Exam 5: Elasticity and Its Application

Exam 1: Ten Principles of Economics387 Questions

Exam 2: Thinking Like an Economist569 Questions

Exam 3: Interdependence and the Gains From Trade463 Questions

Exam 4: The Market Forces of Supply and Demand606 Questions

Exam 5: Elasticity and Its Application524 Questions

Exam 6: Supply,demand,and Government Policies593 Questions

Exam 7: Consumers,producers,and the Efficiency of Markets496 Questions

Exam 8: Application: The Costs of Taxation453 Questions

Exam 9: Application: International Trade441 Questions

Exam 10: Externalities473 Questions

Exam 11: Public Goods and Common Resources388 Questions

Exam 12: The Design of the Tax System499 Questions

Exam 13: The Costs of Production507 Questions

Exam 14: Firms in Competitive Markets502 Questions

Exam 15: Monopoly541 Questions

Exam 16: Monopolistic Competition521 Questions

Exam 17: Oligopoly428 Questions

Exam 18: The Market for the Factors of Production477 Questions

Exam 19: Earnings and Discrimination425 Questions

Exam 20: Income Inequality and Poverty399 Questions

Exam 21: The Theory of Consumer Choice492 Questions

Exam 22: Frontiers of Microeconomics380 Questions

Exam 23: Measuring a Nations Income464 Questions

Exam 24: Measuring the Cost of Living452 Questions

Exam 25: Production and Growth457 Questions

Exam 26: Saving,investment,and the Financial System502 Questions

Exam 27: The Basic Tools of Finance461 Questions

Exam 28: Unemployment610 Questions

Exam 29: The Monetary System461 Questions

Exam 30: Money Growth and Inflation427 Questions

Exam 31: Open-Economy Macroeconomic Models488 Questions

Exam 32: A Macroeconomic Theory of the Open Economy404 Questions

Exam 33: Aggregate Demand and Aggregate Supply511 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand451 Questions

Exam 35: The Short-Run Trade-Off Between Inflation and Unemployment415 Questions

Exam 36: Six Debates Over Macroeconomic Policy273 Questions

Select questions type

Supply is said to be inelastic if the quantity supplied responds substantially to changes in the price and elastic if the quantity supplied responds only slightly to price.

(True/False)

5.0/5  (27)

(27)

If the cross-price elasticity of demand for two goods is negative,then the two goods are substitutes.

(True/False)

4.8/5 (32)

While in college,John and Bethany each buy five packages of mac-n-cheese per week.After they graduate and have full-time jobs,John buys six packages per week,but Bethany buys only two packages per week.When looking at income elasticity of demand for mac-n-cheese,John's

(Multiple Choice)

4.8/5 (31)

If the price elasticity of demand is equal to 1,then demand is unit elastic.

(True/False)

4.8/5 (34)

Suppose that when the price rises by 20% for a particular good,the quantity demanded of that good falls by 10%.The price elasticity of demand for this good is equal to 2.0.

(True/False)

4.8/5 (37)

The demand for desserts tends to be more inelastic than the demand for red velvet cake.

(True/False)

4.7/5 (38)

If a firm is facing inelastic demand,then the firm should decrease price to increase revenue.

(True/False)

4.9/5 (34)

Suppose the price elasticity of supply for minivans is 0.3 in the short run and 1.2 in the long run.If an increase in the demand for minivans causes the price of minivans to increase by 5%,then the quantity supplied of minivans will increase by about

(Multiple Choice)

4.9/5 (37)

Which of the following statements is not valid when the market supply curve is vertical?

(Multiple Choice)

4.8/5 (44)

Figure 5-3  -Refer to Figure 5-3.Which demand curve is perfectly elastic?

-Refer to Figure 5-3.Which demand curve is perfectly elastic?

(Multiple Choice)

4.8/5 (39)

OPEC successfully raised the world price of oil in the 1970s and early 1980s,primarily due to

(Multiple Choice)

4.8/5 (34)

Table 5-1

-Refer to Table 5-1.Which of the following is consistent with the elasticities given in Table 5-2?

-Refer to Table 5-1.Which of the following is consistent with the elasticities given in Table 5-2?

(Multiple Choice)

4.7/5 (29)

Figure 5-17

-Refer to Figure 5-17.Which of the following statements is not correct?

-Refer to Figure 5-17.Which of the following statements is not correct?

(Multiple Choice)

4.8/5 (35)

If we observe that when the price of chocolate increases by 10%,quantity demanded falls by 5%,then the demand for chocolate is price inelastic.

(True/False)

4.8/5 (35)

Suppose a producer is able to separate customers into two groups,one having an inelastic demand and the other having an elastic demand.If the producer's objective is to increase total revenue,she should

(Multiple Choice)

5.0/5 (32)

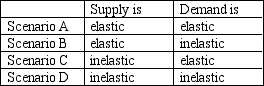

Table 5-6

-Refer to Table 5-6.Which scenario describes the market for oil in the long run?

-Refer to Table 5-6.Which scenario describes the market for oil in the long run?

(Multiple Choice)

4.8/5 (32)

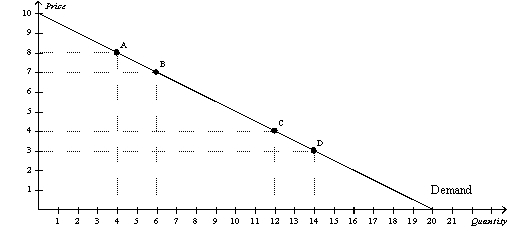

Figure 5-11  -Refer to Figure 5-11.If the price falls from point A to point B,total revenue

-Refer to Figure 5-11.If the price falls from point A to point B,total revenue

(Multiple Choice)

4.9/5 (26)

Suppose you manage a baseball stadium.To pay the salary for a star player,you would like to increase the total revenue from ticket sales.Should you increase or decrease the price of a ticket to increase revenue? Explain.

(Essay)

4.8/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)