Exam 11: Pure Competition in the Long Run

Exam 1: Limits, Alternatives, and Choices107 Questions

Exam 2: The Market System and the Circular Flow287 Questions

Exam 3: Demand, Supply, and Market Equilibrium151 Questions

Exam 4: Market Failures Caused by Externalities Asymmetric Information229 Questions

Exam 5: Public Goods, Public Choice, and Government Failure268 Questions

Exam 6: Elasticity399 Questions

Exam 7: Utility Maximization358 Questions

Exam 8: Behavioral Economics311 Questions

Exam 9: Businesses and the Costs of Production445 Questions

Exam 10: Pure Competition in the Short Run342 Questions

Exam 11: Pure Competition in the Long Run250 Questions

Exam 12: Pure Monopoly407 Questions

Exam 13: Monopolistic Competition279 Questions

Exam 14: Oligopoly and Strategic Behavior362 Questions

Exam 15: Technology, RD, and Efficiency309 Questions

Exam 16: The Demand for Resources359 Questions

Exam 17: Wage Determination168 Questions

Exam 18: Rent, Interest, and Profit305 Questions

Exam 19: Natural Resource and Energy Economics337 Questions

Exam 20: Public Finance: Expenditures and Taxes336 Questions

Exam 21: Antitrust Policy and Regulation264 Questions

Exam 22: Agriculture: Economics and Policy265 Questions

Exam 23: Income Inequality, Poverty, and Discrimination324 Questions

Exam 24: Health Care280 Questions

Exam 25: Immigration259 Questions

Exam 26: International Trade347 Questions

Exam 27: The Balance of Payments, Exchange Rates, and Trade Deficits318 Questions

Exam 28: The Economics of Developing Countries277 Questions

Select questions type

A long-run supply curve that is downward sloping indicates that the firms' ATC curves

Free

(Multiple Choice)

4.8/5  (31)

(31)

Correct Answer: Verified

Verified

C

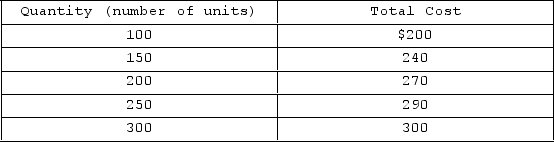

Suppose the table above represents the long-run cost structure for a firm in a perfectly competitive industry. Based on this information we can conclude that this firm operates in

Suppose the table above represents the long-run cost structure for a firm in a perfectly competitive industry. Based on this information we can conclude that this firm operates in

Free

(Multiple Choice)

4.8/5 (30)

Correct Answer:Verified

B

What is the triple equality that we find in pure competition after all long-run adjustments have been made?

Free

(Essay)

4.8/5 (29)

Correct Answer:Verified

In a constant-cost or increasing-cost industry, in the long run, P = minimum ATC = MC. The final long-run equilibrium positions of all firms have these same basic efficiency characteristics. Price (and marginal revenue)will settle where it is equal to minimum average total cost. Because the MC curve intersects the ATC curve at its minimum point, marginal cost and average total cost are equal. In long-run equilibrium, each firm produces at the output level that is associated with this triple equality.

The reason why the long-run supply curve for a purely competitive industry may be upward-sloping is because of diminishing marginal returns.

(True/False)

4.8/5 (31)

What three assumptions are used in the chapter to keep the analysis relatively simple?

(Essay)

4.8/5 (41)

Resources are efficiently allocated when production occurs where

(Multiple Choice)

4.7/5 (31)

Is there a specific amount of time that distinguishes the long run from the short run? Is the amount of time important? Explain.

(Essay)

4.8/5 (29)

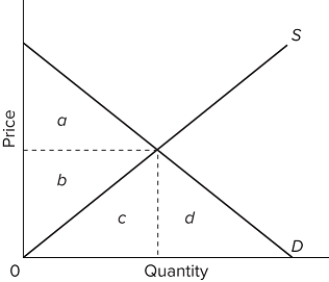

The accompanying graph represents the purely competitive market for a product. When the market is at equilibrium, the total revenues from selling the equilibrium output level would be represented by the area

The accompanying graph represents the purely competitive market for a product. When the market is at equilibrium, the total revenues from selling the equilibrium output level would be represented by the area

(Multiple Choice)

4.8/5 (36)

The long-run supply curve for a competitive, decreasing-cost industry is downward-sloping.

(True/False)

4.8/5 (31)

Long-run adjustments in purely competitive markets primarily take the form of

(Multiple Choice)

4.8/5 (36)

Because the equilibrium position of a purely competitive seller entails an equality of price and marginal costs, competition produces an efficient allocation of economic resources.

(True/False)

4.8/5 (30)

The transformative effects of competition that foster the development of new products or new production methods benefit everyone in society.

(True/False)

4.9/5 (29)

When there is allocative efficiency in a purely competitive market for a product, the minimum price producers are willing to accept is

(Multiple Choice)

4.7/5 (45)

Compare the shape of a long-run supply curve for a constant-cost industry, a decreasing-cost industry, and an increasing-cost industry.

(Essay)

4.9/5 (33)

If the representative firm in a purely competitive industry is in short-run equilibrium and, at its current output level, its marginal cost exceeds its average total cost, then we can conclude that

(Multiple Choice)

4.8/5 (46)

If the price of bottled water is $1.00 and the marginal cost of producing it is $1.50,

(Multiple Choice)

4.9/5 (35)

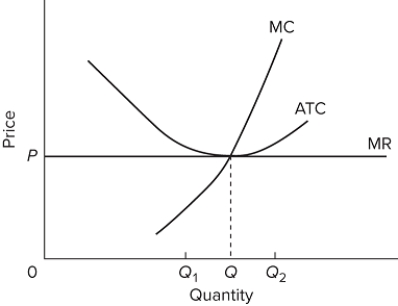

If the competitive firm depicted in this diagram produces output Q, it will

If the competitive firm depicted in this diagram produces output Q, it will

(Multiple Choice)

4.8/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)