Exam 23: Accounting for Changes and Errors

Exam 1: The Environment of Financial Reporting41 Questions

Exam 2: Financial Reporting: Its Conceptual Framework87 Questions

Exam 3: Review of a Companys Accounting System87 Questions

Exam 4: The Balance Sheet and the Statement of Changes in Stockholders Equity78 Questions

Exam 5: The Income Statement and the Statement of Cash Flows104 Questions

Exam 6: Additional Aspects of Financial Reporting and Financial Analysis95 Questions

Exam 7: Cash and Receivables99 Questions

Exam 8: Inventories: Cost Measurement and Flow Assumptions89 Questions

Exam 9: Inventories: Special Valuation Issues109 Questions

Exam 10: Property, Plant, and Equipment: Acquisition and Disposal88 Questions

Exam 11: Depreciation and Depletion103 Questions

Exam 12: Intangibles84 Questions

Exam 13: Current Liabilities and Contingencies99 Questions

Exam 14: Long-Term Liabilities and Receivables140 Questions

Exam 15: Investments101 Questions

Exam 16: Contributed Capital121 Questions

Exam 17: Earnings Per Share and Retained Earnings86 Questions

Exam 18: Income Recognition and Measurement of Net Assets71 Questions

Exam 19: Accounting for Income Taxes74 Questions

Exam 20: Accounting for Postemployment Benefits68 Questions

Exam 21: Accounting for Leases114 Questions

Exam 22: The Statement of Cash Flows62 Questions

Exam 23: Accounting for Changes and Errors86 Questions

Exam 24: Time Value of Money Module72 Questions

Select questions type

Myrna Company overstated the beginning inventory on January 1, 2010, by $20, 000.No other errors were identified.If the error is not discovered, which of the following net income effects related to the inventory error are true? Net Income 2009 2010 2011 I. understated overstated correct II. overstated understated correct III. correct understated overstated IV. overstated understated overstated

(Multiple Choice)

4.9/5  (42)

(42)

On January 1, 2010, Patti Company purchased a machine for $140, 000.Patti depreciated the machine over ten years with a $40, 000 salvage value.On January 1, 2014, Patti determined that the total useful life of the machine should be eight years with a salvage value of $18, 000.What is the depreciation expense on the machine for 2014?

(Multiple Choice)

4.9/5 (37)

Wendy Co.made the following errors in 2010: -Ending inventory was overstated by .

-Beginning inventory was understated by

-Purchaseswere overstated by .

Reported net income was $15, 000.The correct 2010 net income was

(Multiple Choice)

4.8/5 (34)

The mandatory adoption of a new accounting principle as a result of a new FASB statement requires

(Multiple Choice)

4.8/5 (37)

The 2010 and 2011 financial statements for Teresa Company had the following errors:

Teresa Company had reported net income of $90, 000 in 2010 and $95, 000 in 2011.

Required:

Prepare a schedule to determine the correct net income for 2010 and 2011.Begin the schedule with reported net income for 2010 and 2011 and work to a corrected figure.Ignore income taxes.

Teresa Company had reported net income of $90, 000 in 2010 and $95, 000 in 2011.

Required:

Prepare a schedule to determine the correct net income for 2010 and 2011.Begin the schedule with reported net income for 2010 and 2011 and work to a corrected figure.Ignore income taxes.

(Essay)

4.8/5 (35)

Laura Company received merchandise on December 31, 2010.Laura failed to record the purchase on account because the invoice was inadvertently destroyed.The merchandise was, however, included in ending inventory.The effect of this event on the financial statements as of December 31, 2010, would be

(Multiple Choice)

4.8/5 (42)

Exhibit 23-1 On January 1, 2010, the Carol Company purchased a machine for $450, 000 with an estimate useful life of six years and a $30, 000 salvage value.Straight-line depreciation was used for financial reporting purposes and MACRS depreciation for income tax reporting.Effective January 1, 2012, Carol switched to the double-declining-balance depreciation method for financial statement reporting but not for income tax purposes.Carol can justify the change.

-

Refer to Exhibit 23-1.Assuming an income tax rate of 30%, the cumulative effect change reported in Carol's 2012 income statement would be

(Multiple Choice)

4.8/5 (41)

Exhibit 23-5 Nan Company, having a fiscal year ending on December 31, discovered the following errors in 2010:

A collection of from a customer for rent related to January, 2011 , was recorded as revenue in 2010

Depreciation was under state d by in 2010.

The January 1, 2009, invento1y was overstated by .

The January 1,2010, inventory was understated by

Insurance premiums of that relate to 2011 were expensed in 2010 when paid.

