Exam 10: Investments in Noncurrent Operating Assets-Acquisition

Exam 1: Financial Reporting86 Questions

Exam 2: A Review of the Accounting Cycle94 Questions

Exam 3: The Balance Sheet and Notes to the Financial Statements72 Questions

Exam 4: The Income Statement82 Questions

Exam 5: Statement of Cash Flows and Articulation79 Questions

Exam 6: Earnings Management46 Questions

Exam 7: The Revenuereceivablescash Cycle81 Questions

Exam 8: Revenue Recognition74 Questions

Exam 9: Inventory and Cost of Goods Sold121 Questions

Exam 10: Investments in Noncurrent Operating Assets-Acquisition88 Questions

Exam 11: Investments in Noncurrent Operating Assets-Utilization and Retirement84 Questions

Exam 12: Debt Financing103 Questions

Exam 13: Equity Financing88 Questions

Exam 14: Investments in Debt and Equity Securities81 Questions

Exam 15: Leases80 Questions

Exam 16: Income Taxes77 Questions

Exam 17: Employee Compensation-Payroll, Pensions, Other Comp Issues78 Questions

Exam 18: Earnings Per Share78 Questions

Exam 19: Derivatives, Contingencies, Business Segments, and Interim Reports79 Questions

Exam 20: Accounting Changes and Error Corrections74 Questions

Exam 21: Statement of Cash Flows Revisited61 Questions

Exam 22: Accounting in a Global Market60 Questions

Exam 23: Analysis of Financial Statements57 Questions

Select questions type

A company is constructing an asset for its own use. Construction began in 2010. The asset is being financed entirely with a specific new borrowing. Construction expenditures were made in 2010 and 2011 at the end of each quarter. The total amount of interest cost capitalized in 2011 should be determined by applying the interest rate on the specific new borrowing to the

Free

(Multiple Choice)

4.8/5  (44)

(44)

Correct Answer: Verified

Verified

B

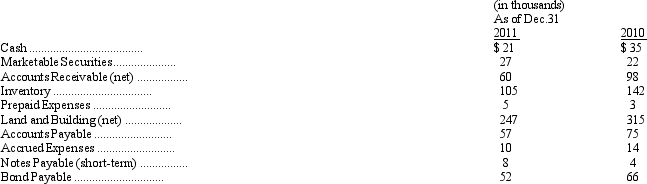

Selected information from the 2011 and 2010 financial statements of Bowen Corporation is presented below.

Bowen had cash sales of $750 and credit sales of $615 during 2011. Cost of goods sold for 2011 was $819. Bowen's fixed asset turnover for 2011 is

Bowen had cash sales of $750 and credit sales of $615 during 2011. Cost of goods sold for 2011 was $819. Bowen's fixed asset turnover for 2011 is

Free

(Multiple Choice)

4.8/5 (44)

Correct Answer:Verified

B

A trademark is an example of which general category of intangible asset that should be recognized separately according to current generally accepted accounting principles?

Free

(Multiple Choice)

4.9/5 (46)

Correct Answer:Verified

A

Nimbus Inc. purchased certain plant assets under a deferred payment contract. The agreement was to pay $30,000 per year for ten years. The plant assets should be valued at

(Multiple Choice)

4.9/5 (39)

The 2011 annual report of Bessemer Steel disclosed the following information relating to the company's construction projects, debt, and interest cost (in thousands of dollars):

Required:

Based on the information provided in the annual report, estimate the amount of interest to be capitalized in 2011. Give reasons why your estimate differs from the amount reported by the company. Assume that the construction payments were made uniformly during the year.

Required:

Based on the information provided in the annual report, estimate the amount of interest to be capitalized in 2011. Give reasons why your estimate differs from the amount reported by the company. Assume that the construction payments were made uniformly during the year.

(Essay)

4.8/5 (32)

In a business combination, goodwill is defined as the excess of cost over the

(Multiple Choice)

4.9/5 (39)

On October 1, Takei, Inc. exchanged 8,000 shares of its $25 par value common stock for a parcel of land to be held for a future plant site. Takei's common stock had a fair market value of $80 per share on the exchange date. Takei received $36,000 from the sale of scrap when an existing building on the site was razed. The land should be carried at

(Multiple Choice)

4.8/5 (38)

On February 12, Laker Company purchased a tract of land as a factory site for $175,000. An existing building on the property was razed and construction was begun on a new factory building in March of the same year. Additional data are available as follows:

The recorded cost of the completed factory building should be

The recorded cost of the completed factory building should be

(Multiple Choice)

4.9/5 (27)

Jazz Company acquired land and paid for it in full by issuing $600,000 of its 10 percent bonds payable and 40,000 shares of its common stock, par $10. The stock was selling at $19 per share and the bonds were trading at 102. What amount should Jazz record as the cost of the land?

(Multiple Choice)

4.8/5 (41)

On March 1, 2011, the Sefkwak Company paid $400,000 for all the issued and outstanding stock of Bodo Corporation in a transaction properly accounted for as a purchase. The market values of the assets and liabilities of Bodo Corporation on March 1, 2011, are as follows:

Make the journal entry necessary for Sefkwak to record the purchase.

