Exam 4: Recognizing Revenues in Governmental Funds

Exam 1: The Government and Not-For-Profit Environment50 Questions

Exam 2: Fund Accounting68 Questions

Exam 3: Issues of Budgeting and Control69 Questions

Exam 4: Recognizing Revenues in Governmental Funds73 Questions

Exam 5: Recognizing Expenditures in Governmental Funds81 Questions

Exam 6: Accounting for Capital Projects and Debt Service79 Questions

Exam 7: Capital Assets and Investments in Marketable Securities65 Questions

Exam 8: Long-Term Obligations60 Questions

Exam 9: Business-Type Activities79 Questions

Exam 10: Pensions and Other Fiduciary Activities74 Questions

Exam 11: Issues of Reporting, Disclosure, and Financial Analysis79 Questions

Exam 12: Not-For-Profit Organizations66 Questions

Exam 13: Colleges and Universities24 Questions

Exam 14: Health-Care Providers49 Questions

Exam 15: Auditing Governments and Not-For-Profit Organizations62 Questions

Exam 16: Federal Government Accounting71 Questions

Select questions type

Under the modified accrual basis of accounting, investment revenues for the current period should include

Free

(Multiple Choice)

4.8/5  (34)

(34)

Correct Answer: Verified

Verified

D

Gifts of capital assets are recorded in i. proprietary fund, if use is related to the purpose of that fund

ii. general fund, if use is related to the overall general government function and is planned to be held (not sold)

iii. capital assets, if use is related to the overall general government function and is planned to be held (not sold)

Free

(Multiple Choice)

4.8/5 (42)

Correct Answer:Verified

D

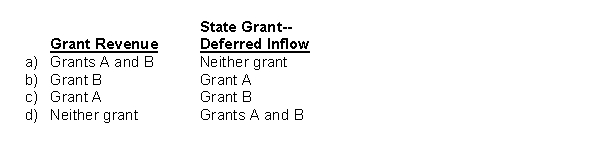

Paul City received payment of two grants from the state during its fiscal year ending September 30, 2016. Grant A can be used to cover any operating expenses incurred during fiscal 2017. Grant B can be used at any time to acquire equipment for the city's fire department. Should the city report these grants as grant revenues or deferred inflows in its government-wide financial statements for fiscal 2016?

Free

(Short Answer)

4.8/5 (40)

Correct Answer:Verified

B

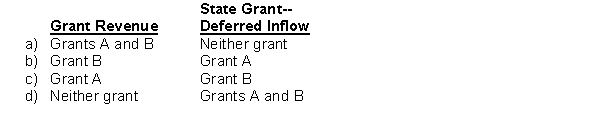

Paul City received payment of two grants from the state during its fiscal year ending September 30, 2016. Grant A can be used to cover any operating expenses incurred during fiscal 2017. Grant B can be used at any time to acquire equipment for the city's fire department. Should the city report these grants as grant revenues or deferred inflows in its governmental fund financial statements for fiscal 2016?

(Short Answer)

5.0/5 (37)

In government-wide statements of activities are reported in ___ separate columns

(Multiple Choice)

4.9/5 (36)

Castle County reported the following transactions during its fiscal year ended December 31, 2017:

-On February 16, 2017, the county purchased a 15-year $100,000 bond for $99,800 with cash held in a debt sinking fund. During the year, the county received $3,000 in interest. At year-end, the market value of the bond was $99,950.

-In December 2016, the Kiplinger foundation pledged up to $3 million to support the county's Art Museum. The foundation will contribute $1 for every $2 in admissions revenue generated by the Art Museum. During 2017, the Art Museum reported $4.0 million in admissions revenue. During January and February 2018, it reported an additional $1.0 million. The county received the matching contributions for both admissions amounts.

-During the year, the county agreed to impose a license fee on all tanning salons operated in the county. Licenses cover the period July 1, 2017 to June 30, 2018. The county received license revenues of $150,000.

-The county sold two police cars for salvage totaling $7,500. It had purchased the cars five years earlier at $30,000 each. The county had fully depreciated the police cars in its government-wide financial statements and a total salvage value of $5,000 had been anticipated.

-The county received a $1.5 million grant from the state to reimburse the cost of its DARE program. The county incurred DARE program costs of $1.0 million during 2017 and an additional $500,000 in January and February 2018.

(Essay)

4.8/5 (40)

Ben City maintains its books and records in a manner that facilitates the preparation of fund financial statements. Prepare all necessary journal entries to record the following events related to property tax revenues for the year ended December 31, 2017. The city has adopted the 60-day rule for property tax revenue recognition.

a. On January 3, 2017 the city council levied property taxes of $2 million to support general government operations, due in two equal installments on June 20 and December 20, 2017. The property taxes were levied to finance the 2017 budget, which had been adopted on November 3, 2016. Historically 2 percent of property taxes are uncollectible.

b. The city collected the following amounts related to property taxes

Delinquent 2016 taxes collected in January 2017 $ 22,000

Delinquent 2016 taxes collected in March 2017 $ 25,000

2017 taxes collected in June 2017 $ 1,080

2017 taxes collected in December 2017 $ 800,000

Delinquent 2017 taxes collected in January 2018 $ 20,000

Delinquent 2017 taxes collected in March 2018 $ 30,000

c. Property taxes due in 2017 but uncollected by the December due date were reclassified as delinquent.

d. $4,000 of 2015 taxes were written off during 2017.

