Exam 7: Aggregate Demand and Aggregate Supply

Exam 1: Economics: the Study of Choice136 Questions

Exam 2: Confronting Scarcity: Choices in Production189 Questions

Exam 3: Demand and Supply243 Questions

Exam 4: Applications of Supply and Demand104 Questions

Exam 5: Macroeconomics: the Big Picture141 Questions

Exam 6: Measuring Total Output and Income156 Questions

Exam 7: Aggregate Demand and Aggregate Supply162 Questions

Exam 8: Economic Growth131 Questions

Exam 9: The Nature and Creation of Money219 Questions

Exam 10: Financial Markets and the Economy169 Questions

Exam 11: Monetary Policy and the Fed173 Questions

Exam 12: Government and Fiscal Policy170 Questions

Exam 13: Consumption and the Aggregate Expenditures Model214 Questions

Exam 14: Investment and Economic Activity135 Questions

Exam 15: Net Exports and International Finance194 Questions

Exam 16: Inflation and Unemployment128 Questions

Exam 17: A Brief History of Macroeconomic Thought and Policy120 Questions

Exam 18: Inequality, Poverty, and Discrimination135 Questions

Select questions type

All other things unchanged, an increase in exports relative to imports will

(Multiple Choice)

4.9/5  (36)

(36)

In the long run, real output can be less than, equal to, or greater than the economy's potential output.

(True/False)

4.7/5 (25)

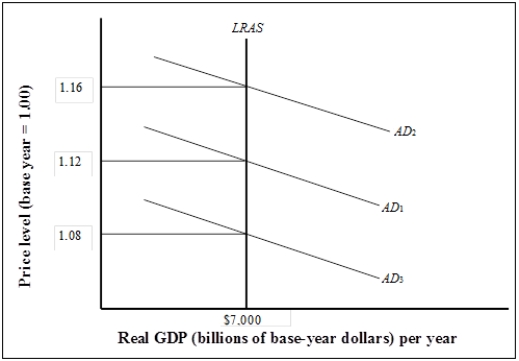

Use the following to answer questions

Exhibit: Long-run Equilibrium  -(Exhibit: Long-run Equilibrium)

Changes in aggregate demand from AD1 to either AD2 or AD3

-(Exhibit: Long-run Equilibrium)

Changes in aggregate demand from AD1 to either AD2 or AD3

(Multiple Choice)

4.8/5 (24)

Suppose the price of an important natural resource such as oil falls.What will be the effect on the short-run aggregate supply curve?

(Multiple Choice)

4.8/5 (39)

Which of the following will not cause a change in aggregate demand?

(Multiple Choice)

4.7/5 (34)

In the long run, a decrease in aggregate demand, all other things unchanged, will cause the price level to

(Multiple Choice)

4.8/5 (41)

Taking no action and allowing an economy to adjust by itself is called a nonintervention policy.

(True/False)

4.8/5 (24)

An increase in aggregate demand, all other things unchanged, in the long run will generate

(Multiple Choice)

4.8/5 (38)

Suppose the economy is initially in long-run equilibrium.Which of the following events leads to an increase in the price level and a decrease in real GDP in the short run?

(Multiple Choice)

4.9/5 (39)

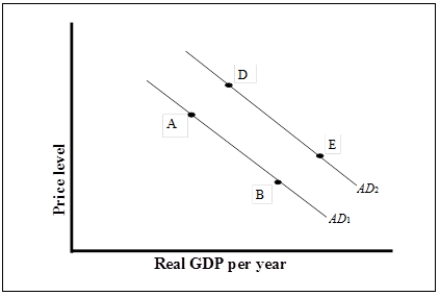

Use the following to answer questions

Exhibit: Aggregate Demand  -(Exhibit: Aggregate Demand)

What could have caused a movement from point D to point A?

-(Exhibit: Aggregate Demand)

What could have caused a movement from point D to point A?

(Multiple Choice)

4.8/5 (33)

Which of the following is a source of wage stickiness?

I.fixed wage contracts

II.minimum wage laws

III.workers and firms want to avoid complexity of negotiating contracts frequently

(Multiple Choice)

4.8/5 (37)

A graph that depicts the relationship between the total quantity of goods and services demanded and the price level is the

(Multiple Choice)

4.8/5 (32)

Which of the following statements is true of the economy in the long run? In the long run,

I.real GDP eventually moves to potential output because all wages and prices are assumed to be flexible.

II.the economy can achieve its natural level of employment and potential output at any price level.

III.there is no cyclical unemployment.

(Multiple Choice)

4.9/5 (28)

An increase in the prices of natural resources will lead to a decrease in short-run aggregate supply.

(True/False)

4.8/5 (38)

What happens in the domestic economy when there is an increase in foreign prices, all other things unchanged?

(Multiple Choice)

4.9/5 (43)

What is the difference between a change in aggregate demand and a change in aggregate quantity of real GDP demanded?

(Multiple Choice)

4.9/5 (29)

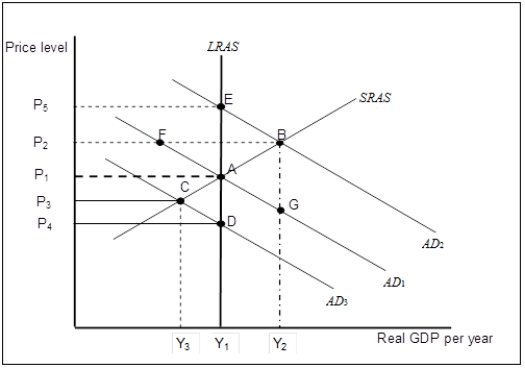

Use the following to answer questions

Exhibit: Short-run Aggregate Supply  -(Exhibit: Short-run Aggregate Supply)

Suppose that the economy is in long-run equilibrium at point A.Now suppose net exports increase.As a result of this,

-(Exhibit: Short-run Aggregate Supply)

Suppose that the economy is in long-run equilibrium at point A.Now suppose net exports increase.As a result of this,

(Multiple Choice)

4.9/5 (36)

During the recession of 2001, the leftward shifts in aggregate demand and aggregate supply that occurred at that time necessarily reduced

(Multiple Choice)

4.9/5 (35)

The short run in macroeconomics is a period in which wages and some other prices are sticky.

(True/False)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)