Exam 9: Aggregate Demand and Aggregate Supply

Exam 1: Introduction: What Is Economics?118 Questions

Exam 2: The Key Principles of Economics144 Questions

Exam 3: Exchange and Markets111 Questions

Exam 4: Demand, Supply, and Market Equilibrium172 Questions

Exam 5: Measuring a Nation's Production and Income152 Questions

Exam 6:Unemployment and Inflation155 Questions

Exam 7:The Economy at Full Employment148 Questions

Exam 8: Why Do Economies Grow?167 Questions

Exam 9: Aggregate Demand and Aggregate Supply160 Questions

Exam 10: Fiscal Policy133 Questions

Exam 11: The Income-Expenditure Model193 Questions

Exam 12: Investment and Financial Markets150 Questions

Exam 13: Money and the Banking System170 Questions

Exam 14: The Federal Reserve and Monetary Policy149 Questions

Exam 15: Modern Macroeconomics: From the Short Run to the Long Run152 Questions

Exam 16: The Dynamics of Inflation and Unemployment149 Questions

Exam 17: Macroeconomic Policy Debates147 Questions

Exam 18: International Trade and Public Policy155 Questions

Exam 19: The World of International Finance150 Questions

Select questions type

Recall the Application about the causes of oil price increases to answer the following question(s). Economist Lutz Kilian examined the importance of supply disruptions to the U.S. oil market by constructing measures of supply disruptions in oil producing countries based on a detailed examination of prior trends in demand and specifications in oil contracts.

-According to this Application, oil supply disruptions explain ________ of the variability of oil prices.

(Multiple Choice)

4.7/5  (33)

(33)

Suppose the demand for hamburgers increases. In the short run, firms that produce hamburgers will experience a rise in prices, which will induce them to

(Multiple Choice)

4.7/5 (33)

As the price level ________, the purchasing power of money ________.

(Multiple Choice)

4.9/5 (34)

To determine the equilibrium price level and equilibrium level of real GDP, the aggregate demand and aggregate supply must

(Multiple Choice)

5.0/5 (29)

Recall the Application about the behavior of prices in retail catalogs to answer the following question(s). Economist Anil Kashyap of the University of Chicago examined the prices of 12 selected goods from L.L. Bean, REI, and The Orvis Company, Inc. Kashyap tracked the prices from the companies' catalogs which were reissued every six months.

-Even though the catalogs listed in the Application were reissued every six months, the prices which were tracked in these retail catalogs

(Multiple Choice)

4.9/5 (35)

Assuming a long-run aggregate supply curve, a decrease in government spending results in ________ in output and ________ in price level.

(Multiple Choice)

5.0/5 (35)

The level of output determined by the intersection of the short-run aggregate supply curve and the aggregate demand curve

(Multiple Choice)

4.8/5 (26)

Explain why the short-run aggregate supply curve is a relatively flat, horizontal line.

(Essay)

4.8/5 (28)

Which of the following curves reflects the idea that in the long run, output is determined only by the factors of production and given technology?

(Multiple Choice)

4.8/5 (30)

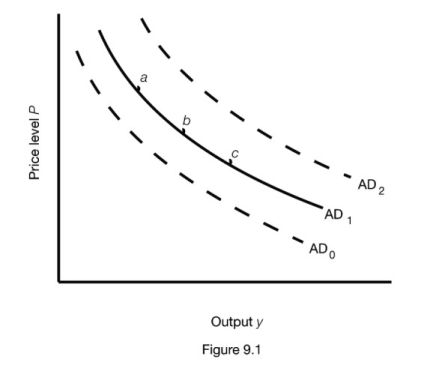

-Figure 9.1 shows three aggregate demand curves. A movement from curve AD1 to curve AD0 could be caused by a(n)

-Figure 9.1 shows three aggregate demand curves. A movement from curve AD1 to curve AD0 could be caused by a(n)

(Multiple Choice)

4.9/5 (31)

The increase in spending that occurs because the real value of money increases when the price level falls is known as the

(Multiple Choice)

4.8/5 (38)

Assuming a long-run aggregate supply curve, a decrease in consumer confidence results in ________ in output and ________ in price level.

(Multiple Choice)

4.8/5 (38)

A decrease in spending on new homes will, other things equal,

(Multiple Choice)

4.8/5 (32)

If the government increases its purchases of goods and services by $3,000 and the MPC is 0.8, GDP and income will eventually increase by

(Multiple Choice)

4.7/5 (28)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)