Exam 1: Limits, Alternatives, and Choices

Exam 1: Limits, Alternatives, and Choices107 Questions

Exam 2: The Market System and the Circular Flow287 Questions

Exam 3: Demand, Supply, and Market Equilibrium151 Questions

Exam 4: Market Failures Caused by Externalities Asymmetric Information229 Questions

Exam 5: Public Goods, Public Choice, and Government Failure268 Questions

Exam 6: Elasticity399 Questions

Exam 7: Utility Maximization358 Questions

Exam 8: Behavioral Economics311 Questions

Exam 9: Businesses and the Costs of Production445 Questions

Exam 10: Pure Competition in the Short Run342 Questions

Exam 11: Pure Competition in the Long Run250 Questions

Exam 12: Pure Monopoly407 Questions

Exam 13: Monopolistic Competition279 Questions

Exam 14: Oligopoly and Strategic Behavior362 Questions

Exam 15: Technology, RD, and Efficiency309 Questions

Exam 16: The Demand for Resources359 Questions

Exam 17: Wage Determination168 Questions

Exam 18: Rent, Interest, and Profit305 Questions

Exam 19: Natural Resource and Energy Economics337 Questions

Exam 20: Public Finance: Expenditures and Taxes336 Questions

Exam 21: Antitrust Policy and Regulation264 Questions

Exam 22: Agriculture: Economics and Policy265 Questions

Exam 23: Income Inequality, Poverty, and Discrimination324 Questions

Exam 24: Health Care280 Questions

Exam 25: Immigration259 Questions

Exam 26: International Trade347 Questions

Exam 27: The Balance of Payments, Exchange Rates, and Trade Deficits318 Questions

Exam 28: The Economics of Developing Countries277 Questions

Select questions type

The economizing problem is one of deciding how to make the best use of

(Multiple Choice)

4.9/5  (31)

(31)

When economists say that people act rationally in their self-interest, they mean that individuals

(Multiple Choice)

4.8/5 (31)

The fundamental economic problem faced by a society is that productive resources are so varied and versatile that it is hard to decide what to do with them.

(True/False)

4.8/5 (36)

Economists have difficulty applying the scientific method because

(Multiple Choice)

4.8/5 (38)

If economic theories are solidly based on relevant facts, then appropriate economic policy becomes obvious and uncontroversial.

(True/False)

4.8/5 (41)

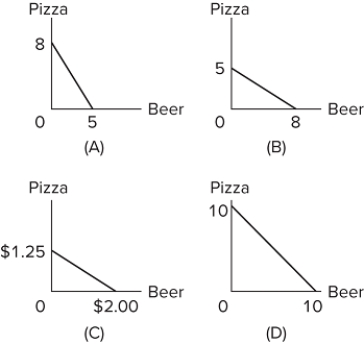

Refer to the graphs. Assume that pizza is measured in slices and beer in pints. In which of the graphs is the opportunity cost of a pint of beer equal to one slice of pizza?

Refer to the graphs. Assume that pizza is measured in slices and beer in pints. In which of the graphs is the opportunity cost of a pint of beer equal to one slice of pizza?

(Multiple Choice)

4.8/5 (32)

Answer the question on the basis of the data given in the following production possibilities table.  Refer to the table. If the economy is producing at production alternative B, the opportunity cost of the sixth unit of consumer goods will be approximately

Refer to the table. If the economy is producing at production alternative B, the opportunity cost of the sixth unit of consumer goods will be approximately

(Multiple Choice)

4.8/5 (30)

Assume the price of product Y (the quantity of which is on the vertical axis)is $10 and the price of product X (the quantity of which is on the horizontal axis)is $5. Also assume that money income is $30. The absolute value of the slope of the resulting budget line is

(Multiple Choice)

4.8/5 (30)

The comment that "taxes must be reduced for the good of the economy" is an example of a normative economic statement.

(True/False)

4.8/5 (33)

The slope of a graph relating two variables is −5. This indicates that as one variable decreases, the other variable also decreases.

(True/False)

4.9/5 (35)

In graphing a relationship between two variables, economists always follow the mathematical convention. Thus, if price is the independent variable then it is measured on the horizontal axis.

(True/False)

4.9/5 (30)

Assume that a consumer has a given budget or income of $12 and that she can buy only two goods, apples or bananas. The price of an apple is $2.00 and the price of a banana is $1.00. This means that, in order to buy six bananas, this consumer must forgo

(Multiple Choice)

4.9/5 (35)

The slope of a graph measures the rate of change in one variable as the other variable changes.

(True/False)

4.9/5 (35)

A person should consume more of something when its marginal

(Multiple Choice)

4.8/5 (33)

When economists talk about the capital resources in the economy, they are referring to the amount of money circulating in the economy.

(True/False)

4.9/5 (32)

An increase in immigration would shift the production possibilities curve to the left.

(True/False)

4.9/5 (29)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)