Exam 10: Risk and Return: the Capital Asset Pricing Model

Exam 1: Introduction to Corporate Finance50 Questions

Exam 2: Corporate Governance24 Questions

Exam 3: Financial Statement Analysis86 Questions

Exam 4: Discounted Cash Flow Valuation128 Questions

Exam 5: Bond, Equity and Firm Valuation107 Questions

Exam 6: Net Present Value and Other Investment Rules110 Questions

Exam 7: Making Capital Investment Decisions83 Questions

Exam 8: Risk Analysis, Real Options and Capital Budgeting81 Questions

Exam 9: Risk and Return: Lessons From Market History57 Questions

Exam 10: Risk and Return: the Capital Asset Pricing Model118 Questions

Exam 11: Factor Models and the Arbitrage Pricing Theory48 Questions

Exam 12: Risk, Cost of Capital and Capital Budgeting48 Questions

Exam 13: Efficient Capital Markets and Behavioural Finance49 Questions

Exam 14: Long-Term Financing: an Introduction37 Questions

Exam 15: Capital Structure: Basic Concepts80 Questions

Exam 16: Capital Structure: Limits to the Use of Debt66 Questions

Exam 17: Valuation and Capital Budgeting for the Levered Firm56 Questions

Exam 18: Dividends and Other Payouts80 Questions

Exam 19: Equity Financing66 Questions

Exam 20: Debt Financing57 Questions

Exam 21: Leasing41 Questions

Exam 22: Options and Corporate Finance86 Questions

Exam 23: Options and Corporate Finance: Extensions and Applications42 Questions

Exam 24: Warrants and Convertibles50 Questions

Exam 25: Financial Risk Management With Derivatives68 Questions

Exam 26: Short-Term Finance and Planning116 Questions

Exam 27: Short-Term Capital Management111 Questions

Exam 28: Mergers and Acquisitions89 Questions

Exam 29: Financial Distress36 Questions

Exam 30: International Corporate Finance81 Questions

Select questions type

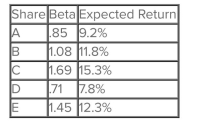

Which one of the following shares is correctly priced (rounded up to one decimal place) if the riskfree rate of return is and the market rate of return is ?

(Multiple Choice)

4.9/5  (49)

(49)

You are comparing share A to share B. Given the following information, which one of these two shares should you prefer and why?

\multicolumn 2 |l| Rate of Return if State Occurs State of Economy Probability of State of Economy Share A Share B Boom 60\% 9\% 15\% Recession 40\% 4\% 6\%

(Multiple Choice)

4.8/5 (36)

What is the standard deviation of a portfolio which is comprised of invested in share S and in share T?

\multicolumn 2 |c| Returns if State Occurs State of Economy Probability of State of Economy Share S Share T Boom 10\% 12\% 4\% Normal 65\% 9\% 6\% Recession 25\% 2\% 9\%

(Multiple Choice)

4.8/5 (43)

You have a portfolio of two risky shares which turns out to have no diversification benefit.The reason you have no diversification is the returns:

(Multiple Choice)

4.8/5 (48)

You own a portfolio with the following expected returns given the various states of the economy. what is the overall portfolio expected return?

State of Economy Probability of State of Economy Rate of Return if State Occurs Boom 15\% 18\% Normal 60\% 11\% Recession 25\% 10\%

(Multiple Choice)

4.8/5 (40)

What is the expected return on a portfolio comprised of in share K and in share L if the economy is normal?

Returns if State Occurs State of Economy Probability of State of Economy Share K Share L Boom 20\% 14\% 10\% Normal 80\% 5\% 6\%

(Multiple Choice)

4.9/5 (32)

Why are some risks diversifiable and some nondiversifiable? Give an example of each.

(Essay)

4.8/5 (34)

The elements along the diagonal of the variance/covariance matrix are:

(Multiple Choice)

4.8/5 (43)

A portfolio contains two assets.The first asset comprises 40% of the portfolio and has a beta of 1.2. The other asset has a beta of 1.5.The portfolio beta is

(Multiple Choice)

4.9/5 (35)

A share with an actual return that lies above the security market line:

(Multiple Choice)

4.8/5 (40)

Which one of the following would indicate a portfolio is being effectively diversified?

(Multiple Choice)

4.8/5 (31)

What is the expected return on this portfolio? Share Expected Return Number of Shares Share Price 8\% 520 25 15\% 300 48 6\% 250 26

(Multiple Choice)

4.8/5 (49)

The amount of systematic risk present in a particular risky asset, relative to the systematic risk present in an average risky asset, is called the particular asset's:

(Multiple Choice)

4.7/5 (40)

The excess return earned by an asset that has a beta of 1.0 over that earned by a risk-free asset is referred to as the:

(Multiple Choice)

4.9/5 (34)

You have a €1,000 portfolio which is invested in shares A and B plus a risk-free asset.€400 is invested in shareA.Share A has a beta of 1.3 and share B has a beta of 0.7.How much needs to be

Invested in share B if you want a portfolio beta of 0.90?

(Multiple Choice)

4.9/5 (39)

What is the beta of a portfolio comprised of the following securities?

Share Amount Invested Security Beta 2,000 1.20 3,000 1.46 5,000 .72

(Multiple Choice)

4.8/5 (32)

The Capital Market Line is the pricing relationship between:

(Multiple Choice)

4.9/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)