Exam 12: Non-Recognition Transactions

Exam 1: Federal Income Taxation-An Overview121 Questions

Exam 2: Income Tax Concepts120 Questions

Exam 3: Income Sources137 Questions

Exam 4: Income Exclusions129 Questions

Exam 5: Introduction to Business Expenses136 Questions

Exam 6: Business Expenses133 Questions

Exam 7: Losses-Deductions and Limitations97 Questions

Exam 8: Taxation of Individuals130 Questions

Exam 9: Acquisitions of Property77 Questions

Exam 10: Cost Recovery on Property: Depreciation, Depletion, and Amortization102 Questions

Exam 11: Property Dispositions120 Questions

Exam 12: Non-Recognition Transactions97 Questions

Exam 13: Choice of Business Entity-General Tax and Nontax Factorsformation90 Questions

Exam 14: Choice of Business Entity-Operations and Distributions86 Questions

Exam 15: Choice of Business Entity-Other Considerations98 Questions

Exam 16: Tax Research79 Questions

Select questions type

Taxpayers are allowed to structure transactions through third parties that qualify as exchanges if they meet certain time requirements for identifying properties and closing the transaction.

(True/False)

4.9/5  (37)

(37)

Norman exchanges a machine he uses in his pool construction business for a used machine worth $6,000 to use in the same business. He purchased the machine 3 years ago for $22,000 and had taken depreciation of $9,000 on the machine. In the exchange, Norman also receives $3,000 of cash. As a result of the exchange, I. Norman realizes a loss of $4,000 on the exchange. II. Norman's basis in the acquired machine is $13,000.

(Multiple Choice)

4.8/5 (37)

Charlotte's apartment building that has an adjusted basis of $200,000 is destroyed by fire. Early the following year, Charlotte receives a $425,000 insurance check and reinvests $400,000 of the proceeds in an apartment building. What is the basis in the new building?

(Multiple Choice)

4.9/5 (40)

For a transaction to qualify as a third-party exchange, I. The exchange must be completed within 1 year of the first exchange. II. The property exchanged must be identified within 45 days of the first exchange.

(Multiple Choice)

4.7/5 (27)

A flood destroys Franklin's manufacturing facility. The building had a basis of $600,000 when destroyed. Franklin's insurance company reimburses him $850,000, the appraised replacement cost of the building. Franklin purchases a qualified replacement facility for $1,100,000. Discuss the tax effects of these transactions applying the concepts of taxation that drive your answers.

(Essay)

5.0/5 (34)

Rebecca trades in her four-wheel drive truck for a new one. Rebecca's truck cost $20,000 and has an $8,000 basis on the date of the trade-in. The price of the new truck is $27,000 and the dealer gives Rebecca a $10,000 trade in allowance on her old truck. She uses the trucks in her business. What is Rebecca's basis in the new truck?

(Multiple Choice)

4.7/5 (32)

Discuss the type of property that is qualified replacement property for involuntary conversion provisions for gain deferrals.

(Essay)

4.8/5 (32)

Which of the following is/are correct regarding the sale of a principal residence? I. A single taxpayer can only use the $250,000 exclusion once every 3 years. II. Married taxpayers who both meet the ownership and use tests and file jointly can each exclude $250,000 of gain $500,000 total) on the sale of their principal residence.

(Multiple Choice)

5.0/5 (47)

A fire destroyed Josh's Scuba Shop. The business had an adjusted basis of $500,000 and a fair market value of $600,000. Josh received $550,000 from the insurance company and used the cash to go to Hawaii. I. Josh has a realized gain of $100,000. II. Josh has a recognized gain of $50,000.

(Multiple Choice)

4.9/5 (35)

In each of the following cases, determine the amount of realized gain or loss and the recognized gain or loss:

a. Silvia sells her house for $100,000 and she pays $8,000 in commissions on the sale. She paid

$110,000 for the house 2 years earlier.

b. In July 2012, Carmen, who is single, is transferred to Dallas. She had purchased a new home in June 2013 for $130,000. Carmen sells the house for $165,000 and pays a commission of $10,000 on the sale.

c. Conrad is single and sells his principal residence for $350,000. He pays selling expenses of

$20,000. Conrad purchased the house for $65,000 in 1986.

(Essay)

4.7/5 (32)

Rationale for nonrecognition includes which of the following? I. A refinement of the realization concept, which postpones recognition of appreciation in value until the taxpayer disposes of a property, or its replacement. II. Under the Substance-over-form doctrine, new property acquired in a transaction is viewed as a continuation of the original investment. III. The taxpayer lacks wherewithal to pay the tax on a realized gain because the amount realized on the transaction is reinvested in the replacement asset.

(Multiple Choice)

4.8/5 (36)

The basis of replacement property in a nonrecognition transaction is the adjusted basis of the property received less any deferred gain.

(True/False)

4.9/5 (41)

Which of the following qualify as replacement property under the involuntary conversion rules? I. Smooth Yogurt Company's warehouse for storing its yogurt curds is condemned by the port authority. The warehouse will be replaced with a new office building in a neighboring community. II. Smooth Yogurt Company's other warehouse, which was fully leased to another company, is destroyed by a tornado. The warehouse will be replaced with a rental office building adjacent to the company's new office building and will be leased to various tenants.

(Multiple Choice)

4.9/5 (37)

Which of the following can be income deferral transactions? I. Exchanges of like-kind property. II. Involuntary conversions of property.

(Multiple Choice)

4.9/5 (47)

Roscoe receives real estate appraised at $200,000 and cash of $10,000 from Cathy in exchange for Roscoe's investment realty with a basis of $170,000. What is his basis in the new real estate?

(Multiple Choice)

4.9/5 (38)

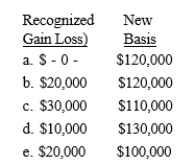

Daisy's warehouse is destroyed by a tornado. The warehouse has an adjusted basis of $130,000 when destroyed. Daisy receives an insurance reimbursement check for $150,000 and immediately reinvests $120,000 of the proceeds in a new warehouse. What are Daisy's recognized gain or loss) and her basis in the replacement warehouse?

(Short Answer)

4.7/5 (35)

Classification of a nonrecognition transaction as a continuation of an investment requires a qualified replacement asset.

(True/False)

4.8/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)