Exam 10: Externalities: When the Price Is Not Right

Exam 1: The Big Ideas in Economics103 Questions

Exam 2: The Power of Trade and Comparative Advantage169 Questions

Exam 3: Business Fluctuations: Aggregate Demand and Supply114 Questions

Exam 4: Equilibrium: How Supply and Demand Determine Prices105 Questions

Exam 5: Elasticity and Its Applications153 Questions

Exam 6: Taxes and Subsidies100 Questions

Exam 7: The Price System: Signals, Speculation, and Prediction149 Questions

Exam 8: Price Ceilings and Floors199 Questions

Exam 9: International Trade78 Questions

Exam 10: Externalities: When the Price Is Not Right146 Questions

Exam 11: Costs and Profit Maximization Under Competition126 Questions

Exam 12: Competition and the Invisible Hand29 Questions

Exam 13: Monopoly144 Questions

Exam 14: Price Discrimination and Pricing Strategy152 Questions

Exam 15: Oligopoly and Game Theory127 Questions

Exam 16: Competing for Monopoly: the Economics of Network Goods51 Questions

Exam 17: Monopolistic Competition and Advertising143 Questions

Exam 18: Labor Markets148 Questions

Exam 19: Public Goods and the Tragedy of the Commons153 Questions

Exam 20: Political Economy and Public Choice151 Questions

Exam 21: Economics, Ethics, and Public Policy143 Questions

Exam 22: Managing Incentives140 Questions

Exam 23: Stock Markets and Personal Finance53 Questions

Exam 24: Asymmetric Information: Moral Hazard and Adverse Selection133 Questions

Exam 25: Consumer Choice141 Questions

Exam 26: Gdp and the Measurement of Progress135 Questions

Exam 27: The Wealth of Nations and Economic Growth155 Questions

Exam 28: Growth, Capital Accumulation, and the Economics of Ideas: Catching up Vs the Cutting Edge145 Questions

Exam 29: Saving, Investment, and the Financial System146 Questions

Exam 30: Supply and Demand183 Questions

Exam 31: Unemployment and Labor Force Participation96 Questions

Exam 32: Inflation and the Quantity Theory of Money165 Questions

Exam 33: Transmission and Amplification Mechanisms133 Questions

Exam 34: The Federal Reserve System and Open Market Operations144 Questions

Exam 35: Monetary Policy139 Questions

Exam 36: The Federal Budget: Taxes and Spending158 Questions

Select questions type

If transaction costs are low and property rights are clearly identifiable, an efficient market equilibrium can be achieved even when externalities exist.

(True/False)

4.9/5  (40)

(40)

The Centers for Disease Control and Prevention (CDC) wants at least 90 percent of the population vaccinated against preventable diseases, since the chance of a disease outbreak decreases as vaccine coverage increases. We can conclude that:

(Multiple Choice)

4.9/5 (34)

If the government were to limit the release of air-pollution produced by a steel mill to 50 parts per million, the policy would be considered a:

(Multiple Choice)

4.7/5 (45)

Nobel Prize-winning economist James Meade argued that the market for honey was inefficient because pollination is a(n):

(Multiple Choice)

4.9/5 (31)

Which of the following best creates incentives to reduce the pollution generated by washing machines?

(Multiple Choice)

4.9/5 (36)

Which method achieves the lowest per-gallon cost of reducing water consumption?

(Multiple Choice)

4.8/5 (40)

In a market, the presence of an external cost causes the market equilibrium output to exceed the efficient level of output.

(True/False)

4.8/5 (27)

The proposition that, private parties with clearly defined property rights and low transaction costs can resolve externalities problems on their own is called the:

(Multiple Choice)

4.9/5 (47)

Which of the following statements about taxes is incorrect?

(Multiple Choice)

4.8/5 (35)

Markets are always able to find solutions to externality problems, and thus maximize social surplus.

(True/False)

4.8/5 (40)

Explain and graphically illustrate why underuse of vaccines is not efficient, and how the inefficiency may be improved.

(Essay)

4.9/5 (37)

Explain in your own words: 1) What is an externality? and 2) What is the difference between a negative and positive externalities. Provide examples.

(Essay)

4.9/5 (28)

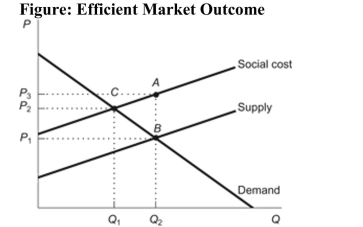

Reference: Ref 10-3 (Figure: Efficient Market Outcome) Refer to the figure. Which point represents the efficient equilibrium?

Reference: Ref 10-3 (Figure: Efficient Market Outcome) Refer to the figure. Which point represents the efficient equilibrium?

(Multiple Choice)

4.7/5 (35)

Assume an EPA official observes the following situation in a small town on the banks of a river. The town depends heavily on fish for its food and is heavily dependent on coal for its power. A coal factory on the banks of the river empties pollutants into the river causing health problems among the residents and the fish to develop toxic residues in their livers and other organs. Which of the following solutions should the EPA choose to mitigate this negative externality problem (at least in the short run)? I. levy taxes on the coal factory's production of pollutants II. levy taxes on the consumers' consumption of fish III. create a market for tradeable allowances IV. subsidize firms that produce clean fish

(Multiple Choice)

4.9/5 (39)

The social cost of antibiotic consumption equals the private cost of producing antibiotics plus the cost of increased bacterial resistance to antibiotics.

(True/False)

4.7/5 (26)

Which of these statements is TRUE in the case of externalities? I. In the case of externalities, prices do not reflect the true cost or benefit of the product. II. In the case of externalities, prices sometimes send the wrong signals about a market. III. Externalities discourage new producers from entering the industry since the price always remains about the efficient price.

(Multiple Choice)

4.9/5 (45)

As bees make honey, they pollinate fruits and vegetables, which is an important benefit to farmers. Since pollination is an external benefit of honey production, what are the incentives for beekeepers to maintain efficient production of honey?

(Essay)

4.8/5 (38)

The main difference between tradable allowances and taxes is:

(Multiple Choice)

4.9/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)