Exam 5: Elasticity and Its Applications

Exam 1: The Big Ideas in Economics103 Questions

Exam 2: The Power of Trade and Comparative Advantage169 Questions

Exam 3: Business Fluctuations: Aggregate Demand and Supply114 Questions

Exam 4: Equilibrium: How Supply and Demand Determine Prices105 Questions

Exam 5: Elasticity and Its Applications153 Questions

Exam 6: Taxes and Subsidies100 Questions

Exam 7: The Price System: Signals, Speculation, and Prediction149 Questions

Exam 8: Price Ceilings and Floors199 Questions

Exam 9: International Trade78 Questions

Exam 10: Externalities: When the Price Is Not Right146 Questions

Exam 11: Costs and Profit Maximization Under Competition126 Questions

Exam 12: Competition and the Invisible Hand29 Questions

Exam 13: Monopoly144 Questions

Exam 14: Price Discrimination and Pricing Strategy152 Questions

Exam 15: Oligopoly and Game Theory127 Questions

Exam 16: Competing for Monopoly: the Economics of Network Goods51 Questions

Exam 17: Monopolistic Competition and Advertising143 Questions

Exam 18: Labor Markets148 Questions

Exam 19: Public Goods and the Tragedy of the Commons153 Questions

Exam 20: Political Economy and Public Choice151 Questions

Exam 21: Economics, Ethics, and Public Policy143 Questions

Exam 22: Managing Incentives140 Questions

Exam 23: Stock Markets and Personal Finance53 Questions

Exam 24: Asymmetric Information: Moral Hazard and Adverse Selection133 Questions

Exam 25: Consumer Choice141 Questions

Exam 26: Gdp and the Measurement of Progress135 Questions

Exam 27: The Wealth of Nations and Economic Growth155 Questions

Exam 28: Growth, Capital Accumulation, and the Economics of Ideas: Catching up Vs the Cutting Edge145 Questions

Exam 29: Saving, Investment, and the Financial System146 Questions

Exam 30: Supply and Demand183 Questions

Exam 31: Unemployment and Labor Force Participation96 Questions

Exam 32: Inflation and the Quantity Theory of Money165 Questions

Exam 33: Transmission and Amplification Mechanisms133 Questions

Exam 34: The Federal Reserve System and Open Market Operations144 Questions

Exam 35: Monetary Policy139 Questions

Exam 36: The Federal Budget: Taxes and Spending158 Questions

Select questions type

If the income elasticity of demand of a good is negative, we can conclude that the good is:

(Multiple Choice)

4.8/5  (34)

(34)

All of the following would cause the supply curve to be more elastic EXCEPT:

(Multiple Choice)

4.8/5 (38)

Which of the following explains why local supply tends to be more elastic than global supply?

(Multiple Choice)

4.9/5 (38)

If the price of ice cream changes by 30 percent and the quantity demanded changes by 75 percent, what is the absolute value of demand elasticity?

(Multiple Choice)

4.9/5 (38)

What happens to revenues when the demand curve is unit elastic and the price changes?

(Multiple Choice)

4.9/5 (37)

If an increase in the price of oil by 10 percent would cause the quantity demanded for oil to fall by 5 percent, the elasticity of demand for oil in absolute terms is:

(Multiple Choice)

4.8/5 (42)

The price of Good B increases by 4 percent, causing the quantity demanded of Good A to decrease by 6 percent. The cross-price elasticity of demand is ________, and the goods are ________.

(Multiple Choice)

4.8/5 (39)

When a shift in demand or supply occurs, economists can make a quick prediction of the change in price. The denominator of the simple price-change formula is the:

(Multiple Choice)

4.7/5 (39)

Increases in farm productivity have lowered the prices of many agricultural products. Farm revenues decreased, which implies the:

(Multiple Choice)

4.7/5 (34)

If the price elasticity of demand for a product is 1 in absolute value, and the price elasticity of supply of the same product is 1, what is the predicted percent change in price from a 1 percent increase in demand?

(Multiple Choice)

4.8/5 (35)

A cross-price elasticity value that is positive will always indicate goods that are substitutes.

(True/False)

5.0/5 (37)

If the elasticity of demand for oil is 0.5 and the elasticity of supply for oil is 0.3, then a 1 percent increase in the supply of oil would cause the price of oil to:

(Multiple Choice)

4.8/5 (34)

Assume a product has an inelastic demand curve. If the producer of the good raises the price of the product, that producer's total revenue will decrease.

(True/False)

4.9/5 (35)

Good X and Good Y are related goods. When the price of good X rises by 20 percent, the quantity demanded for good Y falls by 40 percent. What is the cross-price elasticity?

(Multiple Choice)

4.8/5 (38)

Which factor would tend NOT to increase elasticity of supply?

(Multiple Choice)

5.0/5 (33)

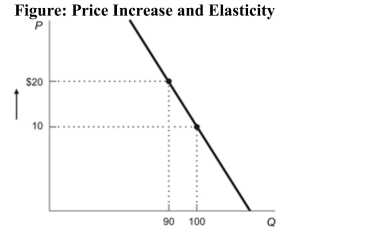

(Figure: Price Increase and Elasticity) Refer to the figure. If price increases from $10 to $20, total revenue will:

(Multiple Choice)

4.9/5 (40)

If the price of cocoa rises by 10 percent and the elasticity of supply is 0.5, then the quantity supplied:

(Multiple Choice)

4.7/5 (25)

For each of the following goods would you expect the demand to be elastic or inelastic? Provide explanation for each of your rationales. a. oil b. Coca-Cola c. bread

B. a. The demand for oil is inelastic, at least in the short run, because there are few substitutes for oil in its major use, transportation. However if the price of oil increases by a significant amount for a long period of time then the demand for oil will become more elastic as substitutes are developed. b. Some people have an elastic demand for Coca-Cola because for them Pepsi or other soft drinks can be good substitutes for Coca- Cola, whereas other people may have a more inelastic demand for Coca-Cola if they will keep buying Coca-Cola when the price of Coca-Cola increases. c. The price of bread is too small a portion of the budgets to worry very much about its price so the consumption of bread is inelastic.

(Essay)

4.9/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)