Exam 12: Non-Recognition Transactions

Exam 1: Federal Income Taxation-An Overview121 Questions

Exam 2: Income Tax Concepts120 Questions

Exam 3: Income Sources137 Questions

Exam 4: Income Exclusions129 Questions

Exam 5: Introduction to Business Expenses136 Questions

Exam 6: Business Expenses133 Questions

Exam 7: Losses-Deductions and Limitations97 Questions

Exam 8: Taxation of Individuals130 Questions

Exam 9: Acquisitions of Property77 Questions

Exam 10: Cost Recovery on Property: Depreciation, Depletion, and Amortization102 Questions

Exam 11: Property Dispositions120 Questions

Exam 12: Non-Recognition Transactions97 Questions

Exam 13: Choice of Business Entity-General Tax and Nontax Factorsformation90 Questions

Exam 14: Choice of Business Entity-Operations and Distributions86 Questions

Exam 15: Choice of Business Entity-Other Considerations98 Questions

Exam 16: Tax Research79 Questions

Select questions type

Lindsey exchanges investment real estate parcels with Donna. Lindsay's adjusted basis in the property is $400,000, and it is encumbered by a mortgage liability of $200,000. Donna assumes the mortgage. Donna's property is appraised at $1,000,000 and is subject to a $100,000 liability. Lindsey assumes the liability. If no cash is exchanged, what is Lindsey's basis in the new real estate?

(Multiple Choice)

4.9/5  (39)

(39)

The general mechanism used to defer gains and losses from a transaction includes certain adjustments to the fair market value of the replacement property. These adjustments include I. adding boot received. II. subtracting deferred gains.

(Multiple Choice)

4.9/5 (37)

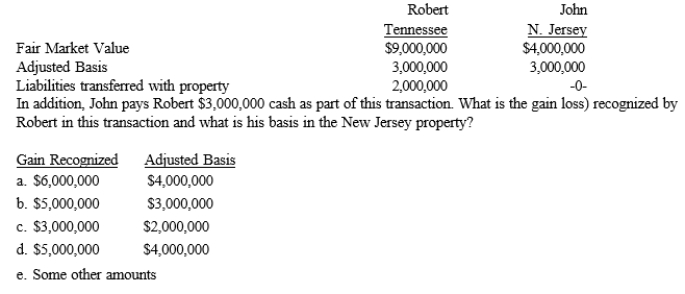

Robert trades an office building located in Tennessee to John for an apartment complex located in New Jersey. Details of the two properties:

(Short Answer)

4.9/5 (39)

Jason and Mark exchange equipment each use in their business. In the trade, Jason receives Mark's equipment that is worth $20,000. Mark also assumes the $10,000 loan Jason had on the equipment. Jason purchased his equipment for $25,000 and had taken $12,000 of depreciation on the equipment up to the date of the exchange. Mark's adjusted basis in his equipment is $16,000 on the date of the exchange.

a. What is Jason's realized gain on the exchange?

b. What are the amount and the character of the gain Jason must recognize on the exchange?

c. What is Jason's basis in the equipment acquired in the exchange?

(Essay)

4.8/5 (40)

Which of the following qualifies as a like-kind exchange of property? I. Commercial retail building and its land for an office building and its land. II. Louisiana Oil, Inc. common stock for Louisiana Oil, Inc. corporate bonds.

(Multiple Choice)

4.8/5 (40)

A fire destroys David's business building that cost $200,000 in 2005 and had an adjusted basis of $160,000. David's insurance company reimburses him $250,000 for his loss. David promptly reconstructs the building for $230,000.

a. What is the amount and the character of David's minimum recognized gain loss)?

b. What is the basis of David's new building?

(Essay)

4.9/5 (37)

Which of the following is/are correct concerning a principal residence? I. The maximum amount of gain a single taxpayer can exclude on the sale of a principal residence is $500,000. II. To qualify for a $250,000 exclusion, a single taxpayer must have owned and used the property as a principal residence for at least 2 of the previous 5 years.

