple Choice)

4.9/5 (39)

On January 1, 2010, Jennifer Company purchased for $40, 000 a truck that had an estimated life of five years and no residual value at the end of its useful life.Jennifer uses straight-line depreciation.The cost of the truck was charged to Repairs Expense when purchased in 2010.

Required:

a. Ignoring income taxes, prepare the journal entry to correct the error if it was discovered and corrected on January 1,2013 (Jennifer's year ends on December 31).

b. When preparing the 2013 financial statements, how much depreciation expense should be reported on the comparative 2011 and 2012 income statements?

(Essay)

4.9/5 (44)

Disadvantages of using the retrospective application method do not include which of the following?

(Multiple Choice)

4.8/5 (28)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)