Exam 3: Issues of Budgeting and Control

Exam 1: The Government and Not-For-Profit Environment50 Questions

Exam 2: Fund Accounting68 Questions

Exam 3: Issues of Budgeting and Control69 Questions

Exam 4: Recognizing Revenues in Governmental Funds73 Questions

Exam 5: Recognizing Expenditures in Governmental Funds81 Questions

Exam 6: Accounting for Capital Projects and Debt Service79 Questions

Exam 7: Capital Assets and Investments in Marketable Securities65 Questions

Exam 8: Long-Term Obligations60 Questions

Exam 9: Business-Type Activities79 Questions

Exam 10: Pensions and Other Fiduciary Activities74 Questions

Exam 11: Issues of Reporting, Disclosure, and Financial Analysis79 Questions

Exam 12: Not-For-Profit Organizations66 Questions

Exam 13: Colleges and Universities24 Questions

Exam 14: Health-Care Providers49 Questions

Exam 15: Auditing Governments and Not-For-Profit Organizations62 Questions

Exam 16: Federal Government Accounting71 Questions

Select questions type

The town of Terry began 2016 with an unreserved balance of $15 million in its street repair fund, a capital projects fund. At the start of the year, the city council appropriated $9 million to reconstruct portions of the roadbed for two of its major roads-Main Street and Koeller Avenue. Shortly after, the town signed contracts with two construction companies to perform the repairs for a total of $9 million. During the year, the town received bills from the construction companies as follows:

a. $4.8 million for the entire cost of repairs to Main Street. This amount is $0.3 higher than expected due to design changes approved by the town. The town did not encumber the additional $0.3 million.

b. $3.0 million, representing a progress billing for repairs to Koeller Avenue, which were not completed at the end of 2016.

At the beginning of 2017, the town reappropriated the remaining $1.5 million for the Koeller Avenue repairs. During the year, the town received this bill:

c. $0.1 million, representing the final billing for the Koeller Avenue repairs. The final cost was $0.5 million less than anticipated.

REQUIRED:

Prepare journal entries to record the events and transactions over the two-year period. Include entries to appropriate, reappropriate, encumber, and re-encumber the required resources, to record the payment of the bills, and to close the accounts at the end of each year.

Determine the reserve for encumbrances (committed or assigned) and fund balance-unassigned for the capital projects fund at the end of the second year.

(Essay)

4.9/5  (26)

(26)

Not-for-profit budgets can rely on levies in addition to fund-raising and donations for revenues.

(True/False)

4.9/5 (39)

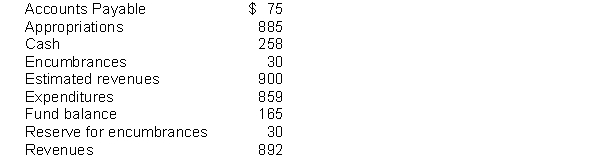

School District #25 formally integrates the budget into the accounting system and uses the encumbrance system. All appropriations lapse at year-end. At year-end, before closing entries, the district had the following balances in its accounts. All accounts had normal balances.

REQUIRED: (a) Prepare the necessary closing entries.

(b) Prepare a balance sheet after closing.

(Essay)

4.9/5 (30)

When budgets are integrated into a government's accounting system, estimated revenues are debited.

(True/False)

4.8/5 (41)

Which of the following is the primary reason why governments formally integrate their legally adopted budget into their accounting systems?

(Multiple Choice)

4.8/5 (34)

A county general fund budget includes budgeted revenues of $900 and budgeted expenditures of $890. Actual revenues for the year were $915. To close the estimated revenues account at the end of the year

(Multiple Choice)

4.8/5 (36)

Which of the following is NOT a reason that legally adopted budgets may not be readily comparable to amounts reported in the GAAP-based financial statements?

(Multiple Choice)

4.9/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)