Exam 11: Optimal Portfolio Choice and the Capital Asset Pricing Model

Exam 1: The Corporation38 Questions

Exam 2: Introduction to Financial Statement Analysis103 Questions

Exam 3: Financial Decision Making and the Law of One Price89 Questions

Exam 4: The Time Value of Money91 Questions

Exam 5: Interest Rates68 Questions

Exam 6: Valuing Bonds115 Questions

Exam 7: Investment Decision Rules86 Questions

Exam 8: Fundamentals of Capital Budgeting95 Questions

Exam 9: Valuing Stocks96 Questions

Exam 10: Capital Markets and the Pricing of Risk103 Questions

Exam 11: Optimal Portfolio Choice and the Capital Asset Pricing Model134 Questions

Exam 12: Estimating the Cost of Capital104 Questions

Exam 13: Investor Behavior and Capital Market Efficiency77 Questions

Exam 14: Capital Structure in a Perfect Market99 Questions

Exam 15: Debt and Taxes97 Questions

Exam 16: Financial Distress,managerial Incentives,and Information111 Questions

Exam 17: Payout Policy96 Questions

Exam 18: Capital Budgeting and Valuation With Leverage99 Questions

Exam 19: Valuation and Financial Modeling: a Case Study49 Questions

Exam 20: Financial Options57 Questions

Exam 21: Option Valuation42 Questions

Exam 22: Real Options64 Questions

Exam 23: Raising Equity Capital51 Questions

Exam 24: Debt Financing54 Questions

Exam 25: Leasing46 Questions

Exam 26: Working Capital Management47 Questions

Exam 27: Short-Term Financial Planning47 Questions

Exam 28: Mergers and Acquisitions59 Questions

Exam 29: Corporate Governance46 Questions

Exam 30: Risk Management53 Questions

Exam 31: International Corporate Finance48 Questions

Select questions type

Use the following information to answer the question(s)below.  The volatility of the market portfolio is 10%,the expected return on the market is 12%,and the risk-free rate of interest is 4%.

-The Sharpe Ratio for Rearden Metal is closest to:

The volatility of the market portfolio is 10%,the expected return on the market is 12%,and the risk-free rate of interest is 4%.

-The Sharpe Ratio for Rearden Metal is closest to:

(Multiple Choice)

4.9/5  (34)

(34)

Use the information for the question(s)below.

Suppose that the risk-free rate is 5% and the market portfolio has an expected return of 13% with a volatility of 18%.Monsters Inc.has a 24% volatility and a correlation with the market of .60,while California Gold Mining has a 32% volatility and a correlation with the market of -.7.Assume the CAPM assumptions hold.

-Monsters' required return is closest to:

(Multiple Choice)

5.0/5 (42)

Use the following information to answer the question(s)below. The volatility of the market portfolio is 10%,the expected return on the market is 12%,and the risk-free rate of interest is 4%.

-The beta for Wyatt Oil is closest to:

(Multiple Choice)

4.9/5 (38)

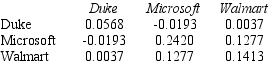

Use the table for the question(s)below.

Consider the following covariances between securities:  -What is the variance on a portfolio that has $3000 invested in Duke Energy,$4000 invested in Microsoft,and $3000 invested in Walmart stock?

-What is the variance on a portfolio that has $3000 invested in Duke Energy,$4000 invested in Microsoft,and $3000 invested in Walmart stock?

(Essay)

4.8/5 (40)

Use the information for the question(s)below.

Suppose you invest $20,000 by purchasing 200 shares of Abbott Labs (ABT)at $50 per share,200 shares of Lowes Companies,Inc.(LOW)at $30 per share,and 100 shares of Ball Corporation (BLL)at $40 per share.

-The weight on Ball Corporation in your portfolio is:

(Multiple Choice)

4.9/5 (34)

Explain how having different interest rates for borrowing and lending affect the CAPM and the SML.

(Essay)

4.8/5 (39)

Use the table for the question(s)below.

Consider the following returns:  -The covariance between Stock X's and Stock Y's returns is closest to:

-The covariance between Stock X's and Stock Y's returns is closest to:

(Multiple Choice)

4.9/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)