Exam 13: Current Liabilities and Contingencies

Exam 1: Environment and Theoretical Structure of Financial Accounting181 Questions

Exam 2: Review of the Accounting Process 139 Questions

Exam 3: The Balance Sheet and Financial Disclosures168 Questions

Exam 4: The Income Statement, Comprehensive Income, and the Statement of Cash Flows178 Questions

Exam 5: Revenue Recognition316 Questions

Exam 6: Time Value of Money Concepts126 Questions

Exam 7: Cash and Receivables187 Questions

Exam 8: Inventories: Measurement182 Questions

Exam 9: Inventories: Additional Issues153 Questions

Exam 10: Property, Plant, and Equipment and Intangible Assets: Acquisition149 Questions

Exam 11: Property, Plant, and Equipment and Intangible Assets: Utilization and Disposition223 Questions

Exam 12: Investments183 Questions

Exam 13: Current Liabilities and Contingencies155 Questions

Exam 14: Bonds and Long-Term Notes256 Questions

Exam 15: Leases262 Questions

Exam 16: Accounting for Income Taxes176 Questions

Exam 17: Pensions and Other Postretirement Benefits246 Questions

Exam 18: Shareholders Equity179 Questions

Exam 19: Share-Based Compensation and Earnings Per Share231 Questions

Exam 20: Accounting Changes and Error Corrections152 Questions

Exam 21: The Statement of Cash Flows Revisited192 Questions

Select questions type

Which of the following is a contingency that would most likely require accrual?

(Multiple Choice)

4.8/5  (34)

(34)

All else equal, a large increase in deferred revenue in the current period would be expected to produce what effect on revenue in a future period?

(Multiple Choice)

4.9/5 (39)

When a deposit on returnable containers is forfeited, the firm holding the deposit will experience:

(Multiple Choice)

4.8/5 (38)

A line of credit is an agreement to provide long-term financing, typically made with a bank or a group of banks.

(True/False)

4.9/5 (28)

On December 31, 2018, L Inc. had a $1,500,000 note payable outstanding, due July 31, 2019. L borrowed the money to finance construction of a new plant. L planned to refinance the note by issuing long-term bonds. Because L temporarily had excess cash, it prepaid $500,000 of the note on January 23, 2019. In February 2019, L completed a $3,000,000 bond offering. L will use the bond offering proceeds to repay the note payable at its maturity and to pay construction costs during 2019. On March 13, 2019, L issued its 2018 financial statements. What amount of the note payable should L include in the current liabilities section of its December 31, 2018, balance sheet?

(Multiple Choice)

4.9/5 (36)

Under IFRS, if it is probable that a contingent liability will result in a future payment but there is a range of equally likely amounts that will be paid, the midpoint of the range should be accrued as a loss.

(True/False)

4.8/5 (34)

Amber Inc. is one of the largest pharmacy retailers in mid-America. In its 2018 annual report to shareholders, it made the following disclosure:

In 2013, Amber assigned a number of leases to Bell's Inc. and Home Stores, Inc., as part of the sale of the Company's former Eastern divisions. Amber is contingently liable if Bell's and Home are unable to continue making rental payments on these leases. In 2017, Amber recorded a pretax charge to earnings of $42.7 million to recognize the estimated lease liabilities associated with the Bell's and Home bankruptcies and for a single lease from Amber's former Georgia division. In 2018, Bell's began the liquidation process and Home emerged from bankruptcy and, based on the resolution of various leases, Amber reversed $12.1 million of this accrual.

Explain the accounting principle(s) that required Amber to record the $42.7 million charge in 2017 and the $12.1 million reversal in 2018.

(Essay)

4.8/5 (28)

Which of the following generally is associated with accounts payable?

(Multiple Choice)

4.8/5 (43)

Providing a monetary rebate program for purchasing a product:

(Multiple Choice)

5.0/5 (42)

A contingent loss should be reported in a disclosure note to the financial statements rather than being accrued if:

(Multiple Choice)

4.7/5 (26)

Branch Company, a building materials supplier, has $18,000,000 of notes payable due April 12, 2019. At December 31, 2018, Branch signed an agreement with First Bank to borrow up to $18,000,000 to refinance the notes on a long-term basis. The agreement specified that borrowings would not exceed 75% of the value of the collateral that Branch provided. At the date of issue of the December 31, 2018, financial statements, the value of Branch's collateral was $20,000,000. On its December 31, 2018, balance sheet, Branch should classify the notes as follows:

(Multiple Choice)

4.8/5 (34)

Which of the following is not a characteristic of a liability?

