Exam 18: Accounting for Decision-Making: Resource Constraints and Decisions Which Are Mutually Exclusive

Exam 1: Introduction to Accounting19 Questions

Exam 2: Wealth and the Measurement of Profit17 Questions

Exam 3: The Measurement of Wealth16 Questions

Exam 4: The Income Statement and the Cash Flow Statement17 Questions

Exam 5: Introduction to the Worksheet17 Questions

Exam 6: Inventory17 Questions

Exam 7: Amounts Receivable and Amounts Payable18 Questions

Exam 8: Non-Current Assets, Fixed Assets, and Depreciation19 Questions

Exam 9: Financing and Business Structures16 Questions

Exam 10: Cash Flow Statements15 Questions

Exam 11: Final Accounts and Company Accounts19 Questions

Exam 12: Financial Statement Analysis19 Questions

Exam 13: Internal Users and Internal Information18 Questions

Exam 14: Planning and Control16 Questions

Exam 15: Cost Behaviour and Cost-Volume-Profit Analysis20 Questions

Exam 16: Accounting for Overheads and Product Costs20 Questions

Exam 17: Accounting for Decision-Making: When There Are No Resource Constraints20 Questions

Exam 18: Accounting for Decision-Making: Resource Constraints and Decisions Which Are Mutually Exclusive20 Questions

Exam 19: Budgets20 Questions

Exam 20: Investment Decisions20 Questions

Exam 21: Management of Working Capital20 Questions

Select questions type

The cash cost of employing labour, for example, is the internal opportunity cost.

Free

(True/False)

4.9/5  (36)

(36)

Correct Answer: Verified

Verified

False

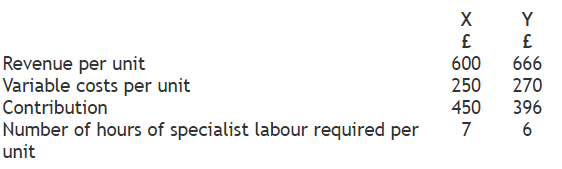

Hobson Limited produces two products, the X and Y, which both use the same grade of specialist labour. Only 3800 specialist labour hours are estimated to be available for the 20X1 financial year because of skills shortages in the economy as a whole.

Ideally the directors would like to sell 500 units of X and 500 units of Y but they recognize the actual amount that can be produced and sold is likely to be limited by the labour shortage.

The following information is available about the products:

What is the optimal production plan for 20X1 (to the nearest whole unit)?

What is the optimal production plan for 20X1 (to the nearest whole unit)?

Free

(Multiple Choice)

4.8/5 (33)

Correct Answer:Verified

B

For decisions where there are constraints the objective is to establish a optimum output within the constraint which will maximise contribution.

Free

(True/False)

4.8/5 (39)

Correct Answer:Verified

True

Differential costs are the differences between fixed and variable costs.

(True/False)

4.9/5 (32)

Invariably, the opportunity cost of a resource that is scarce will be greater than its purchase price.

(True/False)

4.7/5 (42)

It is necessary to establish the contribution per unit of constraint in determining the optimal output level when there is a constraint.

(True/False)

4.8/5 (30)

The analysis of constraints and decision making is only appropriate to manufacturing not service industries.

(True/False)

4.9/5 (40)

Product X - Contribution £40 and uses 20 scarce machine hours. Component Y - used in manufacture of X, has a variable cost of £5 and uses 3 machine hours. Component y can be bought for £10. In determining whether to make or buy what is the relevant cost of making:

(Multiple Choice)

4.7/5 (35)

Were there are resource constraints this will not affect accept or reject decisions

(True/False)

4.8/5 (37)

The make or buy decision is probably the most common type of mutually exclusive decision that confronts organisations.

(True/False)

4.9/5 (45)

When there are no resource constraints all opportunities should be accepted if they make a profit.

(True/False)

4.8/5 (39)

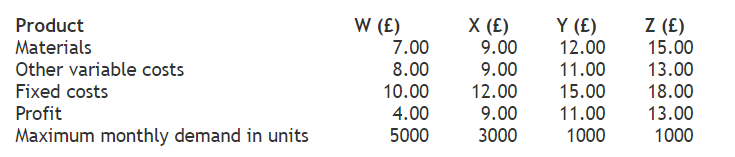

Ben Plc makes a range of clutches for which the cost cards show the following:

For the coming month material suppliers will be limited to £50 000.

The optimum production plan is:

For the coming month material suppliers will be limited to £50 000.

The optimum production plan is:

(Multiple Choice)

4.9/5 (34)

Constraints are often restrict the amount of productive capacity available to a business, or the potential market for a product, or the availability of particular types of material or labour. In management accounting, such constraints are commonly referred to as:

(Multiple Choice)

4.7/5 (36)

A make or buy decision involves the problem of a business choosing between making a product or carrying out a service using its own resources, and paying another external organisation to make or carry out a service for them.

(True/False)

4.9/5 (43)

Additup Ltd manufactures and markets pocket calculators which sell at £22 each. Current output is 40000 units per month, which represent 90% of the plants capacity. A new chain-store offers to buy up to 5000 calculators as a special order at £18 per unit and requires these immediately. These would sell under their own brand name. Total costs per month are £800000 of which £192000 are fixed costs. Assuming that the company maximises profits what is the profit made:

(Multiple Choice)

4.9/5 (37)

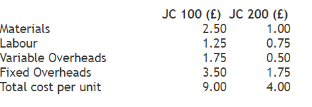

A firm at present manufacturers all the components that go to make up its finished products. A salesman from a component supplier has just offered to provide the firm’s requirements for two components, the JC 100 at £7.75 each and the JC 200 at £2 each. If the firm buys in the components the capacity utilised at present would be unused. The firm currently manufactures 50 000 units of each component and the current costs of production are as follows:

What is the extra cost (EC) or saving (S) per unit if the company decides to buy in the component:

JC 100 (£) JC 200 (£)

What is the extra cost (EC) or saving (S) per unit if the company decides to buy in the component:

JC 100 (£) JC 200 (£)

(Multiple Choice)

4.9/5 (41)

To determine the optimum output with one resource constraint the criteria should be

(Multiple Choice)

4.7/5 (33)

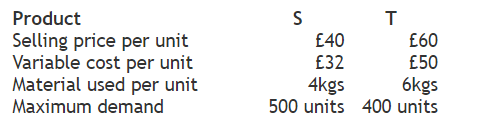

A firm manufacturers two products both of which require the same material. For the coming month the supply of material is limited to 2,600kgs. Details of each product are as follows:

The production plan that will maximum profit is

The production plan that will maximum profit is

(Multiple Choice)

4.7/5 (27)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)