Make the journal entry necessary for Sefkwak to record the purchase.

(Essay)

4.8/5 (35)

During 2011, Grant Industries, Inc. constructed a new manufacturing facility at a cost of $12,000,000. The weighted average accumulated expenditures for 2011 were calculated to be $5,400,000. The company had the following debt outstanding at December 31, 2011:

Determine the amount of interest to be capitalized by Grant Industries for 2011.

Determine the amount of interest to be capitalized by Grant Industries for 2011.

(Essay)

4.9/5 (37)

Jazz company started construction on a building on January 1 of this year and completed construction on December 31 of the same year. Jazz had only two interest notes outstanding during the year, and both of these notes were outstanding for all 12 months of the year. The following information is available:

What amount of interest should Jazz capitalize for the current year?

What amount of interest should Jazz capitalize for the current year?

(Multiple Choice)

4.8/5 (47)

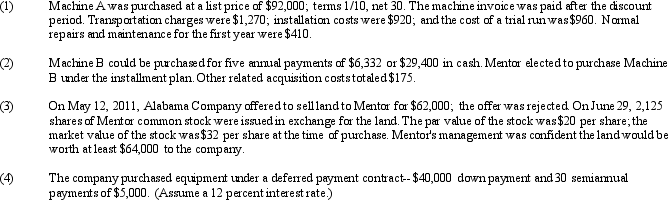

One of the most critical steps in recording the acquisition of assets is the determination of the cost assigned to the asset. Data related to assets acquired by Mentor Manufacturing Company are as follows:

Determine the acquisition cost for each of the assets.

Determine the acquisition cost for each of the assets.

(Essay)

4.7/5 (38)

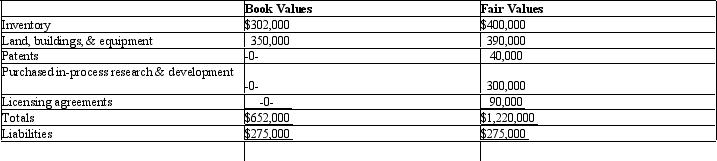

RGW Industries purchased the net assets of SP Company for $1,300,000, comprised of $1,200,000 of cash and a contingent performance condition of $100,000. A schedule of the net assets of SP Company, as recorded on SP Company's books at the time of the acquisition, is as follows:

Assets Cash \ 31,000 Receivables 250,000 Inventory 302,000 Land, buildings, and equipment(net) Total assets \ 933,000

The following schedule shows the differences between the recorded costs and market values of the assets of SP Company at the date of the acquisition:

The following schedule shows the differences between the recorded costs and market values of the assets of SP Company at the date of the acquisition:

Prepare the journal entry to record this acquisition using the acquisition method prescribed by SFAS 141R,, "Business Combinations."

Prepare the journal entry to record this acquisition using the acquisition method prescribed by SFAS 141R,, "Business Combinations."

(Essay)

4.7/5 (34)

The general ledger of the Flayle Corporation as of December 31 includes the following accounts:

In the preparation of Flayle's balance sheet as of December 31, what should be reported as total intangible assets?

In the preparation of Flayle's balance sheet as of December 31, what should be reported as total intangible assets?

(Multiple Choice)

4.8/5 (35)

On September 10, Sandy Company incurred the following costs for one of its printing presses:

Neither the attachment nor the renovation increased the estimated useful life of the press. However, the renovation resulted in significantly increased productivity. What amount of the costs should be capitalized?

Neither the attachment nor the renovation increased the estimated useful life of the press. However, the renovation resulted in significantly increased productivity. What amount of the costs should be capitalized?

(Multiple Choice)

4.8/5 (35)

On April 30, 2011, Sistar, Inc. purchased for $30 per share all 200,000 of Wren Corp.'s outstanding common stock. On this date Wren's balance sheet showed net assets of $5,000,000. Additionally, the fair value of Wren's identifiable assets on this date was $400,000 in excess of their carrying amount. On Sistar's April 30, 2011, consolidated balance sheet, what amount should be reported as goodwill?

(Multiple Choice)

4.9/5 (35)

The third year of a construction project began with a $30,000 balance in Construction in Progress. Included in that figure is $6,000 of interest capitalized in the first two years. Construction expenditures during the third year were $80,000 which were incurred evenly throughout the entire year. The company has had over $300,000 in interest-bearing debt outstanding the third year, at a weighted average rate of 9 percent. How much interest for the third year is capitalized?

(Multiple Choice)

4.7/5 (43)

Western Company entered into a contract with Snape Construction Company to construct a building. Construction began in 2011 and was completed in 2012. As of January 1, 2012, Western had made total progress payments to Snape of $50,000. In addition, interest capitalized on the building during 2011 was $2,500. Western made additional payments on June 30, 2012, and December 31, 2012. Western had issued $80,000 of 9% bonds to finance part of the construction. The average interest on Western's additional debt was 11% for 2012.

How much interest should be capitalized by Western for 2012?

(Multiple Choice)

4.8/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)