Exam 11: Partnerships: Distributions, Transfer of Interests, and Terminations

Exam 1: Understanding and Working With the Federal Tax Law71 Questions

Exam 2: Corporations: Introduction and Operating Rules94 Questions

Exam 3: Corporations: Special Situations99 Questions

Exam 4: Corporations: Organization and Capital Structure84 Questions

Exam 5: Corporations: Earnings Profits and Dividend Distributions114 Questions

Exam 6: Corporations: Redemptions and Liquidations88 Questions

Exam 7: Corporations: Reorganizations86 Questions

Exam 8: Consolidated Tax Returns138 Questions

Exam 9: Taxation of International Transactions163 Questions

Exam 10: Partnerships: Formation, Operation, and Basis122 Questions

Exam 11: Partnerships: Distributions, Transfer of Interests, and Terminations128 Questions

Exam 12: S Corporations135 Questions

Exam 13: Comparative Forms of Doing Business108 Questions

Exam 14: Taxes on the Financial Statements55 Questions

Exam 15: Exempt Entities100 Questions

Exam 16: Multistate Corporate Taxation123 Questions

Exam 17: Tax Practice and Ethics129 Questions

Exam 18: The Federal Gift and Estate Taxes188 Questions

Exam 19: Family Tax Planning145 Questions

Exam 20: Income Taxation of Trusts and Estates136 Questions

Select questions type

Match the following independent distribution payments in liquidation of a partner's interest in an ongoing partnership with the statements below

-Distribution of cash of $100,000, representing the partner's share of the value of partnership equipment which has potential depreciation recapture of $25,000.

(Multiple Choice)

4.8/5  (45)

(45)

Beth sells her 25% partnership interest to Katie for $50,000 cash on July 1 of the current tax year. Katie also assumed Beth's share of the partnership's liabilities. Beth's basis in her partnership interest at the beginning of the year was $40,000, including a $15,000 share of partnership liabilities. The partnership's income for the entire year was $100,000, and Beth's share of partnership debt was $10,000 as of the date she sold the partnership interest. Assume the partnership has no hot assets and that its income is earned evenly throughout the year. Beth recognizes a gain of $12,500 on the sale.

(True/False)

4.9/5 (37)

Match the following statements with the best match from the choices below. Note: Choice L may be used more than once

-Liquidating distribution

(Multiple Choice)

4.7/5 (36)

Match the following statements with the best match from the choices below. Note: Choice L may be used more than once

-Nonliquidating distribution

(Multiple Choice)

4.8/5 (39)

Match the following statements with the best match from the choices below. Note: Choice N may be used more than once

-General partner

(Multiple Choice)

4.9/5 (30)

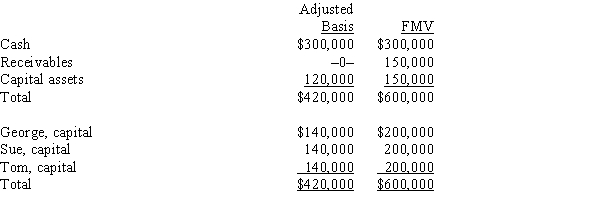

The December 31, 2014, balance sheet of GST Services, LLP reads as follows:  The partners share equally in partnership capital, income, gain, loss, deduction, and credit. Capital is not a material income-producing factor to the partnership, and all partners are active in the business. On December 31, 2014, general partner Sue receives a distribution of $200,000 cash in liquidation of her partnership interest under § 736. Sue's outside basis for the partnership interest immediately before the distribution is $150,000. (Her basis does not correspond to her capital account because she purchased the interest a few years ago at a $10,000 premium.) How much is Sue's gain or loss on the distribution and what is its character?

The partners share equally in partnership capital, income, gain, loss, deduction, and credit. Capital is not a material income-producing factor to the partnership, and all partners are active in the business. On December 31, 2014, general partner Sue receives a distribution of $200,000 cash in liquidation of her partnership interest under § 736. Sue's outside basis for the partnership interest immediately before the distribution is $150,000. (Her basis does not correspond to her capital account because she purchased the interest a few years ago at a $10,000 premium.) How much is Sue's gain or loss on the distribution and what is its character?

(Multiple Choice)

4.8/5 (38)

Match the following statements with the best match from the choices below. Note: Choice N may be used more than once

-Limited partner

(Multiple Choice)

4.9/5 (33)

Cindy, a 20% general partner in the CDE Partnership, wants to retire and has approached the other partners about having the partnership buy her out. The partnership is a cash basis, service oriented partnership in which Cindy is an active partner. The partnership's assets consist primarily of unrealized receivables and cash. The partnership also has substantial going concern value (goodwill) which is probably its most valuable asset. The other partners in the partnership are also active in the business and are not related to Cindy.

Discuss from Cindy's viewpoint how you would structure the liquidation of her interest under § 736. Answer as if you are her advocate. Do you think the other partners will agree with this structure? If not, what structure would they prefer?

