Exam 9: Perfect Competition

Exam 1: What Economics Is About174 Questions

Exam 2: Production Possibilities Frontier Framework157 Questions

Exam 3: Supply and Demand: Theory224 Questions

Exam 4: Prices: Free, Controlled, and Relative123 Questions

Exam 5: Supply, Demand, and Price: Applications80 Questions

Exam 6: Elasticity204 Questions

Exam 7: Consumer Choice: Maximizing Utility and Behavioral Economics179 Questions

Exam 8: Production and Costs246 Questions

Exam 9: Perfect Competition187 Questions

Exam 10: Monopoly195 Questions

Exam 11: Monopolistic Competition, Oligopoly, and Game Theory172 Questions

Exam 12: Government and Product Markets: Antitrust and Regulation158 Questions

Exam 13: Factor Markets: With Emphasis on the Labor Market182 Questions

Exam 14: Wages, Union, and Labor133 Questions

Exam 15: The Distribution of Income and Poverty100 Questions

Exam 16: Interest, Rent, and Profit195 Questions

Exam 17: Market Failure: Externalities, Public Goods, and Asymmetric Information183 Questions

Exam 18: Public Choice and Special-Interest-Group Politics129 Questions

Exam 19: Building Theories to Explain Everyday Life: From Observations to Questions to Theories to Predictions61 Questions

Exam 20: International Trade153 Questions

Exam 21: International Finance121 Questions

Exam 22: The Economic Case for and Against Government: Five Topics Considered82 Questions

Exam 23: Stocks, Bonds, Futures, and Options110 Questions

Select questions type

A perfectly competitive market is initially in long-run competitive equilibrium. Then, market demand increases. By the time all adjustments have been made, price will be __________ its original level if the industry is a(n)__________ cost industry.

Free

(Multiple Choice)

4.9/5  (33)

(33)

Correct Answer: Verified

Verified

B

In long-run competitive equilibrium, firms

Free

(Multiple Choice)

4.7/5 (31)

Correct Answer:Verified

B

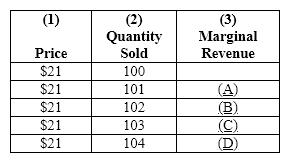

Exhibit 22-1  Refer to Exhibit 22-1. The dollar amounts that go in blanks (C)and (D)are, respectively,

Refer to Exhibit 22-1. The dollar amounts that go in blanks (C)and (D)are, respectively,

Free

(Multiple Choice)

4.9/5 (33)

Correct Answer:Verified

B

Consider the following data: equilibrium price = $40, quantity of output produced = 100 units, average total cost = $47, and average variable cost = $37. What should the firm do and why?

(Multiple Choice)

4.9/5 (33)

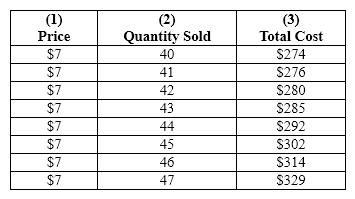

Exhibit 22-3  Refer to Exhibit 22-3. Based upon the information provided in this table, what is the maximum profit this firm can earn?

Refer to Exhibit 22-3. Based upon the information provided in this table, what is the maximum profit this firm can earn?

(Multiple Choice)

4.8/5 (39)

What is the shape of the demand curve faced by the perfectly competitive firm? Why does it have this shape?

(Essay)

4.8/5 (37)

Equilibrium price is $10 in a perfectly competitive market. For a perfectly competitive firm, MR = MC at 1,200 units of output. At 1,200 units, ATC is $23, and AVC is $18. The best policy for this firm is to __________ in the short run. Also, this firm earns __________ of __________ if it produces and sells 1,200 units.

(Multiple Choice)

4.9/5 (34)

Ultimately, market supply curves are upward sloping because of

(Multiple Choice)

4.9/5 (26)

Equilibrium price is $17 in a perfectly competitive market. For a perfectly competitive firm, MR = MC at 275 units of output. At 275 units, ATC is $19, and AVC is $13. The best policy for this firm is to __________ in the short run. Also, total fixed cost equals __________ for this firm.

(Multiple Choice)

4.8/5 (35)

Why is profit maximized at the level of output where marginal revenue equals marginal cost?

(Essay)

4.8/5 (36)

The price charged by a perfectly competitive firm is determined by

(Multiple Choice)

4.8/5 (32)

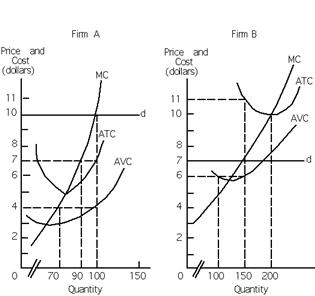

Exhibit 22-8

Refer to Exhibit 22-8. What is the total revenue of firm B at profit-maximizing (or loss-minimizing)level of output?

Refer to Exhibit 22-8. What is the total revenue of firm B at profit-maximizing (or loss-minimizing)level of output?

(Multiple Choice)

4.8/5 (31)

Consider the following data: equilibrium price = $15, quantity of output produced = 10,000 units, average total cost = $12, and average variable cost $7. Given this data, total revenue is __________, total cost is __________, and total fixed cost is __________.

(Multiple Choice)

4.8/5 (38)

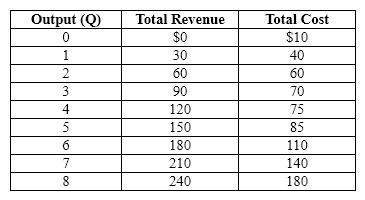

Exhibit 22-10  Refer to Exhibit 22-10. What is the marginal revenue and marginal cost, respectively, of the 7th unit of output?

Refer to Exhibit 22-10. What is the marginal revenue and marginal cost, respectively, of the 7th unit of output?

(Multiple Choice)

5.0/5 (38)

A perfectly competitive firm that maximizes profit exhibits resource allocative efficiency because it produces where price

(Multiple Choice)

4.8/5 (40)

In perfect competition, the firm's marginal revenue curve is

(Multiple Choice)

4.7/5 (37)

A firm operating in a perfectly competitive market finds itself producing a level of output for which marginal revenue is less than marginal cost. In order to maximize profits (or minimize losses), the firm should

(Multiple Choice)

4.9/5 (41)

For a price taker, market equilibrium price is $50. At 1,000 units, MR = MC, ATC = $45, and AVC = $30. This price taker will

(Multiple Choice)

4.8/5 (36)

One of the assumptions upon which the theory of perfect competition is built is that each firm produces and sells a heterogeneous product.

(True/False)

4.7/5 (31)

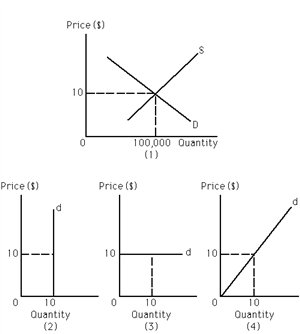

Exhibit 22-6

Refer to Exhibit 22-6. A perfectly competitive firm operating in the market depicted in graph (1)is producing 311 units of output at the profit-maximizing level. What is the marginal revenue of the 312th unit?

Refer to Exhibit 22-6. A perfectly competitive firm operating in the market depicted in graph (1)is producing 311 units of output at the profit-maximizing level. What is the marginal revenue of the 312th unit?

(Multiple Choice)

4.8/5 (29)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)