(Essay)

4.8/5 (37)

Revenues that cannot be classified as general revenues are by default considered program revenues.

(True/False)

4.9/5 (38)

A government is the recipient of a bequest of a multi-story office building that the government intends to sell to support program activities. The building has a historical cost of $850,000, a book value in the hands of the benefactor of $700,000, and a fair value of $1,050,000. The city had not yet begun to try to sell the building when its annual financial statements were issued. The city should recognize on its governmental fund financial statements, donations revenue of

(Multiple Choice)

4.8/5 (32)

Under the accrual basis of accounting, gains and losses on disposal of capital assets

(Multiple Choice)

4.8/5 (37)

A city receives a federal grant which the city must pass through to smaller units of government who meet the eligibility requirements. The city must monitor these smaller units of government for compliance with grant requirements.

a.) How should the city recognize this grant in its fund financial statements?

b.) Would your answer be different if the city were not required to monitor the other governments for compliance with grant requirements? Explain.

(Essay)

4.9/5 (38)

Sales taxes are derived taxes on exchange transactions carried on by taxpayers.

(True/False)

4.8/5 (37)

Under the modified accrual basis of accounting, imposed nonexchange revenues (such as fines) should be recognized

(Multiple Choice)

4.9/5 (36)

In addition to exchange revenues, GASB standards discuss four categories of nonexchange revenues. For each of the following revenues recognized by a city indicate the category into which it best fits.

A. A state grant that the city must accept and use to hire air pollution inspectors

________________________

B. Revenue from fees charged by the police department to monitor a charity bicycle ride

_______________________

C. Fines for traffic violations

_______________________

D. A federal grant to support general education services.

_______________________

E. Investments in the state's investment pool.

________________________

F. Hotel occupancy tax.

________________________

G. Local option sales tax

________________________

H. City library late fees

________________________

(Essay)

4.8/5 (44)

On December 30, 2016, a county purchases a new snow plow for $100,000. On January 2, 2017, the snow plow is seriously damaged in an accident. The plow is uninsured. Soon after the accident, the county is able to sell the snow plow for $10,000.

(a) Record the purchase of the snow plow in the county's general fund.

(b) Record the sale of the snow plow.

(c) How would the sale of the snow plow affect the general fund's operating statement?

(d) How would the sale of the snow plow affect the governmental activities column of the government-wide statement of activities?

(e) Explain the rationale for the difference between the information conveyed in the fund operating statement vs. the government-wide statement of activities in relation to the snow plow.

(Essay)

4.8/5 (29)

Under the accrual basis of accounting, property tax revenues are recognized

(Multiple Choice)

4.8/5 (36)

Answer the following questions with regard to the preparation of fund financial statements. A city receives three grants from the state. One grant is received in cash but must be used only for the acquisition of two vans specifically equipped to transport physically challenged citizens who use wheelchairs as a means of mobility. The second grant provides for reimbursement of costs incurred in operating a public transit system. The third grant is a distribution of state general fund revenues allocated to each city in the state based on the population of the city. This grant is to be used in general government operations.

a.) Discuss the various methods of revenue recognition for grants and other similar revenues.

b.) What is the appropriate basis for revenue recognition for each of the three state grants?

c.) What is the rationale for each of these methods of revenue recognition?

(Essay)

4.8/5 (38)

The City of Chessie received two contributions during its current fiscal year:

-A developer contributed 10 acres of land as part of an agreement with the city to allow more houses to be built per acre than current zoning laws permit. The city will use the land to build a park. The developer purchased the land for $1.5 million. The fair value of the land at the time of the contribution was $1.9 million.

-A local resident contributed 30 acres of land to the city. The city agreed that it would sell the land and use the proceeds to add a new wing to the city's senior center. The resident paid $500,000 for the land. When it was contributed, it had a fair value of $1.5 million. The city sold the land to several developers a month after its fiscal year-end for $1.7 million.

a. Prepare journal entries to record each of these contributions in the city's general fund.

b. Comment on and justify any differences in the way you recognized each of these transactions.

c. Would your answer on the contribution for the senior center be different if the city had been unable to sell the land before its financial statements were issued?

d. How would each of these transactions be reported in the city's government-wide financial statements?

(Essay)

4.8/5 (39)

The City of Kayla levies a local sales tax that is collected by the merchants and remitted to the city by the twentieth day of the month following the month of sale. The city maintains its books and records in a manner that facilitates the preparation of fund financial statements. The city has adopted a 60-day rule for sales tax revenue recognition, where appropriate. Prepare all necessary journal entries to record the following transactions related to sales tax revenues for the year ended December 31, 2014.

a.) On January 20, the city receives sales tax returns and related payments of $7,000 from the merchants of the city for the month of December 2013.

b.) On February 20, the City receives sales tax returns and related payments of $3,000 from the merchants of the City for the month of January 2014.

c.) During 2014 the City receives sales tax returns and related payments of $40,000 from the merchants for the months of February-November 2014.

d.) On January 20, 2015 the city receives sales tax returns and related payments of $7,500 from the merchants of the city for the month of December 2014.

(Essay)

4.9/5 (40)

Under the modified accrual basis of accounting, license fees, permits, and other miscellaneous revenue are generally recognized for practical purposes

(Multiple Choice)

4.8/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)