-Assume no other errors have occurred and ignore income taxes.

Refer to Exhibit 23-5.Net income for 2010 was

(Multiple Choice)

4.8/5 (25)

Generally accepted methods of accounting for a change in accounting principle include

(Multiple Choice)

4.8/5 (37)

Changes in accounting entities that require retrospective restatement of past financial statements occur when

(Multiple Choice)

4.8/5 (36)

The correct 2010 net income for Margie Company, after error corrections, was $56, 000.Two errors were found after net income was first reported.The January 1, 2010 inventory and the December 31, 2010, inventory were overstated by $4, 000 and $9, 000, respectively.The net income that must have been originally reported was

(Multiple Choice)

4.8/5 (34)

Exhibit 23-2 On January 1, 2010, Michelle, Inc.purchased a machine for $48, 000.Eight-year, straight-line depreciation with no salvage value was used through December 31, 2013.On January 1, 2014, it was estimated that the total useful life of the machine from acquisition date was ten years.

-

Refer to Exhibit 23-2.Accordingly, the appropriate accounting change was made in 2014.How much depreciation expense for this machine should Michelle record for the year ended December 31, 2014?

(Multiple Choice)

4.8/5 (36)

Current GAAP requires a company to account for a change in accounting estimate that impacts multiple periods during

(Multiple Choice)

4.9/5 (33)

Exhibit 23-3 Kathy Company acquired a truck on January 1, 2010, for $140, 000.The truck had an estimated useful life of five years with no salvage value.Kathy used straight-line depreciation for the truck.On January 1, 2011, Kathy revises the estimated useful life of the truck.Kathy made the accounting change in 2011 to reflect the extended useful life.

-

Refer to Exhibit 23-3.If the revised estimated useful life of the truck is a total of seven years, and assuming an income tax rate of 30%, Kathy should report in its 2011 income statement an effect on prior years of changing the useful life of the truck of

(Multiple Choice)

4.8/5 (44)

Most errors are discovered automatically through proper use of the double-entry system or by the internal or external auditors.However, some errors escape detection until after they have been included in the published financial statements of a company.

Required:

Describe three types of errors that occur in financial statements and indicate the appropriate corrective action to take when the errors are discovered.

(Essay)

4.7/5 (37)

The Brown Company changed its method of determining inventories from LIFO to FIFO.This change represents a

(Multiple Choice)

4.9/5 (36)

Belinda Corp.reported $80, 000 of net income for 2010.The following errors were then discovered: -Ending 2010 accrued expense was overstated by

-2010 eame drevenue was overstated by .

-Ending 2010 prepaid expense was overstated by .

Ignoring income taxes, the correct 2010 net income is

(Multiple Choice)

4.7/5 (30)

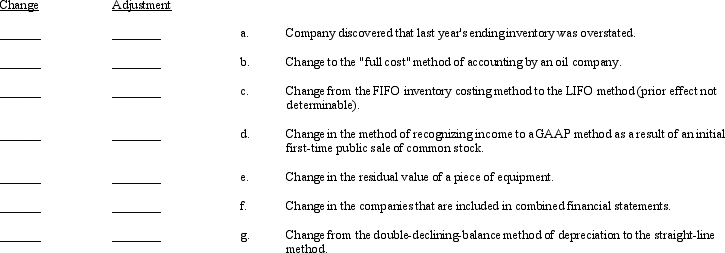

Generally accepted accounting principles have identified four types of accounting changes and two possible methods to use in accounting for these changes, as follows:

Required:

Following is a list of errors and changes.In the spaces provided, use the appropriate symbols selected from the above lists to indicate the type of change and how the change should be treated in the financial statements.

Required:

Following is a list of errors and changes.In the spaces provided, use the appropriate symbols selected from the above lists to indicate the type of change and how the change should be treated in the financial statements.

(Essay)

4.8/5 (28)

Iris Company decided to change from LIFO to FIFO inventory costing, effective January 1, 2012.The following data were available:

Excess of FIFO Ending Inventory Pretax Operating Over LIFO Year Income using LIFO Ending Inventory 2012 \ 40,000 \ 8,000 2011 20,000 7,000 2010 30,000 4,000 The income tax rate is 40%.The company began operations on January 1, 2010, and has paid no dividends since inception.

Required:

Answer the following questions relating to the 2011-2012 comparative financial statements.

a. What is net income for 2012 ?

b. What is restated net income for 2011?

c. Prepare the 2011 statement of reteined earnings as it would appear in the comprative 2011-2012 financial statements

(Essay)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)