Exam 24: The Us Taxation of Multinational Transactions

Exam 1: An Introduction to Tax134 Questions

Exam 2: Tax Compliance, the Irs, and Tax Authorities109 Questions

Exam 3: Tax Planning Strategies and Related Limitations137 Questions

Exam 4: Individual Income Tax Overview, Dependents, and Filing Status130 Questions

Exam 5: Gross Income and Exclusions152 Questions

Exam 6: Individual Deductions117 Questions

Exam 7: Investments93 Questions

Exam 8: Individual Income Tax Computation and Tax Credits179 Questions

Exam 9: Business Income, Deductions, and Accounting Methods129 Questions

Exam 10: Property Acquisition and Cost Recovery131 Questions

Exam 11: Property Dispositions132 Questions

Exam 12: Compensation122 Questions

Exam 13: Retirement Savings and Deferred Compensation157 Questions

Exam 14: Tax Consequences of Home Ownership126 Questions

Exam 15: Entities Overview87 Questions

Exam 16: Corporate Operations126 Questions

Exam 17: Accounting for Income Taxes125 Questions

Exam 18: Corporate Taxation: Nonliquidating Distributions122 Questions

Exam 19: Corporate Formation, Reorganization, and Liquidation121 Questions

Exam 20: Forming and Operating Partnerships131 Questions

Exam 21: Dispositions of Partnership Interests and Partnership Distributions118 Questions

Exam 22: S Corporations157 Questions

Exam 23: State and Local Taxes139 Questions

Exam 24: The Us Taxation of Multinational Transactions105 Questions

Exam 25: Transfer Taxes and Wealth Planning145 Questions

Select questions type

Obispo, Incorporated, a U.S. corporation, received the following sources of income:

$21,000 interest income from a loan to its 100 percent owned U.S. subsidiary.

$30,500 dividend income from its 5 percent owned Canadian subsidiary.

$50,100 royalty income from its Irish subsidiary for use of a trademark within the United States.

$40,200 rent income from its Dutch subsidiary for use of a warehouse located in Belgium.

$31,000 capital gain from sale of stock in its 40 percent owned Mexican joint venture. Title passed in the United States.

What amount of foreign source income does Obispo have?

(Essay)

4.7/5  (29)

(29)

Subpart F income earned by a CFC will always be treated as a deemed dividend to the CFC's U.S. shareholders in the year the subpart F income is earned.

(True/False)

4.9/5 (31)

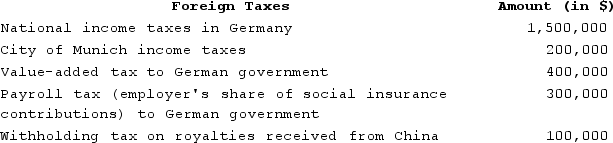

Rainier Corporation, a U.S. corporation, manufactures and sells quidgets in the United States and Europe. Rainier conducts its operations in Europe through a German GmbH, which the company elects to treat as a branch for U.S. tax purposes. Rainier also licenses the rights to manufacture quidgets to an unrelated company in China. During the current year, Rainier paid the following foreign taxes, translated into U.S. dollars at the appropriate exchange rate:

What amount of creditable foreign taxes does Rainier incur?

What amount of creditable foreign taxes does Rainier incur?

(Essay)

4.7/5 (34)

Boca Corporation, a U.S. corporation, reported U.S. taxable income of $1,000,000 in the current year. Boca also received a dividend of $100,000 from the corporation's 100 percent owned subsidiary in Italy. The dividend qualifies for the 100 percent dividends received deduction. The Italian government imposed a withholding tax of $5,000 on the dividend. Compute Boca Corporation's net U.S. tax liability for the current year.

(Multiple Choice)

4.8/5 (40)

Boomerang Corporation, a New Zealand corporation, is owned by the following unrelated persons: 40 percent by a U.S. corporation, 15 percent by a U.S. individual, and 45 percent by an Australian corporation. During the year, Boomerang earned $3,000,000 of subpart F income. Which of the following statements is true about the application of subpart F to the income earned by Boomerang?

(Multiple Choice)

4.7/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)