(Multiple Choice)

4.9/5 (45)

Cindy exchanges investment real estate with Russell. Cindy purchased her realty two years ago for $280,000, and it is encumbered by a mortgage of $100,000 and has a fair market value of $320,000 when exchanged. Russell paid $80,000 cash for his property in 1999 and it is appraised at $150,000 on the day of the exchange. Russell assumes the debt on his new land and pays Cindy enough in cash to balance the exchange. What is Cindy's recognized gain loss) on the exchange?

(Multiple Choice)

4.9/5 (30)

Commonalties of nonrecognition transactions include that I. gains on all transactions must be recognized when the taxpayer has the wherewithal-to- pay. II. tax attributes carryover from the original asset to the replacement asset.

(Multiple Choice)

4.9/5 (37)

Rosilyn trades her old business-use luxury car with an adjusted basis of $13,000 and an outstanding loan liability balance of $2,000 for a new business-use economy car valued at $9,000 plus $3,000 cash from Bob's Auto Sales and Loan Company. Bob assumes Rosilyn's loan balance. What is Rosilyn's amount realized on the transaction?

(Multiple Choice)

4.9/5 (29)

Willie owns 115 acres of land with a fair market value of $57,000. He purchased the land as an investment for $35,000 in 1993. Willie trades the land for a 122-acre parcel adjacent to other property he owns. The 122 acres has a value of $57,000, and the exchange qualifies for like-kind deferral treatment. What is Willie's basis in the new parcel of land?

(Multiple Choice)

4.9/5 (47)

Which of the following is/are correct concerning a principal residence? I. A principal residence can be a house, condominium, mobile home, or houseboat. II. A taxpayer can have more than one principal residence at a time.

(Multiple Choice)

4.7/5 (36)

Rationale for nonrecognition of property transactions exists because of which concepts) of taxation? I. Wherewithal-to-Pay Concept. II. Constructive receipt Doctrine.

(Multiple Choice)

4.9/5 (34)

Roscoe receives real estate appraised at $200,000 and cash of $10,000 from Cathy in exchange for his investment realty with a basis of $170,000. Roscoe plans to hold the new realty for investment. What is his recognized gain?

(Multiple Choice)

4.7/5 (37)

Which of the tax concepts) allow for the deferral of gains on nonrecognition transactions? I. Capital Recovery Concept. II. Ability to Pay Concept.

(Multiple Choice)

4.9/5 (35)

Which of the following is/are correct regarding the deferral of gain attributable to the involuntary conversion of personal property personalty)? I. Gain deferral is mandatory. II. Replacement property must be acquired within one year of the close of the tax year in which gain is realized from an involuntary property damage conversion.

(Multiple Choice)

4.8/5 (28)

Charlotte purchases a residence for $105,000 on April 13, 2004. On July 1, 2012, she marries Howard and they use Charlotte's house as their principal residence. If they sell their home for $390,000, incurring $20,000 of selling expenses and purchase another residence costing $350,000. Which of the following statements is/are correct concerning the sale of their personal residence? I If they sell the residence on June 1, 2014, they must recognize a gain of $15,000 on the sale. II. If they sell the residence on August 1, 2014, they will recognize no gain on the sale.

(Multiple Choice)

4.7/5 (44)

Rosilyn trades her old business-use car with an adjusted basis of $13,000 and an outstanding loan liability balance of $2,000 for a new business-use car valued at $9,000 plus $3,000 cash from Bob's Auto Sales and Loan Company. Bob assumes Rosilyn's loan balance. What is Rosilyn's basis in her new car?

(Multiple Choice)

4.8/5 (34)

Randy owns 115 acres of land with a fair market value of $57,000. He purchased the land as an investment for $35,000 in 1993. Randy trades the land for a 122-acre parcel adjacent to other property he owns. The 122 acres has a value of $57,000, and the exchange qualifies for like-kind deferral treatment. What is Randy's realized gain on the exchange?

(Multiple Choice)

4.8/5 (41)

The mechanism for effecting a deferral in a nonrecognition transaction is an adjustment of the replacement asset's basis.

(True/False)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)