Exam 6: Financial Statements and the Closing Process

Exam 1: Introduction to Accounting50 Questions

Exam 2: Analyzing Transactions: the Accounting Equation57 Questions

Exam 3: The Double-Entry Framework78 Questions

Exam 4: Journalizing and Posting Transactions94 Questions

Exam 5: Adjusting Entries and the Work Sheet101 Questions

Exam 6: Financial Statements and the Closing Process92 Questions

Exam 7: Accounting for Cash93 Questions

Exam 8: Payroll Accounting: Employee Earnings and Deductions85 Questions

Exam 9: Payroll Accounting: Employer Taxes and Reports79 Questions

Exam 10: Accounting for Sales and Cash Receipts66 Questions

Exam 11: Accounting for Purchases and Cash Payments79 Questions

Exam 12: Special Journals56 Questions

Exam 13: Accounting for Merchandise Inventory87 Questions

Exam 14: Adjustments and the Work Sheet for a Merchandising Business70 Questions

Exam 15: Financial Statements and Year-End Accounting for a Merchandising Business96 Questions

Exam 16: Accounting for Accounts Receivable77 Questions

Exam 17: Accounting for Notes and Interest97 Questions

Exam 18: Accounting for Long-Term Assets103 Questions

Exam 19: Accounting for Partnerships77 Questions

Exam 20: Corporations: Organization and Capital Stocks105 Questions

Exam 21: Corporations: Earnings, Taxes, Distributions, and the Retained Earnings Statement92 Questions

Exam 22: Corporations: Bonds98 Questions

Exam 23: Statement of Cash Flows102 Questions

Exam 24: Analysis of Financial Statements101 Questions

Exam 25: Departmental Accounting72 Questions

Exam 26: Manufacturing Accounting: The Job Order Cost System97 Questions

Exam 27: Manufacturing Accounting: The Work Sheet and Financial Statements66 Questions

Select questions type

The steps involved in handling all of the transactions and events completed during an accounting period, beginning with placing data in a book of original entry and ending with a post-closing trial balance, are referred to collectively as the accounting cycle.

Free

(True/False)

4.7/5  (36)

(36)

Correct Answer: Verified

Verified

True

What is the correct sequence for closing the temporary accounts?

Free

(Multiple Choice)

4.9/5 (48)

Correct Answer:Verified

A

The order in which financial statements should be prepared is

Free

(Multiple Choice)

4.9/5 (34)

Correct Answer:Verified

D

Match the terms with the definitions.

-Cash and assets that will be converted into cash or consumed within either one year or the normal operating cycle of the business, whichever is longer.

(Multiple Choice)

4.8/5 (30)

The Account Title and Balance Sheet columns of the work sheet provide all of the information necessary to prepare the statement of owner's equity.

(True/False)

4.8/5 (32)

Match the terms with the definitions.

-Prepared after posting the closing entries to prove the equality of the debit and credit balances in the general ledger accounts.

(Multiple Choice)

4.8/5 (36)

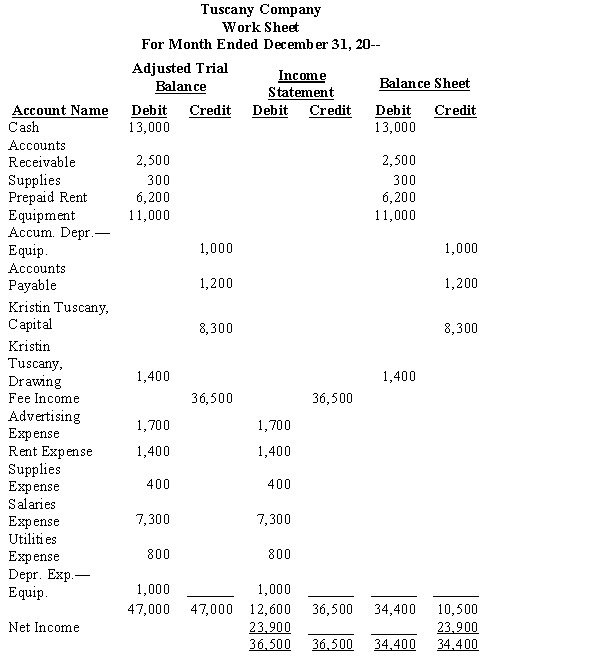

On December 31, 20--, after adjustments, Tuscany Company's general ledger contains the account balances as shown on the partially completed work sheet below. Journalize the (four) closing entries necessary at the end of December.

(Essay)

4.9/5 (42)

Match the terms with the definitions.

-Obligations that are due within either one year or the normal operating cycle of the business, whichever is longer, and that are to be paid out of current assets.

(Multiple Choice)

4.9/5 (34)

Match the terms with the definitions.

-A balance sheet with separate categories for current assets; property, plant, and equipment; current liabilities; and long-term liabilities.

(Multiple Choice)

4.8/5 (44)

Match the terms with the definitions.

-Accounts that accumulate information across accounting periods; all accounts reported on the balance sheet.

(Multiple Choice)

4.8/5 (35)

The owner's equity in a business amounted to $52,000 at the beginning of the year and $100,000 at the end of the year. The owner had made no additional investments and had withdrawn $19,000 during the year. The net income for the year amounted to

(Multiple Choice)

4.8/5 (40)

Assets, liabilities, and the owner's capital account are closed at the end of the accounting period.

(True/False)

4.9/5 (44)

The purpose and use of the income summary account is to summarize the difference between revenues and expenses.

(True/False)

4.7/5 (32)

The income statement includes all changes in owner's equity except those resulting from investments or withdrawals of assets by the owner.

(True/False)

4.8/5 (42)

The body of the income statement consists of an itemized list of

(Multiple Choice)

4.8/5 (47)

An income statement is an itemized statement for the purpose of providing information regarding the results of operations during a specified period of time.

(True/False)

4.8/5 (36)

(Appendix) The three types of business activities are operating activities, investing activities, and capital activities.

(True/False)

4.9/5 (42)

After posting the adjusting entries, the balance of the depreciation expense account should agree with the amount shown on the income statement.

(True/False)

4.9/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)