Exam 8: Debt Service Funds

Exam 1: Governmental and Nonprofit Accountingenvironment and Characteristics29 Questions

Exam 2: State and Local Government Accounting and Financial Reporting Modelthe Foundation66 Questions

Exam 3: Budgeting, Budgetary Accounting, and Budgetary Reporting36 Questions

Exam 4: The General Fund and Special Revenue Funds71 Questions

Exam 5: Revenue Accountinggovernmental Funds50 Questions

Exam 6: Expenditure Accountinggovernmental Funds65 Questions

Exam 7: Capital Projects Funds54 Questions

Exam 8: Debt Service Funds47 Questions

Exam 9: General Capital Assets; General Long-Term Liabilities; Permanent Fundsintroduction to Interfund-Gca-Gltl Accounting50 Questions

Exam 10: Enterprise Funds48 Questions

Exam 11: Internal Service Funds40 Questions

Exam 12: Trust and Agency Fiduciary Funds Summary of Interfund-Gca-Gltl Accounting41 Questions

Exam 13: Financial Reportingthe Basic Financial Statements and Required Supplementary Information58 Questions

Exam 14: Financial Reporting Deriving Government-Wide Financial Statements and Required Reconciliations48 Questions

Exam 15: Financial Reportingthe Comprehensive Annual Financial Report and the Financial Reporting Entity48 Questions

Exam 16: Non-Slg Not-For-Profit Organizations40 Questions

Exam 17: Accounting for Colleges and Universities41 Questions

Exam 18: Accounting for Health Care Entities34 Questions

Exam 19: Federal Government Accounting34 Questions

Exam 20: Auditing Governments and Not-For-Profit Organizations45 Questions

Select questions type

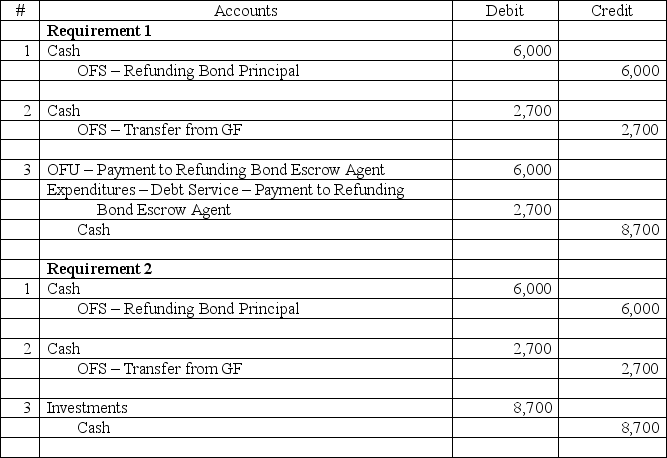

The City of Armona has decided to refinance $8,000 par value of general government, general obligation bonds outstanding. The bonds had a related unamortized bond premium of $200. The city issues $6,000 of refunding bonds and transfers $2,700 from the General Fund to the Debt Service Fund. The city paid $8,700 from the Debt Service Fund into an irrevocable trust to cover future payments on the original bonds. All amounts are in thousands of dollars.

1. Record the above transactions in the Debt Service Fund assuming the refinancing meets the conditions for treatment as a defeasance in substance.

2. Record the above transactions in the Debt Service Fund assuming the refinancing does not meet the conditions for treatment as a defeasance in substance.

3. For both requirements (1) and (2), indicate the effects of each transaction on the accounting equation of the Debt Service Fund and on the General Capital Assets and General Long-Term Liabilities accounts. If an element is not affected, put "NE" in the appropriate box.

Free

(Essay)

4.8/5  (28)

(28)

Correct Answer: Verified

Verified

Refunding

Investment (non-Refunding)

*Investments increase and cash decreases by equal amounts.