(Essay)

4.8/5 (42)

Melissa is a partner in a continuing partnership. At the end of the current year, the partnership makes a proportionate, nonliquidating distribution to Melissa of $50,000 cash, inventory (basis of $22,000, fair market value of $20,000), and land (basis of $30,000, fair market value of $60,000). Melissa's basis in the partnership interest was $90,000 before the distribution. What is Melissa's basis in the inventory, land, and partnership interest following the distribution?

(Essay)

4.8/5 (33)

Match the following independent distribution payments in liquidation of a partner's interest in an ongoing partnership with the statements below

-Distribution of cash of $60,000 for a partner's share of unrealized receivables where the partner is a limited partner, and most of the partnership's income is derived from services.

(Multiple Choice)

4.8/5 (36)

Tom, Tina, Tatum, and Terry are equal owners in the 4-Ts LLC, a cash basis service entity. 4-Ts has unrealized receivables of $400,000 (basis of $0), and no other hot assets. A goodwill payment of $50,000 per partner is provided for in the LLC's operating agreement. If 4-Ts distributes cash of $300,000 to Tom in liquidation of his LLC interest, which of the following statements is correct?

(Multiple Choice)

4.9/5 (36)

Bob received a proportionate nonliquidating distribution of land from the BZ Partnership. The land had a fair market value of $15,000 and a basis to the partnership of $10,000. The land was held for investment purposes by the partnership. Bob's basis in his partnership interest immediately before the distribution was $6,000. If the partnership has a § 754 election in effect, it will record a $4,000 step-down in the basis of remaining assets, and the step-down will be attributed to all partners in the partnership.

(True/False)

4.7/5 (37)

Match the following statements with the best match from the choices below. Note: Choice L may be used more than once

-Nonqualified distribution

(Multiple Choice)

4.8/5 (29)

On December 31 of last year, Maria gave her daughter, Chelsea, a gift of a 25% interest in a partnership in which capital is a material income-producing factor. For the current calendar year, the partnership's ordinary income was $100,000. Maria and Chelsea were the only partners, and there were no guaranteed payments. Maria's services performed for the partnership were worth $60,000, and Chelsea has never performed any services. What is Maria's distributive share of partnership income for the current year?

(Multiple Choice)

4.9/5 (38)

Match the following statements with the best match from the choices below. Note: Choice L may be used more than once

-Ordering rules

(Multiple Choice)

4.8/5 (35)

Scott owns a 30% interest in the capital and profits of the SOS Partnership. Immediately before he receives a proportionate nonliquidating distribution from SOS, the basis of his partnership interest is $40,000. The distribution consists of $30,000 in cash and land with a fair market value of $80,000. SOS's adjusted basis in the land immediately before the distribution is $50,000. As a result of the distribution, Scott recognizes no gain or loss and his basis in the land is $10,000.

(True/False)

4.9/5 (33)

Julie is an active owner of a 52% interest in the JIR LLP, a consulting company (service provider). Her basis in the partnership interest is $100,000, and her share of the partnership's inside basis in assets is $120,000. Julie can sell her interest in the LLP on the first day of the tax year to Irene and Rachel (the other partners) for $100,000 each ($200,000 total). Alternatively, the LLP can distribute $200,000 of cash to redeem Julie's interest.

Assume the following: $10,000 of the redemption payment would be for the LLP's goodwill (which is not provided for in the partnership agreement); Julie's share of JIR's unrealized receivables is $40,000; and JIR has a § 754 election in effect. What are the advantages and disadvantages of the sale versus the redemption from Julie's and JIR's perspective? What is your recommendation? Explain.

(Essay)

4.7/5 (35)

Match the following statements with the best match from the choices below. Note: Choice N may be used more than once

-Service providing partnership

(Multiple Choice)

4.8/5 (31)

Match the following statements with the best match from the choices below. Note: Choice N may be used more than once

-Capital intensive partnership

(Multiple Choice)

4.8/5 (36)

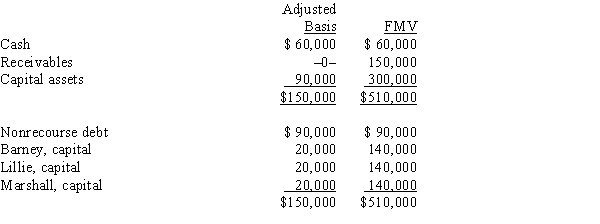

The BLM LLC's balance sheet on August 31 of the current year is as follows.  The nonrecourse debt is shared equally among the LLC members. On that date, Lillie sells her one-third interest to Robyn for $170,000, including cash and relief of Lillie's share of the nonrecourse debt. Lillie's outside basis for her interest in the LLC is $50,000, including her share of the LLC's debt. How much capital gain and/or ordinary income will Lillie recognize on the sale?

The nonrecourse debt is shared equally among the LLC members. On that date, Lillie sells her one-third interest to Robyn for $170,000, including cash and relief of Lillie's share of the nonrecourse debt. Lillie's outside basis for her interest in the LLC is $50,000, including her share of the LLC's debt. How much capital gain and/or ordinary income will Lillie recognize on the sale?

(Multiple Choice)

4.7/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)