Exam 16: Non-Slg Not-For-Profit Organizations

Exam 1: Governmental and Nonprofit Accountingenvironment and Characteristics29 Questions

Exam 2: State and Local Government Accounting and Financial Reporting Modelthe Foundation66 Questions

Exam 3: Budgeting, Budgetary Accounting, and Budgetary Reporting36 Questions

Exam 4: The General Fund and Special Revenue Funds71 Questions

Exam 5: Revenue Accountinggovernmental Funds50 Questions

Exam 6: Expenditure Accountinggovernmental Funds65 Questions

Exam 7: Capital Projects Funds54 Questions

Exam 8: Debt Service Funds47 Questions

Exam 9: General Capital Assets; General Long-Term Liabilities; Permanent Fundsintroduction to Interfund-Gca-Gltl Accounting50 Questions

Exam 10: Enterprise Funds48 Questions

Exam 11: Internal Service Funds40 Questions

Exam 12: Trust and Agency Fiduciary Funds Summary of Interfund-Gca-Gltl Accounting41 Questions

Exam 13: Financial Reportingthe Basic Financial Statements and Required Supplementary Information58 Questions

Exam 14: Financial Reporting Deriving Government-Wide Financial Statements and Required Reconciliations48 Questions

Exam 15: Financial Reportingthe Comprehensive Annual Financial Report and the Financial Reporting Entity48 Questions

Exam 16: Non-Slg Not-For-Profit Organizations40 Questions

Exam 17: Accounting for Colleges and Universities41 Questions

Exam 18: Accounting for Health Care Entities34 Questions

Exam 19: Federal Government Accounting34 Questions

Exam 20: Auditing Governments and Not-For-Profit Organizations45 Questions

Select questions type

Computer equipment used in the business office of a not-for-profit organization was sold for $9,000. The original cost of the equipment had been $21,000 and there was $15,000 of accumulated depreciation as of the date of sale. How will the gain be reported?

Free

(Multiple Choice)

4.9/5  (32)

(32)

Correct Answer: Verified

Verified

B

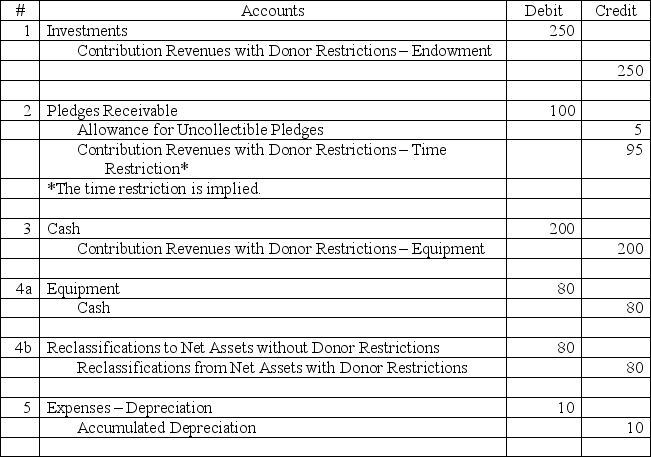

The following selected transactions occurred for a nongovernment, not-for-profit organization. All amounts are in thousands of dollars.

1. Received a contribution of stock to establish an endowment fund. The income from the endowment is unrestricted. The donor had acquired the stock for $23 about 20 years earlier. Its estimated fair value when donated was $250.

2. Pledges receivable at year end were $100, all from pledges received during the year. The pledges are unrestricted and 5% of the pledges are estimated to be uncollectible. The pledges expect to be collected early next year.

For questions 3-5, assume that the organization has adopted a policy that restrictions on donations made for capital purposes are met when the capital item is purchased.

3. A cash gift of $200 was received restricted for the purchase of equipment.

4. Equipment of $80 was purchased from the gift restricted for this purpose.

5. Depreciation expense for the year on the equipment purchased is $10.

Prepare the journal entries for the above transactions.

Free

(Essay)

4.8/5 (38)

Correct Answer:Verified

Investment earnings of $1,250 were earned on restricted investments. The earnings are to be used for various research projects during the current year. The earnings would be reported as

Free

(Multiple Choice)

4.7/5 (42)

Correct Answer:Verified

B

Special fund-raising events of a nongovernment, not-for-profit organization

(Multiple Choice)

4.8/5 (33)

Nongovernment not-for-profit organizations recognize revenues when

(Multiple Choice)

4.8/5 (37)

The line item, net assets released from restrictions, may be reported in a nongovernment, not-for-profit organization's statement of activities in which classifications?

(Multiple Choice)

4.9/5 (36)

A nongovernment not-for-profit organization received a cash donation restricted for construction of a new building. How should the donation be reported be reported in the statement of cash flows?