A government has $3,000,000 of 6%, 10-year general obligation bonds outstanding. The bonds were issued on July 2, 20X7 to finance construction of a general capital asset. Interest is payable semiannually on January 1 and July 1. What is the maximum amount of interest expenditures that the government would be permitted to report on the bonds for the year ended December 31, 20X7?

Free

(Multiple Choice)

4.7/5 (36)

Correct Answer:Verified

C

Debt Service Fund expenditures reported on the Statement of Revenues, Expenditures, and Changes in Fund Balance commonly exclude

Free

(Multiple Choice)

4.9/5 (37)

Correct Answer:Verified

D

A government paid $6,000,000 into an irrevocable trust to be used to service $5,000,000 of outstanding general obligation bonds, but the transaction does not meet the defeasance in-substance criteria. The payment included $3,000,000 of proceeds from a new bond issue that was issued to provide resources for the old bond. The other $3,000,000 had been accumulated over previous years from taxes and interest earnings in the Debt Service Fund. The government should report this transaction in its Debt Service Fund as

(Multiple Choice)

4.8/5 (42)

A government has $1,000,000 of 6%, 10-year general obligation bonds outstanding. The bonds were issued on August 15, 20X6 to finance construction of a general capital asset. Interest is payable semiannually on February 15 and August 15. What is the maximum amount of interest expenditures that the government would be permitted to report on the bonds for the year ended December 31, 20X6?

(Multiple Choice)

4.8/5 (40)

A Debt Service Fund received an annual payment from the General Fund to finance upcoming debt service payments. The amount received from the General Fund should be reported in the Debt Service Fund statement of revenues, expenditures, and changes in fund balance as

(Multiple Choice)

4.8/5 (32)

All of the following statements regarding a Debt Service Fund are true except

(Multiple Choice)

4.8/5 (41)

If General Fund cash is transferred to a Debt Service Fund to provide resources to refund outstanding debt, the Debt Service Fund statement of revenues, expenditures, and changes in fund balance would report

(Multiple Choice)

4.8/5 (43)

Debt Service Fund expenditures would include all of the following except

(Multiple Choice)

4.9/5 (44)

If a special tax is levied to finance debt service for a particular debt issue, the entry to record the levy in the Debt Service Fund would include

(Multiple Choice)

4.9/5 (42)

Debt service expenditures on general long-term debt principal should be recognized in the period that the liability:

(Multiple Choice)

5.0/5 (39)

Which of the following is not usually a requirement of a Debt Service Fund (DSF) for a term bond issue?

(Multiple Choice)

4.9/5 (41)

Assume that a county with a June 30 fiscal year end levied $900,000 in special assessments to finance debt service on a special assessment debt issuance. The levy date was January 20X1. The levy is to be paid by the property owners over a 10-year period beginning in January 20X2. The amount of revenue recognized by the county in the Debt Service Fund as of June 30, 20X1 would be

(Multiple Choice)

4.9/5 (33)

Assume that the fair market value of investments in a Debt Service Fund decreased by $25,000 as of the end of the fiscal year. What entry would be necessary to reflect this change?

(Multiple Choice)

4.9/5 (44)

Which of the following financial statements is not presented for a Debt Service Fund?

(Multiple Choice)

4.9/5 (33)

A government retired $5,000,000 of outstanding general obligation bonds when due. The government used $3,000,000 of proceeds from new bonds issued to provide resources for retiring the old bonds. The other $2,000,000 had been accumulated from tax and interest revenues over the years that the old bonds were outstanding. The government should report this transaction in its Debt Service Fund as

(Multiple Choice)

4.8/5 (36)

The GASB Codification sets forth circumstances in which a state or local government is permitted to accrue expenditures related to unmatured principal and interest on general obligation long-term liabilities. Which of the following are those circumstances?

I. Dedicated financial resources to pay the maturing principal and interest have been accumulated in a Debt Service Fund by year end.

II. The debt service payment is due early next year (within 30 days).

III. The debt service payment is due early next year (within 60 days).

(Multiple Choice)

4.9/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)