(Multiple Choice)

4.9/5 (38)

On January 1, 2018, G Corporation agreed to grant all its employees two weeks paid vacation each year, with the stipulation that vacations earned each year can be taken the following year. For the year ended December 31, 2018, G's employees each earned an average of $800 per week. A total of 500 vacation weeks earned in 2018 were not taken during 2018. Wage rates for employees rose by an average of 5 percent by the time vacations actually were taken in 2019. What is the amount of G's 2019 wages expense related to 2018 vacation time?

(Multiple Choice)

4.9/5 (35)

The following selected transactions relate to liabilities of Chicago Glass Corporation for 2018. Chicago's fiscal year ends on December 31.

1. On January 15, Chicago received $7,000 from Henry Construction toward the purchase of $66,000 of plate glass to be delivered on February 6.

2. On February 3, Chicago received $6,700 of refundable deposits relating to containers used to transport glass components.

3. On February 6, Chicago delivered the plate glass to Henry Construction and received the balance of the purchase price.

4. First quarter credit sales totaled $700,000. The state sales tax rate is 4% and the local sales tax rate is 2%.

Required:

Prepare journal entries for the above transactions.

(Essay)

5.0/5 (41)

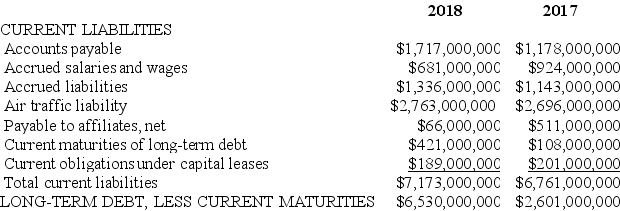

In its 2018 annual report to shareholders, Border Airlines Inc. presented the following balance sheet information about its liabilities:  In addition, Border presented the following among its note disclosures:

Maturities of long-term debt (including sinking fund requirements) for the next five years are: 2019 - $421 million; 2020 - $212 million; 2021 - $273 million; 2022 - $1.0 billion; 2023 - $777 million.

Required:

Consider the appropriate classification of these long-term debt obligations. Assuming no more long-term debt will be issued, what are the implications of the information above for Border's liquidity and solvency risk in 2018 and the following years?

In addition, Border presented the following among its note disclosures:

Maturities of long-term debt (including sinking fund requirements) for the next five years are: 2019 - $421 million; 2020 - $212 million; 2021 - $273 million; 2022 - $1.0 billion; 2023 - $777 million.

Required:

Consider the appropriate classification of these long-term debt obligations. Assuming no more long-term debt will be issued, what are the implications of the information above for Border's liquidity and solvency risk in 2018 and the following years?

(Essay)

4.8/5 (44)

Identify the major components included in the official definition of a liability as set forth by Statement of Financial Accounting Concepts No. 6, "Elements of Financial Statements."

(Essay)

4.9/5 (40)

Panther Co. had a quality-assurance warranty liability of $350,000 at the beginning of 2018 and $310,000 at the end of 2018. Warranty expense is based on 4% of sales, which were $50 million for the year. What were the warranty expenditures for 2018?

(Multiple Choice)

4.9/5 (33)

Expense for a quality-assurance warranty is recorded along with the related liability in the reporting period in which the product under warranty is sold.

(True/False)

4.9/5 (37)

Diversified Industries sells perishable electronic products. Some must be shipped in reusable containers. Customers pay a deposit for each container. The deposit is equal to the container's cost. Customers receive a refund when the container is returned. During 2018, deposits collected on containers shipped were $700,000. Deposits are forfeited if containers are not returned in 18 months. Containers held by customers on January 1, 2018, were $330,000. During 2018, $410,000 was refunded and deposits of $25,000 were forfeited.

Required:

1. Prepare the appropriate journal entries for the deposits received and returned during 2018.

2. Determine the liability for refundable deposits to be reported in the December 31, 2018, balance sheet.

(Essay)

4.7/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)