Exam 6: The Risk and Term Structure of Interest Rates

Exam 1: Why Study Money, Banking, and Financial Markets114 Questions

Exam 2: An Overview of the Financial System113 Questions

Exam 3: What Is Money110 Questions

Exam 4: The Meaning of Interest Rates109 Questions

Exam 5: The Behaviour of Interest Rates113 Questions

Exam 6: The Risk and Term Structure of Interest Rates110 Questions

Exam 7: The Stock Market, the Theory of Rational Expectations, and the Efficient Market Hypothesis93 Questions

Exam 8: An Economic Analysis of Financial Structure110 Questions

Exam 9: Economic Analysis of Financial Regulation101 Questions

Exam 10: Banking Industry: Structure and Competition112 Questions

Exam 11: Financial Crises100 Questions

Exam 12: Banking and the Management of Financial Institutions139 Questions

Exam 13: Risk Management With Financial Derivatives96 Questions

Exam 14: Central Banks and the Bank of Canada110 Questions

Exam 15: The Money Supply Process164 Questions

Exam 16: Tools of Monetary Policy110 Questions

Exam 17: The Conduct of Monetary Policy: Strategy and Tactics116 Questions

Exam 18: The Foreign Exchange Market131 Questions

Exam 19: The International Financial System140 Questions

Exam 20: Quantity Theory, Inflation, and the Demand for Money109 Questions

Exam 21: The Is Curve139 Questions

Exam 22: The Monetary Policy and Aggregate Demand Curves108 Questions

Exam 23: Aggregate Demand and Supply Analysis120 Questions

Exam 24: Monetary Policy Theory92 Questions

Exam 25: The Role of Expectations in Monetary Policy110 Questions

Exam 26: Transmission Mechanisms of Monetary Policy108 Questions

Select questions type

Over the next three years, the expected path of 1-year interest rates is 4, 1, and 1 percent. The expectations theory of the term structure predicts that the current interest rate on 3-year bond is ________.

(Multiple Choice)

5.0/5  (40)

(40)

Explain using a diagram how the "flight to quality" after the Subprime collapse lead to a rising spread between lower-quality (BBB-rated) and highest-quality (AAA-rated) bonds.

(Essay)

4.9/5 (32)

Explain the factors that determine the risk structure of interest rates. Explain how a change of each factor changes interest rates.

(Essay)

5.0/5 (43)

Which of the following bonds are considered to be default-risk free?

(Multiple Choice)

4.7/5 (39)

A bond with default risk will always have a ________ risk premium and an increase in its default risk will ________ the risk premium.

(Multiple Choice)

4.8/5 (29)

The risk that interest payments will not be made, or that the face value of a bond is not repaid when a bond matures is ________.

(Multiple Choice)

4.9/5 (41)

An increase in the riskiness of corporate bonds will ________ the yield on corporate bonds and ________ the yield on government securities, everything else held constant.

(Multiple Choice)

4.7/5 (31)

According to the segmented markets theory of the term structure ________.

(Multiple Choice)

4.9/5 (29)

The risk premium on corporate bonds reflects the fact that corporate bonds have a higher default risk and are ________ Canada bonds.

(Multiple Choice)

4.7/5 (40)

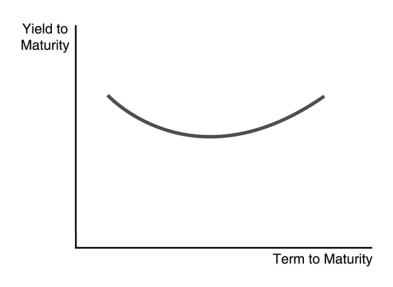

-The U-shaped yield curve in the figure above indicates that short-term interest rates are expected to ________.

-The U-shaped yield curve in the figure above indicates that short-term interest rates are expected to ________.

(Multiple Choice)

4.9/5 (44)

If the probability of a bond default increases because corporations begin to suffer large losses, then the default risk on corporate bonds will ________ and the expected return on these bonds will ________, everything else held constant.

(Multiple Choice)

4.9/5 (32)

According to the liquidity premium theory, a yield curve that is flat means that ________.

(Multiple Choice)

4.9/5 (42)

If the U.S. government where to raise the income tax rates, would this have any impact on a state's cost of borrowing funds? Explain.

(Essay)

4.8/5 (44)

According to the segmented markets theory of the term structure ________.

(Multiple Choice)

4.8/5 (43)

If a higher inflation is expected, what would you expect to happen to the shape of the yield curve? Why?

(Essay)

4.9/5 (32)

According to the liquidity premium theory of the term structure ________.

(Multiple Choice)

4.8/5 (36)

The spread between the interest rates on Baa corporate bonds and Canada bonds was very large during the Great Depression years 1930-1933. Explain this difference using the bond supply and demand analysis.

(Essay)

4.9/5 (47)

The collapse of the subprime mortgage market increased the spread between Baa and default-free Canada bonds. This is due to ________.

(Multiple Choice)

4.9/5 (41)

If 1-year interest rates for the next three years are expected to be 4, 2, and 3 percent, and the 3-year term premium is 1 percent, than the 3-year bond rate will be ________.

(Multiple Choice)

4.9/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)