(Multiple Choice)

4.8/5 (37)

A not-for-profit organization receives donated supplies valued at $40,000 in June. As of the fiscal year end December, 31, 20X3, the organization had used 25% of the materials. The organization should report

(Multiple Choice)

4.8/5 (41)

A nongovernment not-for-profit organization received a cash donation of $100,000 restricted for a specific operating purpose. Only $20,000 of expenses related to the specific operating purpose was incurred during the current year. How should this activity be reported be in the statement of activities?

(Multiple Choice)

4.9/5 (32)

A nongovernment, not-for-profit organization provides the following information and asks you to determine how much revenue should be reported in each of its changes in net assets categories. All pledges are unconditional Cash contributions restricted to specific proprarns \ 200,000 Cash contributions restricted to endownent \ 1,000,000 Net realizable value of pledges to a buildirg prograrn resulting fron current year furdd raising efforts \4 50,000 Net realizable value of unconditional pledges resulting from curtent year fund raising efforts \1 50,000

Net Assets Net Assets without With Donor Restrictions Donor Restrictio A. \ 0 \ 1,755,000 B. \ 0 \ 755,000 C. \ 105,000 \ 1,650,000 D. \ 305,000 \ 1,450,000

(Short Answer)

4.7/5 (40)

The following selected transactions occurred for a nongovernmental, not-for-profit organization. All amounts are in thousands of dollars.

1. Unrestricted cash contributions received during the year, $300.

2. Restricted cash contributions were received during the year for the following: (a) Education programs, $43; (b) Building fund, $202; and (c) Endowment, $1,000.

3. Pledges received during the year were as follows: Unrestricted, $3,000; (b) Building fund, $5,000; and (c) Endowment, $20,000. 10% of pledges receivable typically prove uncollectible. Pledges expect to be collected early in the next year.

4. A benefit concert was held to raise resources for the building fund. Receipts totaled $1,400 and direct costs incurred totaled $850.

5. Salary expenses incurred for the education programs were paid, $14.

6. Materials were purchased on account for the education programs, $25.

7. Fees paid to an architect for design of the building during the year were $92. Additionally, payments to the building contractor during the year were $110.

8. Earnings on endowment fund investments are restricted to the entity's education programs. The earnings for the year were $13.

9. Cost of materials used for education programs during the year, $32

10. Earnings on building fund investments were not restricted by donors but the board requires that they be used to finance the building. The earnings on those investments for the year were $25.

Prepare the journal entries for the above transactions.

(Essay)

4.7/5 (30)

With respect to collections, nongovernment not-for-profit organizations are

(Multiple Choice)

4.8/5 (40)

Which of the following financial statements is not required for all nongovernment not-for-profit organizations?

(Multiple Choice)

4.9/5 (45)

A nongovernment not-for-profit organization received a cash donation of $100,000 restricted for a specific operating purpose. Only $20,000 of the donation was spent during the current year. How should the donation be reported be in the statement of activities?

(Multiple Choice)

4.8/5 (44)

A nongovernment voluntary health and welfare organization received unrestricted cash donations of $23,000 for the current year, $30,000 of pledges to be received in and used for general purposes in the following year, and a $100,000 donation to establish a permanent investment endowment. The organization should report

(Multiple Choice)

4.8/5 (36)

In 20X8, the following pledges were made: $35,000 in unrestricted contributions for use in 20X8; $20,000 in contributions restricted for use in 20X9; and a $400,000 contribution restricted for the establishment of a permanent endowment. It is anticipated that 10% of all pledges except the endowment pledge will be uncollectible. Pledges receivable for 20X8 should be

(Multiple Choice)

4.7/5 (34)

A nongovernment, not-for-profit organization received $5,000,000 of unconditional pledges during 2013 that had not been collected by year end. In its 2013 statement of activities, the organization should recognize

(Multiple Choice)

4.9/5 (31)

A private school is given $40,000 to permanently endow one of its education programs. A debit of $40,000 should be made to

(Multiple Choice)

4.8/5 (42)

Land valued at $100,000 was donated to a not-for-profit organization. The donation came with no restrictions. The organization's management decided to hold the land for resale and use the proceeds to establish a reserve for future capital needs. Which of the following journal entries would be made on the date of donation? Debit Credit A. Land Held for Resale \1 00,000 Contribution Revenues with Donor Restrictions \1 00,000 B. Land Held for Resale \1 00,000 Capital Contributions \1 00,000 C. Land Held for Resale \1 00,000 Contribution Revenues with Donor Restrictions \1 00,000 D. Land Held for Resale \1 00,000 Contribution Revenues with Donor Restrictions \1 00,000

(Short Answer)

5.0/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)