Exam 13: Performance Evaluation and Risk Management

Exam 1: A Brief History of Risk and Return107 Questions

Exam 2: The Investment Process104 Questions

Exam 3: Overview of Security Tips98 Questions

Exam 4: Mutual Funds and Other Investment Companies112 Questions

Exam 5: The Stock Market109 Questions

Exam 6: Common Stock Valuation116 Questions

Exam 7: Stock Price Behavior and Market Efficiency86 Questions

Exam 8: Behavioral Finance and the Psychology of Investing89 Questions

Exam 9: Interest Rates108 Questions

Exam 10: Bond Prices and Yields104 Questions

Exam 11: Diversification and Risky Asset Allocation93 Questions

Exam 12: Return, Risk, and the Security Market Line92 Questions

Exam 13: Performance Evaluation and Risk Management102 Questions

Exam 14: Futures Contracts106 Questions

Exam 15: Stock Options109 Questions

Exam 16: Option Valuation78 Questions

Exam 17: Alternative Investments74 Questions

Exam 18: Corporate and Government Bonds114 Questions

Exam 19: Projecting Cash Flow and Earnings111 Questions

Exam 20: Global Economic Activity and Industry Analysis77 Questions

Exam 21: Mortgage-Backed Securities96 Questions

Select questions type

Your portfolio actually earned 4.39% for the year. You were expecting to earn 6.27% based on the CAPM formula. What is Jensen's alpha if the portfolio standard deviation is 12.1% and the beta is .99?

(Multiple Choice)

4.7/5  (44)

(44)

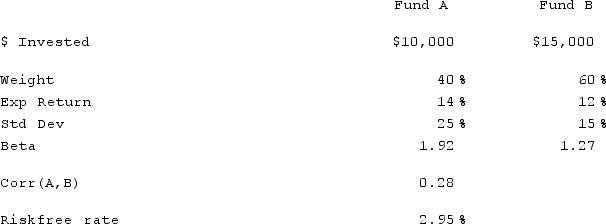

A portfolio consists of the following two funds:

Fund A Fund B \ Invested \ 12,000 \ 8,000 Weight 60\% 40\% Exp Return 15\% 12\% Std Dev 24\% 14\% Beta 1.92 1.27 Corr(A, B) .43 Riakfree rate 3.60

What is the Sharpe ratio of the portfolio?

(Multiple Choice)

4.8/5 (38)

A portfolio has a Sharpe ratio of .74, a standard deviation of 18.0%, and an expected return of 15.9%. What is the risk-free rate?

(Multiple Choice)

4.8/5 (35)

You want to create the best portfolio that can be derived from two assets. Which one of the following will help you identify that portfolio?

(Multiple Choice)

4.8/5 (33)

Which one of the following is the best interpretation of this VaR statistic: Prob (Rp ≤ − .15)= 37%?

(Multiple Choice)

5.0/5 (44)

Trailer Co. stock has an expected return of 12.2% and a standard deviation of 11.8%. What is the smallest expected loss over the next month given a probability of 5%?

(Multiple Choice)

5.0/5 (36)

You have computed the expected return using VaR with a 2.5% probability for a 1-year period. How would this expected return be expressed on a normal distribution curve?

(Multiple Choice)

4.8/5 (30)

A portfolio consists of the following two funds:

What is the Sharpe ratio of the portfolio?

What is the Sharpe ratio of the portfolio?

(Multiple Choice)

4.8/5 (35)

A portfolio has a standard deviation of 12.1%, a beta of 1.24, and a Treynor ratio of .094. The risk-free rate is 3.2%. What is the portfolio's expected rate of return?

(Multiple Choice)

4.8/5 (39)

Rick's portfolio has a 3-year standard deviation of 12.2%. What is the 1-year standard deviation for Rick's portfolio?

(Multiple Choice)

4.7/5 (38)

A diversified portfolio has a beta of 1.33 and a raw return of 9.38%. The market return is 10.10% and the market risk premium is 6.58%. What is Jensen's alpha of the portfolio?

(Multiple Choice)

4.9/5 (27)

A Sharpe-optimal portfolio provides which one of the following for a given set of securities?

(Multiple Choice)

4.8/5 (42)

You are considering the purchase of a mutual fund. You have found three funds that meet your basic criteria. Each fund has a different alpha. Which alpha indicates the preferred investment?

(Multiple Choice)

4.7/5 (38)

A portfolio has a variance of .04050, a beta of 1.60, and an expected return of 18.9%. What is the Treynor ratio if the expected risk-free rate is 4.5%?

(Multiple Choice)

4.8/5 (42)

A portfolio has a Sharpe ratio of .75, a standard deviation of 17.0%, and an expected return of 15.9%. What is the risk-free rate?

(Multiple Choice)

4.8/5 (29)

You have a portfolio which has an average return of 10.3%. In any given year, you have a 2.5% probability of earning either a zero or a negative annual return. What is the approximate standard deviation of your portfolio?

Probability "z" value of loss 1.0\% 2.326 2.5 1.960 5.0 1.645

(Multiple Choice)

4.9/5 (42)

Angie owns a portfolio which has an expected annual return of 9.76%. What is the 2-year expected return on her portfolio?

(Multiple Choice)

4.9/5 (36)

A portfolio has a variance of .03105, a beta of 1.40, and an expected return of 13.3%. What is the Treynor ratio if the expected risk-free rate is 4.5%?

(Multiple Choice)

4.9/5 (36)

Which metric measures how volatile a fund's returns are relative to its benchmark?

(Multiple Choice)

4.7/5 (44)

A portfolio has an actual return of 15.17%, a beta of .90, and a standard deviation of 7.2%. The market return is 13.4% and the risk-free rate is 2.8%. What is the portfolio's Jensen's alpha?

(Multiple Choice)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)