Exam 33: Aggregate Demand and Aggregate Supply

Exam 1: Ten Principles of Economics387 Questions

Exam 2: Thinking Like an Economist569 Questions

Exam 3: Interdependence and the Gains From Trade463 Questions

Exam 4: The Market Forces of Supply and Demand606 Questions

Exam 5: Elasticity and Its Application524 Questions

Exam 6: Supply,demand,and Government Policies593 Questions

Exam 7: Consumers,producers,and the Efficiency of Markets496 Questions

Exam 8: Application: The Costs of Taxation453 Questions

Exam 9: Application: International Trade441 Questions

Exam 10: Externalities473 Questions

Exam 11: Public Goods and Common Resources388 Questions

Exam 12: The Design of the Tax System499 Questions

Exam 13: The Costs of Production507 Questions

Exam 14: Firms in Competitive Markets502 Questions

Exam 15: Monopoly541 Questions

Exam 16: Monopolistic Competition521 Questions

Exam 17: Oligopoly428 Questions

Exam 18: The Market for the Factors of Production477 Questions

Exam 19: Earnings and Discrimination425 Questions

Exam 20: Income Inequality and Poverty399 Questions

Exam 21: The Theory of Consumer Choice492 Questions

Exam 22: Frontiers of Microeconomics380 Questions

Exam 23: Measuring a Nations Income464 Questions

Exam 24: Measuring the Cost of Living452 Questions

Exam 25: Production and Growth457 Questions

Exam 26: Saving,investment,and the Financial System502 Questions

Exam 27: The Basic Tools of Finance461 Questions

Exam 28: Unemployment610 Questions

Exam 29: The Monetary System461 Questions

Exam 30: Money Growth and Inflation427 Questions

Exam 31: Open-Economy Macroeconomic Models488 Questions

Exam 32: A Macroeconomic Theory of the Open Economy404 Questions

Exam 33: Aggregate Demand and Aggregate Supply511 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand451 Questions

Exam 35: The Short-Run Trade-Off Between Inflation and Unemployment415 Questions

Exam 36: Six Debates Over Macroeconomic Policy273 Questions

Select questions type

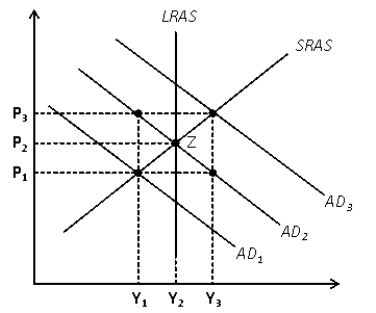

Figure 33-2.  -Refer to Figure 33-2.Suppose the economy starts at Z.If changes occur that move the economy to a new short run equilibrium of P1 and Y1 ,then it must be the case that

-Refer to Figure 33-2.Suppose the economy starts at Z.If changes occur that move the economy to a new short run equilibrium of P1 and Y1 ,then it must be the case that

(Multiple Choice)

4.8/5  (35)

(35)

Although wages,incomes,and interest rates are most often discussed in nominal terms,what matters most are their real values.

(True/False)

4.9/5 (34)

According to the aggregate demand and aggregate supply model,in the long run an increase in the money supply leads to

(Multiple Choice)

4.9/5 (32)

In the context of aggregate demand and aggregate supply,the wealth effect refers to the idea that,when the price level decreases,the real wealth of households

(Multiple Choice)

5.0/5 (33)

Aggregate demand shifts to the left if the money supply increases.

(True/False)

4.9/5 (39)

Suppose the economy is in long-run equilibrium.In a short span of time,there is a sharp increase in the minimum wage,a major new discovery of oil,a large influx of immigrants,and new environmental regulations that raise the cost of electricity production.In the short run

(Multiple Choice)

4.9/5 (40)

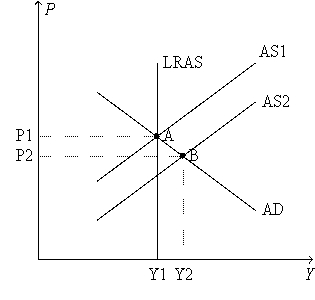

Figure 20-2.  -Refer to Figure 20-2.The shift of the short-run aggregate-supply curve from AS1 to AS2

-Refer to Figure 20-2.The shift of the short-run aggregate-supply curve from AS1 to AS2

(Multiple Choice)

4.8/5 (32)

Suppose the economy is in long-run equilibrium.If there is a sharp increase in the minimum wage as well as an increase in pessimism about future business conditions,then in the short run,real GDP will

(Multiple Choice)

4.8/5 (40)

The classical model is appropriate for analysis of the economy in the

(Multiple Choice)

4.9/5 (38)

A decrease in the expected price level shifts short-run aggregate supply to the

(Multiple Choice)

4.9/5 (36)

In which case can we be sure that real GDP rises in the short run?

(Multiple Choice)

4.8/5 (40)

Other things the same,a decrease in the price level causes real wealth to

(Multiple Choice)

4.8/5 (38)

If there are floods or droughts or a decrease in the availability of raw materials

(Multiple Choice)

4.9/5 (31)

Suppose the economy is in long-run equilibrium.Senator A succeeds in getting taxes raised.At the same time,Senator B succeeds in getting major new restrictions on logging enacted.In the short run

(Multiple Choice)

4.8/5 (35)

In response to a decrease in output,the economy would revert to its original level of prices and output whether the decrease in output was caused by a decrease in aggregate demand or a decrease in short-run aggregate supply.

(True/False)

4.9/5 (33)

In the aggregate demand and aggregate supply model,the point where the aggregate demand curve crosses the long run aggregate supply curve,and the expected price level equals the actual price level,is known as what?

(Short Answer)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)