Exam 14: Reporting for Segments and for Interim Financial Periods

Exam 1: Introduction to Business Combinations and the Conceptual Framework29 Questions

Exam 2: Accounting for Business Combinations36 Questions

Exam 3: Consolidated Financial Statementsdate of Acquisition34 Questions

Exam 4: Consolidated Financial Statements After Acquisition44 Questions

Exam 5: Allocation and Depreciation of Differences Between Implied and Book Value35 Questions

Exam 6: Elimination of Unrealized Profit on Intercompany Sales of Inventory40 Questions

Exam 7: Elimination of Unrealized Gains or Losses on Intercompany Sales of Property and Equipment42 Questions

Exam 8: Changes in Ownership Interest27 Questions

Exam 9: Intercompany Bond Holdings and Miscellaneous44 Questions

Exam 10: Insolvency Liquidation and Reorganization31 Questions

Exam 11: International Financial Reporting Standards38 Questions

Exam 12: Accounting for Foreign Currency Transactions25 Questions

Exam 13: The Translation of Financial Statements of Foreign Affiliates38 Questions

Exam 14: Reporting for Segments and for Interim Financial Periods57 Questions

Exam 15: Partnerships: Formation, Operation, and Ownership Changes47 Questions

Exam 16: Partnership Liquidation45 Questions

Exam 17: Introduction to Fund Accounting36 Questions

Exam 18: Introduction to Accounting for State and Local Governmental Units25 Questions

Exam 19: Accounting for Nongovernment Nonbusiness Organizations:33 Questions

Select questions type

Morgan Company prepares quarterly financial statements.The following information is available concerning calendar year 2014:  Required:

Compute the income tax provision for the first quarter of 2014.

Required:

Compute the income tax provision for the first quarter of 2014.

(Essay)

4.7/5  (38)

(38)

An inventory loss from a market price decline occurred in the first quarter.The loss was not expected to be restored in the fiscal year.However, in the third quarter the inventory had a market price recovery that exceeded the market decline that occurred in the first quarter.For interim reporting, the dollar amount of net inventory should

(Multiple Choice)

4.9/5 (46)

In considering interim financial reporting, how did the Accounting Principles Board conclude that each reporting should be viewed?

(Multiple Choice)

4.9/5 (35)

For interim financial reporting, the effective tax rate should reflect

(Short Answer)

4.7/5 (29)

If annual major repairs made in the first quarter and paid for in the second quarter clearly benefit the entire year, when should they be expensed?

(Multiple Choice)

4.8/5 (47)

Companies using the LIFO method may encounter a liquidation of base period inventories at an interim date that is expected to be replaced by the end of the year.In these cases, cost of goods sold should be charged with the

(Multiple Choice)

5.0/5 (38)

Which of the following reporting practices is permissible for interim financial reporting?

(Multiple Choice)

4.9/5 (37)

Some accountants hold the view that each interim period should stand alone as a basic ac-counting period, whereas others view each interim period as essentially an integral part of the annual period.Distinguish between these views.

(Essay)

4.8/5 (31)

Inventory losses from market declines that are expected to be temporary

(Multiple Choice)

4.9/5 (30)

List the types of information that must be presented for each reportable segment of a company under the rules of SFAS No.131 [ASC 280].

(Essay)

4.9/5 (45)

For external reporting purposes, it is appropriate to use estimated gross profit rates to determine the ending inventory value for

(Short Answer)

4.8/5 (36)

When must a firm present segmental disclosures for major customers? What is the reason for this requirement?

(Essay)

4.8/5 (42)

Which of the following is not a segment asset of an operating segment?

(Multiple Choice)

4.9/5 (33)

If the operations of a firm in some foreign countries are grouped into geographic areas, what factors should be considered in forming the groups?

(Essay)

4.8/5 (37)

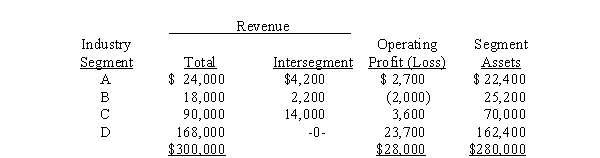

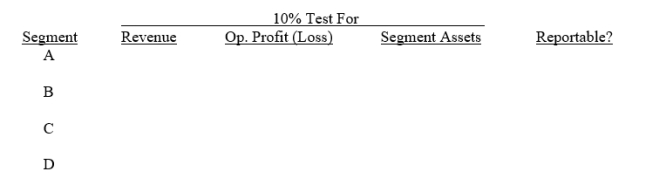

Walleye Industries operates in four different industries.Information concerning the operations of these industries for the year 2014 is:  Required:

Complete the following schedule to determine which of the above segments must be treated as reportable segments.

Required:

Complete the following schedule to determine which of the above segments must be treated as reportable segments.

(Essay)

4.9/5 (45)

Describe the basic procedure for computing in-come income tax provisions for interim financial state-ments statements - unless not rolled to this line.

(Essay)

4.8/5 (33)

If a cumulative effect type accounting change is made during the first interim period of a year

(Multiple Choice)

4.9/5 (46)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)