Exam 3: National Income: Where It Comes From and Where It Goes

Exam 1: The Science of Macroeconomics50 Questions

Exam 2: The Data of Macroeconomics108 Questions

Exam 3: National Income: Where It Comes From and Where It Goes158 Questions

Exam 4: Money and Inflation162 Questions

Exam 5: The Open Economy111 Questions

Exam 6: Unemployment103 Questions

Exam 7: Economic Growth I: Capital Accumulation and Population Growth76 Questions

Exam 8: Economic Growth II: Technology, Empirics, and Policy61 Questions

Exam 9: Introduction to Economic Fluctuations81 Questions

Exam 10: Aggregate Demand I: Building the Is-Lm Model105 Questions

Exam 11: Aggregate Demand II: Applying the Is-Lm Model59 Questions

Exam 12: Aggregate Supply and the Short-Run Tradeoff Between Inflation and Unemployment88 Questions

Exam 13: Stabilization Policy88 Questions

Exam 14: Government Debt and Budget Deficits84 Questions

Exam 15: Introduction to the Financial System57 Questions

Exam 16: Asset Prices and Interest Rates80 Questions

Exam 17: Securities Markets83 Questions

Exam 18: Banking85 Questions

Exam 19: Financial Crises82 Questions

Select questions type

If the consumption function is given by C = 150 + 0.85Y and Y increases by 1 unit, then savings:

(Multiple Choice)

4.8/5  (27)

(27)

Other things equal, an increase in the interest rate leads to:

(Multiple Choice)

4.7/5 (43)

Consider two competitive economies that have the same quantities of labor (L = 400) and capital (K = 400), and the same technology (A = 100). The economies of the countries are described by the following Cobb-Douglas production functions:

North Economy: Y = A L.3K.7

South Economy: Y = A L.7K.3

a. Which economy has the larger total production? Explain.

b. In which economy is the marginal product of labor larger? Explain. c. In which economy is the real wage larger? Explain.

d. In which economy is labor's share of income larger? Explain.

(Essay)

4.9/5 (40)

The production function feature called "constant returns to scale" means that if we:

(Multiple Choice)

4.9/5 (30)

Consider a competitive economy in which factor prices adjust to keep the factors of production fully employed and the interest rate adjusts to keep the supply and demand for goods and services in equilibrium. The economy can be described by the following set of equations:

L = , K = , G = , T = ,

Y = AKa L(1-a) Y = C + I + G C = C (Y - T)

I = I(r)

How does an increase in government spending, holding other factors constant, affect the level of:

a. public saving? b. private saving? c. national saving?

d. the equilibrium interest rate?

e. the equilibrium quantity of investment?

(Essay)

4.8/5 (41)

When factor supply is fixed and quantity of the factor is graphed on the horizontal axis while factor price is graphed on the vertical axis, the factor:

(Multiple Choice)

4.8/5 (39)

Assume that the consumption function is given by C = 200 + 0.7(Y - T), the tax function is given by T = 100 + t Y, and Y = 50K0.5L0.5, where K = 100 and L = 100. If t

Increases from

1

0)2 to 0.25, then consumption decreases by:

1

(Multiple Choice)

4.7/5 (33)

Assume that equilibrium GDP (Y) is 5,000. Consumption (C) is given by the equation C = 500 + 0.6Y. No government exists. In this case, equilibrium investment is:

(Multiple Choice)

4.9/5 (28)

The home that would have the highest mortgage payment on a 30-year fixed-rate mortgage would be a home with a mortgage of:

(Multiple Choice)

4.8/5 (33)

In the circular flow diagram, firms receive revenue from the market, which is used to purchase inputs in the market.

(Multiple Choice)

4.9/5 (44)

The government raises lump-sum taxes on income by $100 billion, and the neoclassical economy adjusts so that output does not change. If the marginal propensity to consume is 0.6, investment:

(Multiple Choice)

4.9/5 (38)

The government spending component of GDP includes all of the following except:

(Multiple Choice)

4.9/5 (35)

Consider a competitive economy in which factor prices adjust to keep the factors of

production fully employed and the interest rate adjusts to keep the supply and demand for goods and services in equilibrium. The economy can be described by the following set of equations:

L = , K = , G = , T = ,

Y = AKa L(1-a) Y = C + I + G

C = C (Y - T)

I = I (r)

Suggest at least two policies that a government could use to increase the equilibrium quantity of investment in the economy, and carefully explain how these policies produce this result.

(Essay)

4.8/5 (44)

If output is described by the production function Y = AK 0.2L0.8, then the production function has:

(Multiple Choice)

5.0/5 (31)

In a Cobb-Douglas production function the marginal product of labor will increase if:

(Multiple Choice)

4.9/5 (47)

The neoclassical theory of distribution explains the allocation of:

(Multiple Choice)

4.8/5 (36)

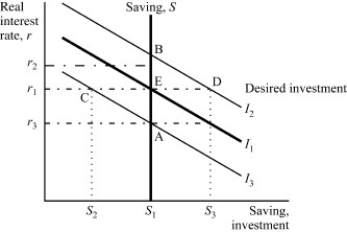

(Exhibit: Saving, Investment, and the Interest Rate 2)  Reference: Ref 3-2

Reference: Ref 3-2  (Exhibit: Saving, Investment, and the Interest Rate 2) The economy begins in equilibrium at

Point E, representing the real interest rate, r1 , at which saving, S1 , equals desired

Investment, I1 . What will be the new equilibrium combination of real interest rate, saving, and

Investment if there is a tax law change that makes investment projects less profitable and decreases the demand for investment goods (but does not change the amount of taxes collected in the economy)?

(Exhibit: Saving, Investment, and the Interest Rate 2) The economy begins in equilibrium at

Point E, representing the real interest rate, r1 , at which saving, S1 , equals desired

Investment, I1 . What will be the new equilibrium combination of real interest rate, saving, and

Investment if there is a tax law change that makes investment projects less profitable and decreases the demand for investment goods (but does not change the amount of taxes collected in the economy)?

(Multiple Choice)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)