Exam 3: The Fundamental Economic Problem: Scarcity and Choice

Exam 1: What Is Economics254 Questions

Exam 2: The Economony: Myth and Reality184 Questions

Exam 3: The Fundamental Economic Problem: Scarcity and Choice278 Questions

Exam 4: Supply and Demand: an Initial Look297 Questions

Exam 5: Consumer Choice: Individual and Market Demand213 Questions

Exam 6: Demand and Elasticity247 Questions

Exam 7: Production, Inputs, and Cost: Building Blocks for Supply Analysis246 Questions

Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis232 Questions

Exam 9: The Financial Markets and the Economy: the Tail That Wags the Dog225 Questions

Exam 10: The Firm and the Industry Under Perfect Competition219 Questions

Exam 11: The Case for Free Markets: the Price System251 Questions

Exam 12: Monopoly236 Questions

Exam 13: Between Competition and Monopoly248 Questions

Exam 14: Limiting Market Power: Antitrust and Regulation152 Questions

Exam 15: The Shortcomings of Free Markets210 Questions

Exam 16: The Economics of the Environment, and Natural Resources218 Questions

Exam 17: Taxation and Resource Allocation218 Questions

Exam 18: Pricing the Factors of Production230 Questions

Exam 19: Labor and Entrepreneurship: the Human Inputs267 Questions

Exam 20: Poverty, Inequality, and Discrimination167 Questions

Exam 21: An Introduction to Macroeconomics212 Questions

Exam 22: The Goals of Macroeconomic Policy212 Questions

Exam 23: Economic Growth: Theory and Policy226 Questions

Exam 24: Aggregate Demand and the Powerful Consumer216 Questions

Exam 25: Demand-Side Equilibrium: Unemployment or Inflation215 Questions

Exam 26: Bringing in the Supply Side: Unemployment and Inflation228 Questions

Exam 27: Managing Aggregate Demand: Fiscal Policy207 Questions

Exam 28: Money and the Banking System222 Questions

Exam 29: Monetary Policy: Conventional and Unconventional208 Questions

Exam 30: The Financial Crisis and the Great Recession64 Questions

Exam 31: The Debate Over Monetary and Fiscal Policy216 Questions

Exam 32: Budget Deficits in the Short and Long Run214 Questions

Exam 33: The Trade-Off Between Inflation and Unemployment218 Questions

Exam 34: International Trade and Comparative Advantage215 Questions

Exam 35: The International Monetary System: Order or Disorder216 Questions

Exam 36: Exchange Rates and the Macroeconomy215 Questions

Exam 37: Contemporary Issues in the Useconomy23 Questions

Select questions type

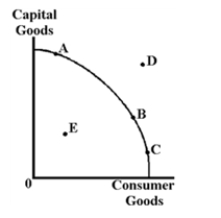

Figure 3-2  -In Figure 3-2, at point B

-In Figure 3-2, at point B

Free

(Multiple Choice)

4.9/5  (30)

(30)

Correct Answer: Verified

Verified

D

Figure 3-2

-In Figure 3-2, a point such as E

Free

(Multiple Choice)

4.8/5 (42)

Correct Answer:Verified

C

Efficient production can be carried out anywhere on or beyond the production possibilities frontier.

Free

(True/False)

4.8/5 (37)

Correct Answer:Verified

False

The law of comparative advantage implies that a doctor who is also a talented auto mechanic should

(Multiple Choice)

4.7/5 (29)

A production possibilities curve always slopes downward to the right because resources

(Multiple Choice)

4.7/5 (43)

While specialization and exchange were very important to Adam Smith in 1776, they have largely lost their importance in the 21st century.

(True/False)

4.9/5 (39)

The workers in Adam Smith's famous pin factory, who were proficient in pin production, faced the problem of

(Multiple Choice)

4.8/5 (34)

If good "A" is represented on the horizontal axis and good "B" on the vertical axis, then the steeper the production possibilities frontier at a given level of production of good "A," the

(Multiple Choice)

4.9/5 (40)

If a farmer's opportunity cost of producing 50,000 bushels of wheat is 20,000 fewer bushels of soybeans, then his or her opportunity cost of producing 50,000 bushels of soybeans must also be 20,000 fewer bushels of wheat.

(True/False)

4.9/5 (37)

Which of the following is likely to affect the position and shape of society's production possibilities frontier?

(Multiple Choice)

4.9/5 (40)

In a market system, ____ distributes goods among consumers in accord with their tastes and preferences, using voluntary exchange to determine who gets what.

(Multiple Choice)

4.8/5 (30)

What mechanism assures that firms produce outputs that consumers actually desire?

(Multiple Choice)

4.9/5 (34)

If a market system is functioning well, we can conclude that goods with

(Multiple Choice)

4.8/5 (31)

Economists use the term capital to describe that factor of production that includes human-made resources such as factories, buildings, machinery, and tools.

(True/False)

4.9/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)